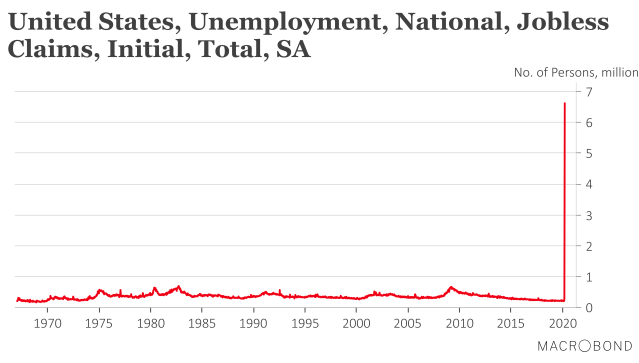

It is hard to overstate how rapidly economic conditions are deteriorating in economies affected by coronavirus, most particularly in the United States, which is seeing hitherto unbelievable numbers of people filing for unemployment benefits (see chart below). The 6.6 million claims last week was twice the previous record of 3.3 million, which was set the week before, and which was already an unbelievably high number, 10X the number from the week before that one. So that’s around 10 million additional Americans unemployed in two weeks, although it’s unclear how many jobs are gone for good and how many workers have just been furloughed or stood down for a temporary period, as Jason Furman has noted (Obama economist: Lessons from the 2008 crash). It’s been observed by US commentators that the increase in US unemployment over the last two weeks is broadly equivalent to the increase which took six months to occur during the Great Recession in the late 2000s.

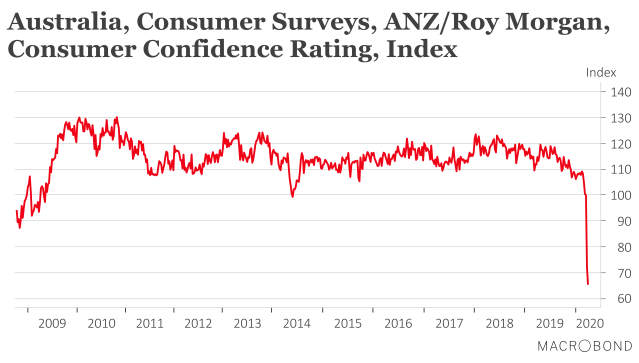

We are seeing a rapid real-time demonstration of the Keynesian multiplier, as the initial direct shock from coronavirus ripples through the economy, with reductions in aggregate output and income leading to lower spending, leading in turn to lower output and income, further reducing spending, and so on, in a cumulative process. The huge amounts of government support being provided to both the US and Australian economies will mean they should soon find a floor and we should avert a re-run of the Great Depression, but the US unemployment rate is widely expected to now be at least 10% and will probably get even higher still before this is over. There’s little doubt we’ll end up with a 10%+ unemployment rate in Australia. Certainly, consumer confidence has plummeted (see chart below).

It looks like we may learn today just how much money the Australian Office of Financial Management (AOFM) will need to borrow each week to pay for the coronavirus rescue measures and to make up for lower revenues, based on an article (Can the bond market pass the $300b test?) in the Financial Review:

Soon, the government’s debt management agency, the Australian Office of Financial Management, will reveal just how much it intends to borrow to fund the coronavirus response. The estimate is that an additional $300 billion of bonds will have to be sold over 15 months.

That is, the AOFM will need to increase its weekly bond sales from $1.2-1.6 billion to $4-5 billion. Will this mean Australia loses its AAA credit rating? Possibly, although even with this additional debt we’ll still be in a better position than many other OECD economies. The big problem with debt is the interest bill, which, while manageable at the low interest rates we’ve seen, could become hugely problematic in future years if the AOFM ends up having to refinance large amounts of debt at higher interest rates in the future.

I chatted about how the AOFM borrows money on behalf of the Australian Government with Steve Austin on 612 ABC Brisbane on Tuesday afternoon (from 2:41:00). Incidentally, I expect the Queensland Government is also facing a huge funding challenge, and I wouldn’t be surprised if it has been lobbying the Australian Government for assistance with its borrowing program, as it did during the financial crisis, a story I tell in my 2018 book Beautiful One Day, Broke the Next.

Gene

Great post. Apart from the obvious impacted sectors (tourism and travel, retail, education services etc.), have you come across any analysis on a broader suite of sectors and / or regions impacted yet? Some regions in Queensland will surely be more vulnerable than others.

I suspect this is the first time in a very long time that being in an agriculture-dominated region like the Burdekin, Bundaberg or Lockyer Valley will be an advantage. Those regions will not face such a hit from the current health-related restrictions due to lower reliance on worst-hit sectors, and they will have sustained demand for their dominant outputs anyway (we still have to eat!). Furthermore, their service sectors are both small and largely reliant on local demand, so they should recover quicker once restrictions are lifted.

Rather than being the ‘Sunshine State’, we might need to rename Queensland the ‘Pockets of Sunshine State’.

Thanks Jim, yes, I agree some regions will fare better than others, and will try to cover that in future posts. That said, it will be different degrees of bad news I expect.