I’m delighted to present a guest post from my old friend and former Treasury colleague Joe Branigan. It goes without saying that the views presented below are Joe’s and not necessarily mine. That said, I agree broadly with Joe regarding the fiscal reality that will face the new Government.

Fiscal reality will drive the next reform agenda

What a week in Australian politics! And the upheaval is still not over.

It would seem that the most likely election outcome in Queensland is a minority Labor Government of 44+2+1=47, with perhaps Peter Wellington elected Speaker and the two KAPs agreeing to vote on the floor with Labor to guarantee its government.

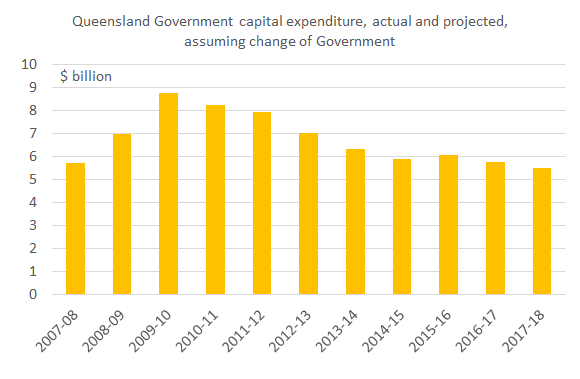

The price of that guarantee will be billions in new capital expenditure in the regions, primarily on roads. Without asset leasing, this money will need to be borrowed. KAPs proposal to defer or cancel the BaT tunnel in Brisbane and the Townsville Stadium won’t help because no money has been allocated to these projects in the current budget’s forward estimates.

And maintaining KAPs new inland highway will cost an additional tens of millions annually, which must be factored into the forward estimates. Without additional borrowing, we are about to see the deferral of infrastructure projects in SEQ that benefit millions of people to fund projects that benefit thousands of people – just imagine how that affects overall state productivity.

Queensland’s fiscal realities will hit the new Palaszczuk minority government like a hammer to the back of the head in a matter of weeks as the Expenditure Review Committee wrestles with Labor’s campaign promises, union demands for more public servants and higher pay rises, and the fact that our royalty revenues and other state taxes are at an ebb through the bottom of the resources cycle. And don’t expect LNG to save us as global supply rapidly expands.

If Labor chooses to put its collective head in the sand, by the 2018 election, state gross debt could again be approaching $80 billion and with the demands of KAP, the public service unions and the Greens (that remember lifted Labor’s primary vote above the LNP’s), it will prove impossible for Palaszczuk to maintain a firm grip on the state’s finances. Remember that the LNP actually cut spending in real terms in its first two budgets and limited the spending increase to just 1.5% in real terms in its third budget, and yet it still did not achieve a surplus in its first term. How Labor could possibly achieve a surplus is a question for greater minds than me.

There will, therefore, be an enormous temptation for Labor to increase taxes, fees, levies and charges, and permanently defer the stepped increases in the payroll tax threshold – anything that can close the gap between spending and revenue. I expect environmental levies to make a comeback (remember the Kate Jones $373 million Waste Levy?) and a new round of climate-change and animal-protection red and green tape to strangle the private sector economy but grow the public service.

But by 2018 the need for reform will be more urgent and more obvious than in 2012-2015. Labor will not deliver a budget surplus in its first term because it will not address the structural deficit that is causing the difference between spending and revenue, and as a result our net and gross debt will rise. Asset sales will again be back on the agenda and central to fiscal and economic reform. The election of a Labor minority government has simply delayed the inevitable by 3 years.

Will the LNP be ready to fight for good policy in 2018? Of course not! The LNP will draw the wrong lessons from its defeat and looks set to throw not only good policies overboard but its chief remaining advocate, former Treasurer Tim Nicholls. While Nicholls will be looked on favourably by history, having achieved the greatest fiscal consolidation since Keating in 1987-88, the next lot of LNP leaders will not.

Under new leadership, the LNP will almost certainly abandon its commitment to fiscal and economic reform and return to the old Nationals/Labor style of big government, industry assistance and barrels of pork. Yet, their quickest way back to government would be to stand their ground on economic and fiscal reform, elect Tim Nicholls as leader who will sell the message clearly and without aggro, and sit back and watch Labor’s magic pudding melt in the harsh Queensland sun.

Joe Branigan is Senior Research Fellow at the SMART Infrastructure Facility and a former Regulator at the Queensland Competition Authority. In an earlier incarnation, he was one of Brisbane’s greatest pizza delivery drivers in the 1990s, and perhaps of all time.