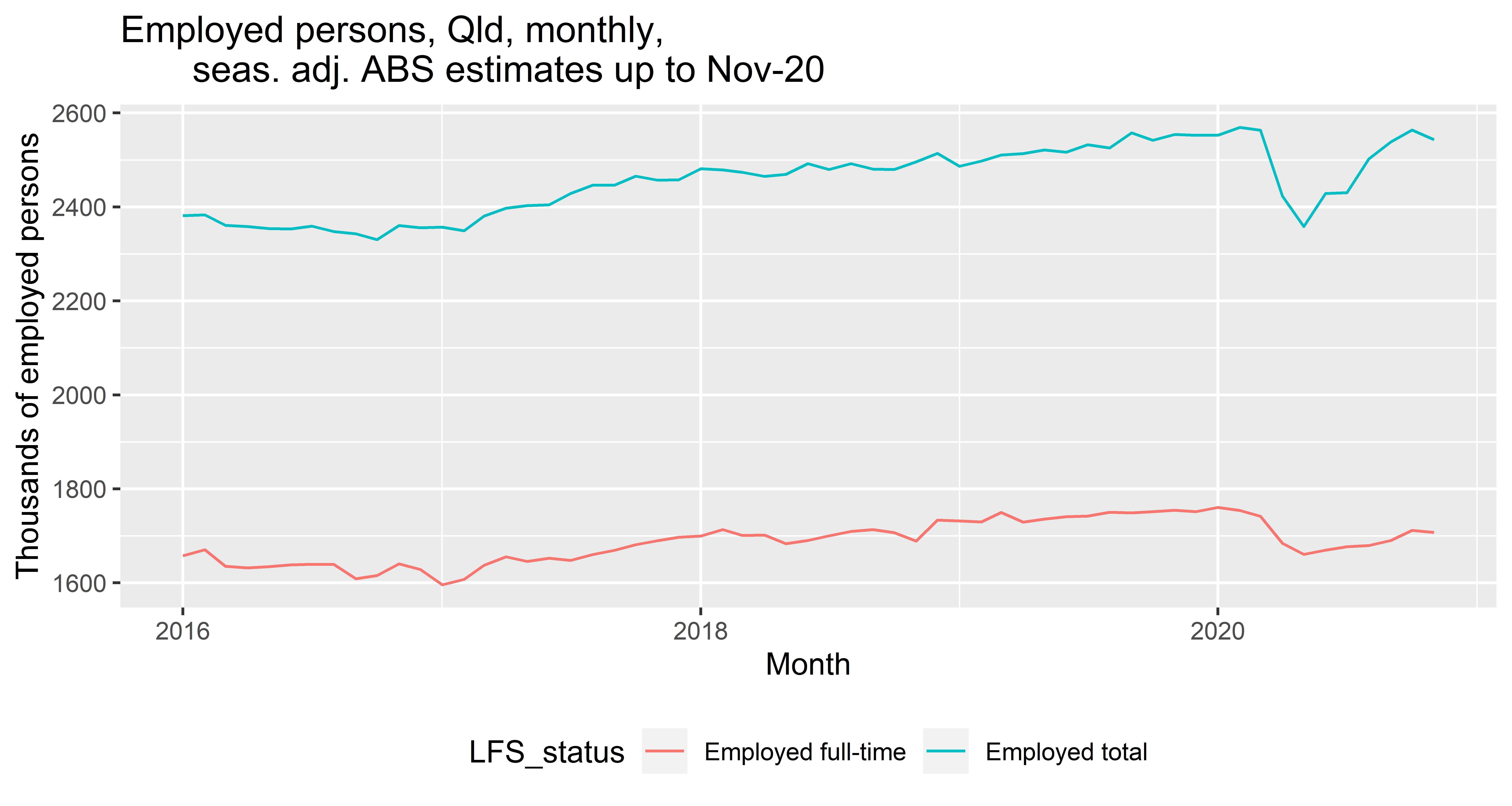

Last month, I dissected the Queensland Treasurer’s bold claim that more Queenslanders are working now than were working pre-COVID (check out my 21 November post). I thought it was a bold claim given a) the substantial sampling error at the state level in the ABS Labour Force Survey data and b) that the claim wasn’t supported by the payroll jobs estimates also published by the ABS. So I wasn’t surprised when the November Queensland employed persons (seas. adj.) estimate came in below the March level (see chart below), destroying the Treasurer’s claim last month that “Queensland is the only state in Australia that has put back on every single job lost since the lockdowns started in March”. Based on the November data, we’re 20,000 jobs down on where we were in March and our state unemployment rate is 7.7% compared with a national average of 6.8%.

As I usually say when commenting on the Labour Force data, don’t read too much into month-to-month movements, so we shouldn’t necessarily conclude that the recovery was derailed in Queensland in November. The October employment figure the Treasurer was overly excited about was obviously an over-estimate and the November estimate represents a correction to that.

The economy has definitely been recovering and there are several positive indicators, particularly around consumer and business confidence. Of course, there are risks to the economic outlook, including, most obviously, the potential re-imposition of interstate travel restrictions in response to the Sydney northern beaches COVID cluster. Furthermore, a good deal of the restored confidence is likely related to high levels of government support, which can’t last forever (check out my post Aussies over-confident after being over-compensated by Gov’t for COVID-recession).

Finally, check out Pete Faulkner’s post for some excellent analysis of the data:

When I recorded the latest episode of my Economics Explored podcast last Friday afternoon, the price of one Bitcoin was a bit above US$18,000 after having failed to get beyond US$20,000 in the previous weeks. In my chat with my friend Tim Hughes, I said who knew what it would end up at when the episode was finally released. Well, it turns out that the price of one Bitcoin has finally gone beyond US$20,000 (check out this Coindesk report).

The US$20,000 Bitcoin price is the latest illustration of the Greater Fool Theory. If you’re buying Bitcoin at this price you’re speculating/gambling you’ll find a greater fool who’ll buy it at a higher price. Coindesk suggests there could be a lot of greater fools out there:

