Last month, the Federal Treasurer and Queensland Premier argued over their respective roles in luring the Aquaman film production to the Gold Coast (see news.com.au article). In monetary terms, the Federal Government made the greatest contribution by far, with $22 million in tax breaks offered to the film production. The beneficiaries are the highly profitable US companies DC Comics and Warner Bros, which are the producers of Aquaman.

The tax break the production will receive is called the Location Tax offset, which for Aquaman the Commonwealth has bumped up to 30 percent from the usual 16.5 percent applied to production expenditure within Australia. The Commonwealth will pay the Aquaman producers $22 million, less whatever tax is owed by them for profits booked to the Australian operation.

The Queensland Government has not disclosed any financial contribution, but its media release notes:

“The Palaszczuk Government, through Screen Queensland, has invested an extra $30 million over four years to continue to attract large-scale film and high-end television productions to Queensland to increase jobs and expenditure into the State’s economy.”

So the Queensland Government may have provided a sweetener to attract the production, possibly as a rebate of payroll tax. The production will also benefit from the use of a large sound stage at Village Roadshow Studios on the Gold Coast that, oddly, the Queensland Government covered the bulk of the costs for: $11 million out of a total cost of

$15.5 million (see this media release for details). Sure, it will be used during the Commonwealth Games, but Village Roadshow will derive the bulk of the benefits from the sound stage over its life.

Given all this special assistance to the film industry, we should ask what justifies the industry getting such special treatment. Is it merely because of the glamour of Hollywood, the opportunity for politicians to appear on location or on the red carpet with movie stars? Or is there is a genuine benefit from an economic perspective?

Consider first that the Queensland Premier did make an important point in her attempt to claw back some of the credit from the Federal Treasurer for luring the production, noting in the Queensland Government media release:

“Australia doesn’t have a competitive tax system.”

I suspect the Premier was referring to the competitiveness of our tax system in relation to international film productions specifically, but her point is of broader applicability. Indeed, business groups and the Australian Treasury have been saying Australia’s tax system is internationally uncompetitive for years, and our uncompetitive tax system is the motivation for the Government’s proposed reduction in the company tax rate from 30 to 25 percent.

But why should the film industry, and particularly an international film production where the bulk of the profits will be repatriated overseas, get special treatment? Why not provide broader tax relief?

Let us consider the arguments typically advanced by film industry advocates. First, it is argued the film industry deserves special treatment because it creates jobs, directly and indirectly. Second, it is argued that government support is needed in the early stages to get the industry going, so it can reach a critical mass, an infant industry argument for public support.

The jobs argument is subject to a number of problems. It is typically very expensive for the government to create jobs. In this case, the $22 million tax break amounts to $22,000 to $37,000 for each of the 600 to 1,000 (temporary) jobs estimated to be supported by the production. And the Gold Coast does not appear to be suffering from an unemployment problem. The Queensland Government Statistician’s office estimates an average unemployment rate for the Gold Coast of 5.6 percent compared with the State average of 6.1 percent in the 12 months to November 2016. Other problems with the jobs argument are that, as noted above, the jobs are only temporary, many of the people getting the temporary jobs had other jobs anyway, and, based on the experience with Thor: Ragnarok, many of the jobs are typically not well paid and not as many jobs end up created as expected. CGI means that film productions need fewer people nowadays (see this Gold Coast Bulletin report).

Regarding the infant industry argument, that the industry just needs a hand up in its early days until it becomes self-supporting, we tried that over six decades with the car industry and it did not work, unnecessarily costing taxpayers billions of dollars in the failed attempt. Typically, infant industries do not reach adulthood.

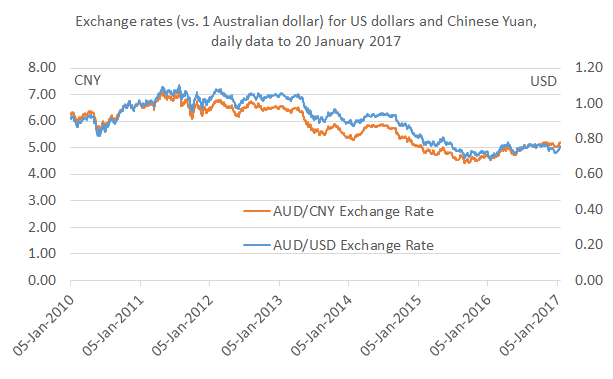

While we have the occasional flurries of meaningful foreign film production expenditure in Australia, these are not long-lasting, as we typically only have a chance of attracting big budget international productions when the exchange rate is low, such as it was in the late 1990s and early 2000s (Chart 1). Even though the Australian dollar has fallen from around parity with the US dollar during the mining boom, currently our exchange rate at 73 US cents is still significantly higher than it was in the late 1990s and early 2000s, when it was in the 50 to 60 US cents range. Hence governments have had to dial up the incentives to attract Hollywood productions such as Aquaman, Thor: Ragnarok and Pirates of the Caribbean 5.

Chart 1: Foreign film production spend in Australia and exchange rate

Source: Foreign production spend data available from Screen Australia.

It does not make sense for our governments to pick winners and losers, but that is what they are doing when they extend special tax breaks to the film industry. Instead of having special tax breaks for the film industry, we should focus on getting our tax and regulatory policy settings right, so we can attract foreign productions without having to offer special rates for special mates.

My previous posts on the film industry include:

Ragnarok in Brissywood

International film productions such as Thor: Ragnarok unworthy of Qld taxpayer support

Also see my ABC Drum opinion piece:

Taxpayer money wasted chasing film productions