A tendency has developed among commentators to dismiss the relevance of discouraging employment data, based on the view that the labour market is a lagging indicator of the economy (e.g., a recent post by a prominent Australian economic commentator: Crappy jobs data, but it is a lagging indicator). As I posted on early last week, I don’t believe this is true (Sorry to tell you, QTC, but the labour market is not a lagging indicator). Some of the misunderstanding among commentators possibly relates to the somewhat complicated fashion in which employment and GDP are related.

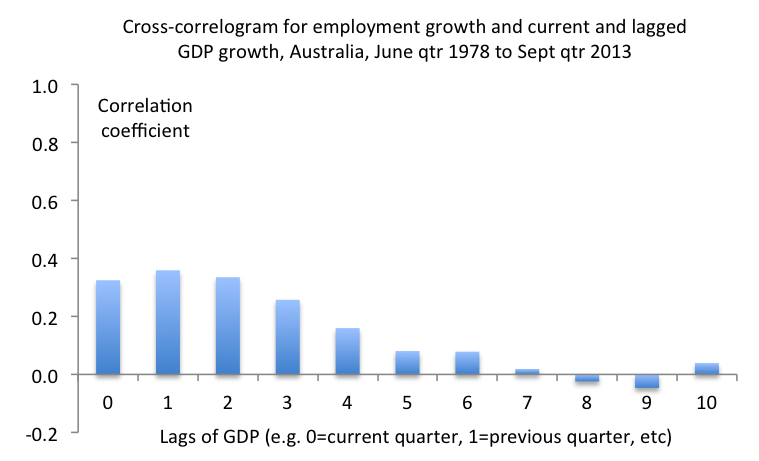

The growth rates of employment and GDP are correlated in the current quarter, but employment growth in the current quarter is also related to GDP growth in, at least, the three previous quarters. That is, employment reacts to current economic conditions, but only partially, and the adjustment to current conditions continues in future quarters. In Australia, this lagged impact is reasonably strong, based on the correlations between quarterly Australian employment growth and GDP growth in current and previous quarters reported in the chart (a cross-correlogram) below.

Note: In this chart, the value at lag 0 is the correlation between current employment growth and current GDP growth, the value at lag 1 is the correlation between current employment growth and GDP in the previous quarter (i.e. GDP growth lagged one quarter), and so on. (Note that from lag 4 onwards, the correlation is not statistically significant).

Nonetheless, employment growth is significantly related to GDP growth in the current quarter, and hence I maintain it is incorrect to suggest the labour market is a lagging indicator. Current employment growth may indeed be telling us something important about current economic conditions.

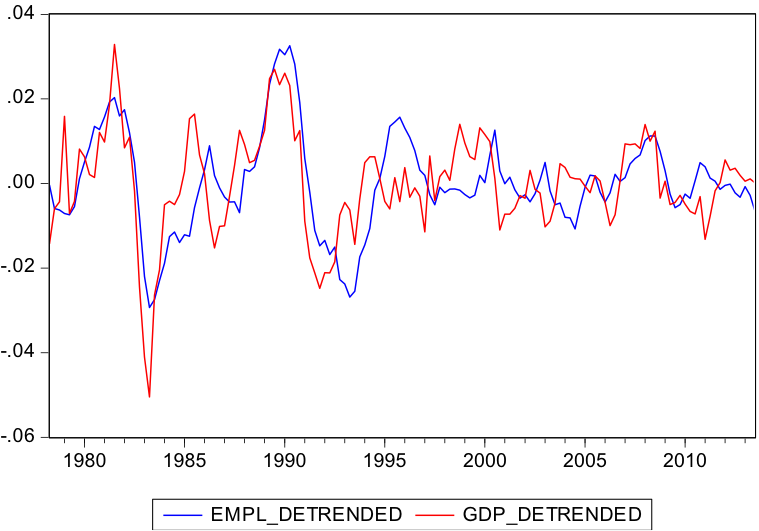

This chart of de-trended Australian employment and de-trended GDP (generated using the Hodrick-Prescott filter) confirms that employment and GDP often plunge or rebound in the same quarter, although I acknowledge there are occasions where a lagged relationship appears to exist:

I’m willing to concede that the employment and GDP relationship is complicated, but I won’t accept that employment is typically a lagging indicator of the economy. While I’m not too worried yet, it is very possible the labour market is telling us the economy is not currently in good shape, and recent employment data shouldn’t be quickly dismissed.