Breaking above $20,000, which represented a significant hurdle in the mindset of most traders, is entirely new ground for bitcoin and opens the doors for a climb to $100,000 over the course of 2021, according to some.

This is not investment advice. Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

Many Queenslanders would have been terrified about the possibility of a re-imposition of border restrictions when they learned about the new NSW community-acquired COVID case, but, thankfully, Acting Premier Steven Miles has told us all is good for now, and he’s confident NSW has it under control, according to this news.com.au report. But what if it doesn’t, and we see more cases? Will the Government lose its nerve and slam the border shut? Based on previous form, quite possibly.

Arguably, our current predicament is best approached with stoicism. The modern evangelist of stoicism Ryan Holiday has co-authored a new book Lives of the Stoics: The Art of Living from Zeno to Marcus Aurelius, which is the ideal book for 2020. I just wish it was released earlier in the year. The book surveys the lives of the 26 leading thinkers of the Stoic philosophy in the Classical world, philosophers such as Zeno and Seneca and men of action imbued with Stoicism such as Roman Emperor Marcus Aurelius and Senator Cato the Younger. The authors show us how the Stoics generally (and not always) lived up to the values of the philosophy: Courage, Justice, Moderation, and Wisdom. Those are qualities that we’ve definitely needed in 2020.

Lives of the Stoics by Ryan Holiday and Stephen Hanselman. If you’re in Brisbane, you can pick up a copy at Dymocks on the Mall.

While, in Australia at least, 2020 in no way compares to those awful years of Depression and War endured by my grandparents’ generation, it undoubtedly is the hardest year many of us have had to live through, and we’ll be glad to see the end of it. What really shocked me this year is how willing governments have been to impose severe restrictions on our way of life for so long and, in some cases, such as the second round of Queensland-NSW border restrictions, with so little justification. Sure, arguably many restrictions were for the greatest good of the greatest number, but we’ve placed a lot of trust in the wisdom and moderation of our public officials. Occasionally, I’ve worried that trust was misplaced (e.g. see my 11 September post).

