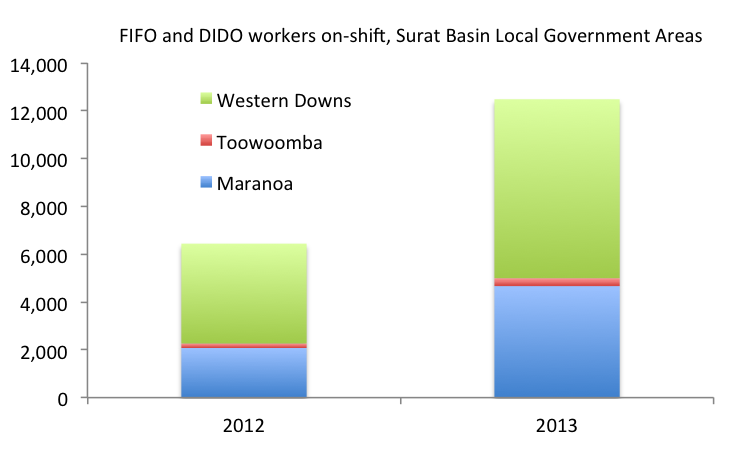

The new data from Queensland Treasury on non-resident – i.e. fly-in, fly-out (FIFO) or drive-in, drive-out (DIDO) – workers in the Surat Basin illustrate the boom we’re seeing in the gas-field communities out west of Toowoomba on the Darling Downs, including Chinchilla, Miles and Roma (see the Treasury report). FIFO and DIDO workers in the Surat Basin local government areas increased from 6,445 to 12,480 people in 2013 – an increase of 94% (see chart below).

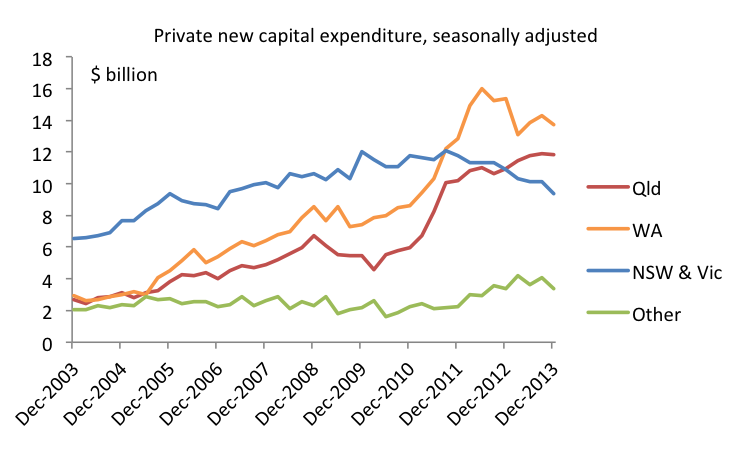

The activity in the gas fields and the commencement of LNG exports later this year is one reason I’m not panicking yet about the plateauing of capital expenditure in Queensland that is now evident in the data, and the declines in other States, particularly WA, driven by falls in mining investment, and in NSW and Victoria, reflecting the parlous state of Australia’s manufacturing sector (see chart below).

The activity in the gas fields and the commencement of LNG exports later this year is one reason I’m not panicking yet about the plateauing of capital expenditure in Queensland that is now evident in the data, and the declines in other States, particularly WA, driven by falls in mining investment, and in NSW and Victoria, reflecting the parlous state of Australia’s manufacturing sector (see chart below).

Good coverage of yesterday’s capital expenditure data can be found at MacroBusiness and Pete Faulkner’s website:

Good coverage of yesterday’s capital expenditure data can be found at MacroBusiness and Pete Faulkner’s website:

Actual capital expenditures fall sharply

Q4 CAPEX will hit GDP. Forward estimate weak.

Queensland is now expected to see a large drop in capital expenditure over 2014 and there will clearly be a loss of construction jobs associated with this over coming years, as projected in a construction industry report released yesterday:

8000 Queensland construction jobs to go: report

Nonetheless I remain confident about Queensland’s longer-term prospects and our ability to adjust to the drop in mining-related construction, as I’ve posted on before:

Qld’s economic future bright if we look beyond short-term

That said, it’s possible the whole Australian economy could be in for a challenging year in 2014, given recent discouraging signs from the labour market suggesting a weak economy.

I’m not sure I am quite as optimistic about the medium to longer term prospects for the Queensland economy. I suspect we are actually entering a prolonged period of sluggish growth at best. The Deloitte’s report you refer to suggests the greatest prospects are in a few areas (gas, agribusiness, tourism, higher education). I cannot see where their optimism is really coming from unless they make some bold assumptions about Australia’s future international competitiveness.

Gas. Expansion phase has a few years to go (albeit growing at a slower rate), before a prolonged production for export cycle. Lots of royalties for the Government, but negligible value adding and not much employment.

Agribusiness. Governments and commentators get very excited about feeding hundreds of millions of emerging middle class citizens in Asia. But for the foreseeable future, a high AUD, high capital and labour costs in Australia, high cost logistical chains, and deliberate (and subsidised) policies for food self reliance in most Asian countries, probably means we will be a bit player only.

Tourism is showing signs of life as the AUD falls (good all round for Queensland operators) and new markets are emerging (e.g. China, India). But there is still a lot of scope for growth in visitor numbers before we get anywhere near historical heights.

Higher education is recovering from a very high AUD and bad reputational issues. But growth in the international student market will be constrained by improvements in the quality of universities in Asian countries, where Asian universities look very attractive in terms of quality and price. Our competitive advantage attributable to quality is being quickly eroded.

Thanks Jim, all good points. Hopefully our G8 unis can at least successfully market themselves in Asia as a prestige offering compared with their domestic options.

Looks like I underestimated the amount of upstream work arising from the huge expansion of the industry – this certainly is welcome news, let’s hope it continues!

But how long will it continue for though Gene? Gasfield well and pipeline work is capex – and the resource sector has made it clear that it will not be long before it begins sharply reducing capex. It seems to me that the amount of this work still on the drawing board has already been stated in capex intentions.