Industry bailouts by governments have been subject to intense debate in this time of coronavirus, including in Australia where the airline Virgin Australia is in voluntary administration and seeking additional financial support from government. Last weekend, I discussed industry bailouts with renowned US economist and commentator Dr Dan Mitchell, Founder of the Center for Freedom and Prosperity and former Senior Fellow at the Cato Institute. Dan regularly appears on Fox News and CNBC and is regularly quoted in the Wall Street Journal and other publications. I am grateful he agreed to appear again on my podcast (Bailouts in this time of coronavirus).

Use these (approximate) timestamps to jump right to the highlights:

- 1:05 – discussion of venture capitalist Chamath Palihapitiya’s view that companies should go bankrupt rather than being bailed out (check out Government should let airlines fail)

- 5:15 – an ostensible libertarian justification for bailouts, the concept of regulatory taking (check out Dan’s post Protecting Airlines and Other Companies from Government Control)

- 7:40 – we need to ensure there isn’t a permanent expansion of government when it’s all over

- 10:00 – discussion of merits of different ways of bailing out companies, after I quoted from a Guardian article US government agrees on $25bn bailout for airlines as pandemic halts travel

- 11:50 – “There are no good options” according to Dan

- 17:00 – is the coronavirus crisis an indictment of capitalism? No, says Dan. Check out Dan’s post Coronavirus and the Tradeoff Between Big Government and Competent Government

- 19:10 – to what extent is the US situation a failure of the federal government versus state governments? Dan thinks the states are best placed to deal with coronavirus

- 25:10 – discussion of what Dan thinks are misplaced concerns about stock buybacks (check out Dan’s post Washington’s Counterproductive Attack on Stock Buybacks)

- 32:05 – discussion of Dan’s Venn diagram in his post Coronavirus, Economics, and Saving Lives

- 34:05 – reference to UN report which acknowledges economic cost of coronavirus containment measures (check out this NPR article U.N. Agency Fears ‘Vulnerable’ Africa May Suffer At Least 300,000 COVID-19 Deaths)

![]()

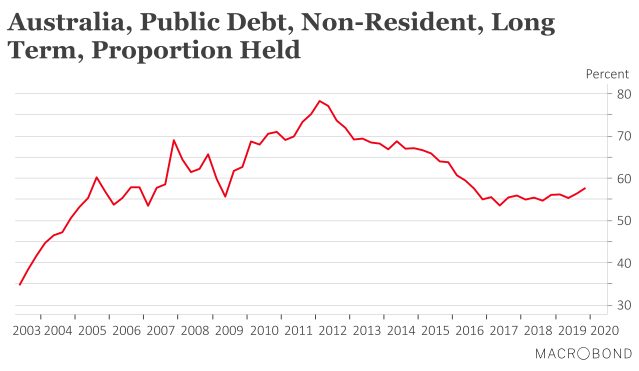

There are currently around $560 billion of Australian Government bonds (excluding short-term Treasury Notes) on issue. In a few years’ time, that figure will very likely be in the order of $1 trillion – i.e. $1,000 billion (see this

There are currently around $560 billion of Australian Government bonds (excluding short-term Treasury Notes) on issue. In a few years’ time, that figure will very likely be in the order of $1 trillion – i.e. $1,000 billion (see this