Arguably, the restriction on allowing Australians to travel overseas is excessive and it’s good to see Andrew Cooper through his LibertyWorks think tank is challenging its legality, as reported by the Guardian Australia: Rightwing thinktank launches legal challenge to Australia’s travel ban. Yes, I know we’re in a pandemic and COVID is a serious disease, but I think it’s important someone stands up for civil liberties in a year when we’ve been very willing to sacrifice them for what our officials perceive is the greater good.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

Prime Minister Scott Morrison did a good job yesterday at putting China’s reported ban on Australian thermal coal into perspective, pointing out Japan is our largest customer for thermal coal, and it takes twice the amount of thermal coal as China. Check out the PM’s comments on Sky News: Coal added to industries China ‘has crippled through sanctions’. Also worth checking out is this excellent ABC video which notes 16% of Australia’s $26 billion of annual thermal coal exports go to China, which is approximately $4 billion nationally: What’s at stake if China bans Australian coal? The ABC, which has obviously spoken with industry representatives, suggests there is a good chance the rejected thermal coal can be sold into other markets, mitigating the potential loss.

What’s the potential impact on Queensland? From Queensland coal industry statistics published by the state government we know that Queensland exported 61 mega tonnes of thermal coal in 2019-20 compared with 152 mega tonnes of coking coal (check out Total coal exports by coal type). Unfortunately, the government doesn’t appear to publish a cross-tabulation of exports by coal type and country of destination.* But we know that, in 2019-20, 42 mega tonnes out of a total of 213 mega tonnes of all types of coal, were exported from Queensland to China, or 52 mega tonnes if you include Hong Kong (check out Coal exports by country). A straightforward estimate of thermal coal exports to China (including Hong Kong) would be the share of total coal exports going to China of 24% x 61 mega tonnes of total thermal coal exports, giving approximately 15 mega tonnes of thermal coal going to China. But what if a higher proportion of China’s coal imports are thermal coal than the proportions for other countries? If half of Queensland’s coal exports to China were of thermal coal, we’d be talking 26 mega tonnes.

Let’s use 15 to 26 mega tonnes as a range for Queensland’s annual thermal coal exports to China in the absence of actual data. Using the Queensland Budget forecast thermal coal price of A$94/tonne (approx.) we get an estimate of the total value of thermal coal exports to China affected by the ban of $1.4 billion to $2.4 billion. Applying a royalty rate for coal of 7%, as per the Business Queensland website, we get a potential annual loss to the state budget of $100 million to $170 million if our coal exporters can’t find alternative customers, a reasonable amount of money but not a devastating loss. I should note there may also be impacts on other tax revenues if coal production is cut back and jobs are lost. If anyone has superior data or information that would improve these estimates please let me know in the comments.

The impact would be much worse obviously if the more valuable coking coal exports were also affected, so we’re lucky the ban apparently only applies to thermal coal at this stage.

All said, the ban is unwelcome and comes at a bad time, when the Australian economy is recovering from the COVID-recession and the Queensland state budget, like budgets for other states, is already heavily in deficit.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

*Update: since posting this on Tuesday 15/12/20 I’ve learned that the Government does actually publish quarterly data by country and coal type. The data, however, aren’t 100% complete (i.e. not all mines have reported) and are subject to revisions, as noted in the workbook. The current estimate in the data set of thermal coal exports to China for 2019-20 of a bit under 10 mega tonnes (and under $900M of value) looks low to me. For instance, in 2018-19, Queensland exported 16 mega tonnes of thermal coal to China and, in 2017-18, exports were 21 mega tonnes. Possibly the drop in 2019-20 was due to greater reliance on domestic coal by China which has been Chinese Government policy, or it could be an issue with the data. I’m going to look more into this over the next few days and will post again on it in the future. If thermal coal exports from Queensland to China are only running at around 10 mega tonnes per annum then the royalties loss from the latest ban may only amount to $60-70M per annum.

We’ve seen some impressive rainfall in Brisbane over the last few days, but it appears parts of the state such as Warwick which really need it can do with a lot more to fill dams and help them get over the drought. A headline on the Warwick Daily News site reads “Farmers face new battle as hopes for big rains dashed”.

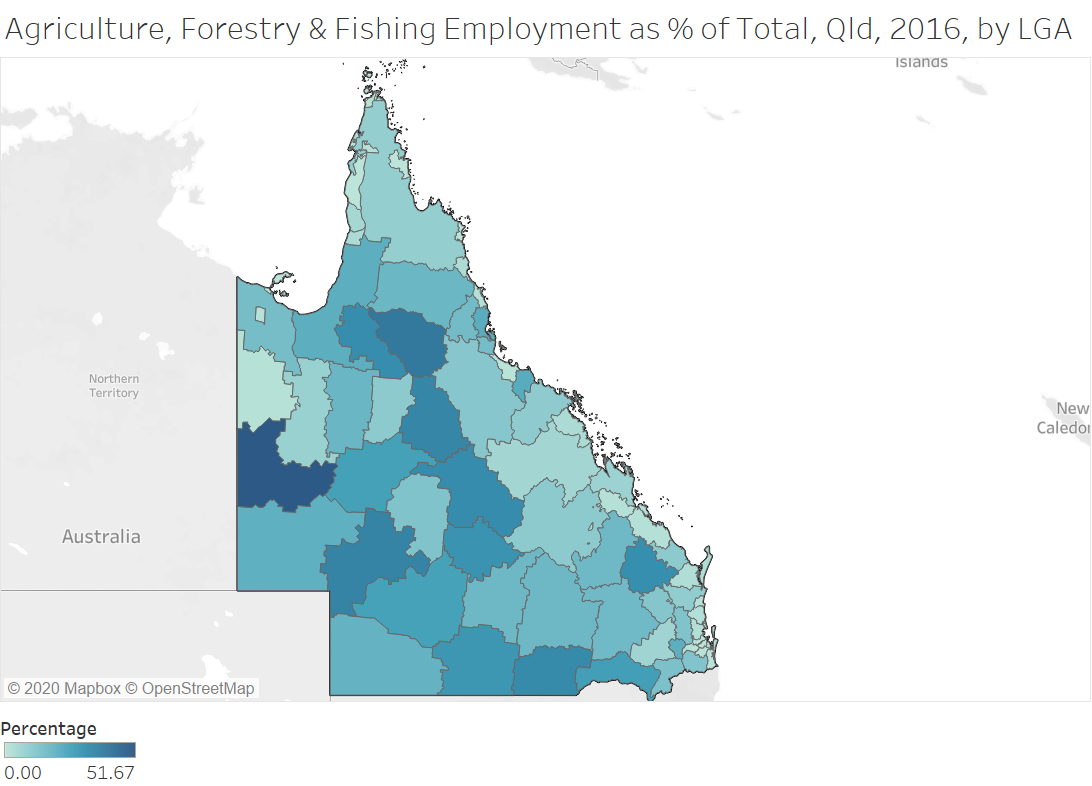

Let’s hope there’s much more rain to come for our farmers. An interview I saw on ABC News Breakfast with a Southern Downs community leader this morning reminded me of the importance of agriculture, and hence water, to so much of regional Queensland (check out the thematic map below based on 2016 ABS Census data accessed via the QGSO’s excellent Qld Regional Database).

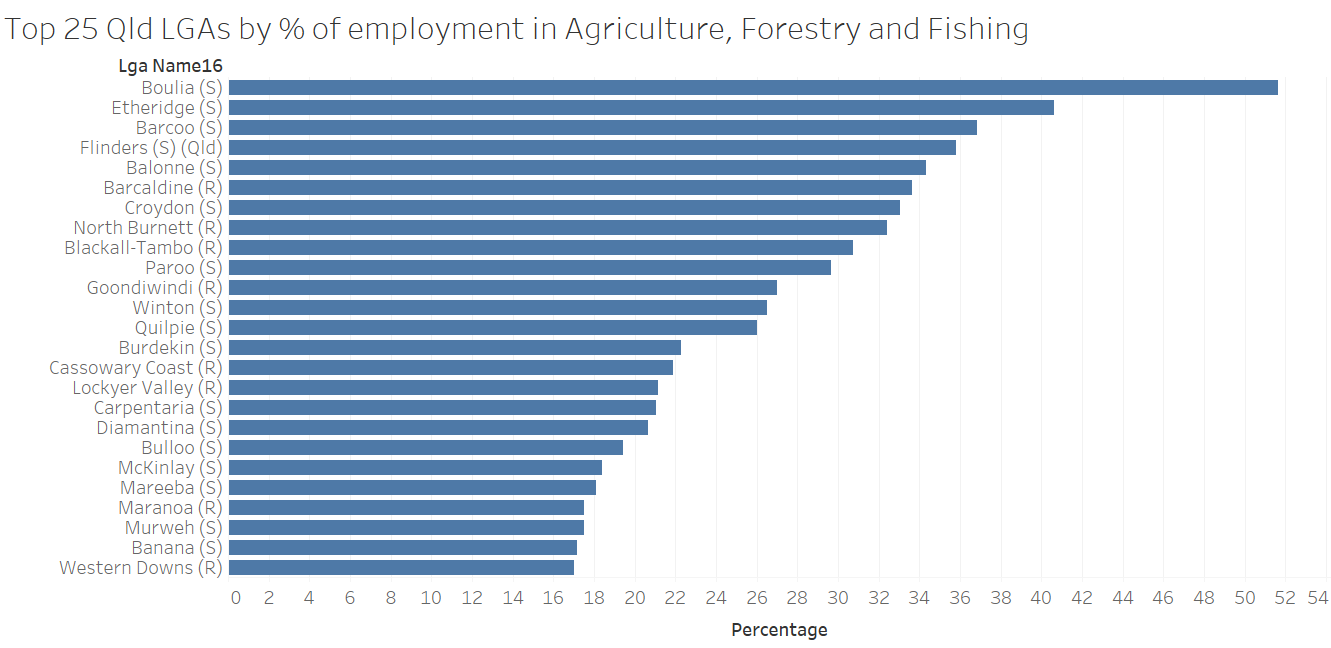

The Local Government Area (LGA) with the highest percentage of employed persons working in agriculture is Boulia, a small community (with fewer than 500 residents) out on the Qld-NT border which specialises in cattle (see chart below).

The 25 LGAs with the smallest relative contributions from agriculture all have fewer than 2% of total employed people working in agriculture (see chart below). Those of us in the city need to be conscious we don’t forget about the importance of agriculture to our regional economies, and we should hope for further rain to water crops and help fill regional dams.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

Two UQ geographers have written a great Conversation article, republished in the Brisbane Times, on Why city policy to ‘protect the Brisbane backyard’ is failing. The authors argue that current planning policies lead to undesirable outcomes. Current Brisbane City Council policies include a preference for low-density infill (i.e. sub-dividing a block and sticking another house on it), a townhouse ban in single home precincts, and heritage protection of old Queenslanders. One perverse outcome of current policies is that, despite the objective of the Council to preserve green space, there is now less green space in Brisbane suburbs as suburban blocks are subdivided and new detached dwellings are crammed into the new lots. Here’s the summary of the implications of existing policies from the authors Rachel Gallagher and Thomas Sigler:

While low-density infill may balance consumer preference for detached houses with meeting infill targets, it in effect creates a “compressed suburbia”. The results fail to deliver on the core promises of consolidation policy, including greater housing diversity and affordability, and a halt to urban sprawl.

It also leads to a dichotomy of new dwellings: high-rise apartments or detached houses. We found very little development of medium-density dwellings.

This is a real shame as medium-density development is probably the best way to meet the housing needs of Brisbane’s population while maintaining highly liveable neighbourhoods. On the potential benefits of medium-density development in Brisbane, I’d recommend an excellent essay by Tony Hall in the volume A Climate for Growth, which I commented on in one of my earliest QEW posts Planning for the 200-kilometre city.

In my view, it would be desirable to remove both the townhouse ban and heritage protection of old Queenslanders to allow more medium-density development in Brisbane.

In inner Brisbane, new residential development is either apartment towers in commercial/light industrial areas or detached dwellings on small sub-divided blocks, rather than more desirable medium-density options.

The Bitcoin price was getting close to US$20,000 at the end of last month, but has since come down to a bit over US$18,000. In March, it was around US$5,000 (see chart above). There has been a lot of speculative money going into Bitcoin, driven partly by the Fear of Missing Out (e.g. check out The Wealthy Are Jumping Into Bitcoin as Stigma Around Crypto Fades and Tyler Winklevoss: ‘Smartest people in the room buying the Bitcoin quietly’). Bitcoin is also seen by some as a hedge against future hyper-inflations (as governments resort to Modern Monetary Theory) and political chaos (e.g. check out Naval Ravikant’s latest interview on the Tim Ferriss Show). I have come to think that a fundamental breakdown in civilisation would actually be required for Bitcoin to become useful as money, but then you’d have to wonder what would guarantee the internet would function and Bitcoin would be a reliable means of payment.

Bitcoin can’t really become a useful form of money if its value is so volatile, as most people would be reluctant to set prices or write contracts in Bitcoin. The cryptocurrency faces a huge challenge in supplanting traditional currencies, which benefit from a lock-in effect. In his brilliant 2016 book Macroeconomics in Times of Liquidity Crises, renowned Argentine-American economist Guillermo Calvo nicely explains why money has value, even though it is no longer backed by a commodity such as gold. Calvo suggests it has to be much more than the fact that government require tax liabilities to be paid in fiat currencies, and he writes (pp. 28-29):

An explanation that has been largely ignored by the profession and that I find very appealing—although admittedly incomplete—was proposed in Keynes’s General Theory. He writes: “the fact that contracts are fixed, and wages are usually somewhat stable in terms of money, unquestionably plays a large part in attracting to money so high a liquidity-premium”…

…the PTM [Price Theory of Money] asserts that money’s output value cannot be nil in equilibrium because economic agents set several key nominal prices/wages in advance, thereby offering a ground-up output guarantee to cash.

That strikes me as incredibly insightful and shows the huge barrier that Bitcoin and other cryptocurrencies need to overcome. To have true value as money, prices, wages, and contract values will need to be enumerated in Bitcoin (or some other cryptocurrency). At the moment, anyone who tried to specify a Bitcoin price for a commodity or asset in advance would be engaging in highly risky speculation. Unfortunately for Bitcoin, this means it won’t end up with a reasonably stable value and its price will continue to swing wildly as it is merely a plaything of speculators.

We’d need to see an outbreak of hyper-inflation, which looks unlikely at the moment given the state of the global economy, and possibly widespread political chaos, for Bitcoin to become widely adopted and to have any real value as a money in my view.

For more on Bitcoin, I’d recommend John Quiggin’s 2018 blog post Bitcoin’s belated bust. While Bitcoin has surged in value since John’s post, I think the points he makes about the problems with Bitcoin are still apposite.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

As a Queenslander who grew up during the days of Sir Joh, I’ve come to expect a certain level of impropriety in Queensland politics, so I haven’t been surprised governments since Sir Joh’s have had questionable dealings, although they’ve been of a lesser magnitude than what we saw in the 1980s I should note. This week we’ve learned more about the proximity of two prominent lobbyists to the highest levels of government, as I noted in my post Special deals can be bad deals for Government – my comments in today’s Courier-Mail re. Maryborough trains contract. The Premier’s granting of a $600M+ contract without any competitive process was extremely bad form, and I thought it would be worth noting the Queensland Competition Authority noted in its excellent review of industry assistance in 2015 that such deals were not in the interests of Queenslanders. Here are the relevant excerpts, for the record (from p. 309):

While much of the activity under Queensland Government procurement policies and programs focuses on improving value for money, some activity may result in the preferential treatment of local businesses, thus providing industry assistance.

Procurement policies reflect the ongoing tension between the desirability of achieving value for money in procurement and longstanding pressures for policies which preference local industry…

…Preferential procurement policies can protect local businesses from international competition, increase procurement costs leading to higher taxation, and disadvantage businesses with higher productivity. Even if preferences support the expansion of those businesses supplying government, they do so at the expense of other businesses and lower household incomes…

…Public sector procurement decisions should be guided by a single objective — achieving value for money in procurement. Broader economic, social and environmental objectives are best addressed through other policy instruments.

Basically, the QCA’s words suggest the Premier’s announcement, during the election campaign, of a $600M+ contract for Downer to build trains was bad policy. But, hey, this is Queensland, and, if you’re a client of a lobbyist on our side, how can we help?

I acknowledge we have nowhere near the rot we did in the eighties, but we clearly need to improve standards of governance in Queensland based on recent news.

The latest episode of my Economics Explored podcast considers the emerging field of behavioural finance, which is basically the application of behavioural economics to finance. It considers lessons from this field for households, investors, and governments. The episode features an interview I conducted earlier this week with Dr Tracey West of the Griffith Business School.

Tracey teaches behavioural finance to undergraduates and postgraduates at Griffith’s Gold Coast campus. She’s also an active commentator on economic policy issues. For instance, last year, Tracey wrote an excellent Conversation article on 3 lessons from behavioural economics Bill Shorten’s Labor Party forgot about, three lessons which Tracey and I consider in our conversation. Those lessons are:

1. People are loss averse

2. Limited decision-making

3. Now is worth more than later (and much more so than economists would typically assume using typical discount rates).

Tracey and I had a great discussion about behavioural finance theory and practice, including the need for regulation of financial markets and investments. The Storm Financial collapse, which wrecked the finances of many North Queenslanders, was given as an example illustrating the need for regulation of financial investments. I hope you enjoy our conversation. A transcript is available via my business website.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com

Today we learned that, as Reuters reports, Australia consumer sentiment hits 10-year high (see chart above). This is despite Chinese trade restrictions and the looming insolvency tsunami in the new year and the fiscal cliff in April 2021. Sure, given we’ve crushed COVID in Australia and a vaccine is on its way, there are reasons to be confident, but both consumer and business confidence figures look too high to me, all things considered. So, what’s going on?

The most likely reason for buoyant confidence is that Australians have been over-compensated by the federal government for the COVID-recession, via JobKeeper and the JobSeeker coronavirus supplement. Future historians and economists will look back and wonder what led a notionally conservative government to bring in such massive support measures. But let’s leave the debate over whether such measures were necessary and desirable to a later time. Let’s just review their impacts by considered data from the September quarter National Accounts released by the ABS last week.

First, check out the spike in social assistance benefits to households this year (chart below).

Second, check out the boost in profits of incorporated businesses, partly due to JobKeeper, after an initial fall in the March quarter (chart below).

Third, check out how Gross Mixed Income, largely of the self-employed and sole traders, has been juiced up by JobKeeper (chart below).

Fourth, understand the consequences of all this assistance are continued growth in household incomes despite COVID (see chart below)…

…and a big pool of savings (see chart below) which consumers will be able to spend over Christmas and in the New Year. It’s certainly been the most unusual recession we’ve ever seen.

Please feel free to comment below. Alternatively, you can email comments, suggestions, or hot tips to contact@queenslandeconomywatch.com