John McCarthy had a very good opinion piece in yesterday’s Courier-Mail on the “Sorry tale of the great Queensland divide”, in which he contrasted SEQ’s relatively strong economic performance with weakness in many regions, an issue which I frequently commented on last year. John observed:

“Right now, Brisbane is booming. It really doesn’t get much better for the capital…Brisbane and the southeast have dragged the state into a third straight quarter of increased economic activity.

But rural and regional Queensland is a disaster. That’s not hyperbole, it’s real, and it’s due to a combination of factors, ranging from the lasting effects of the drought to commodity prices, poor infrastructure development, and the collapse of mining investment.”

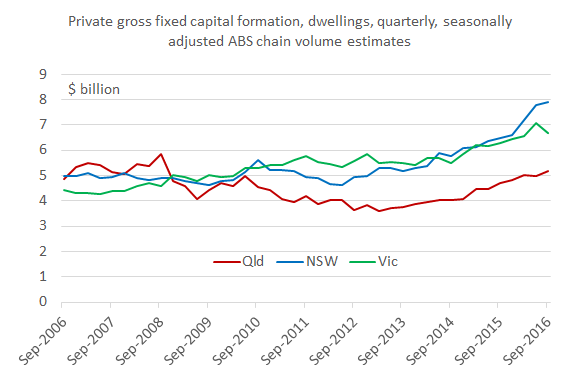

SEQ’s relatively strong performance in recent years has been due in part to a residential construction boom, but this is unlikely to continue given the already huge additions to housing supply we have seen.

The HIA has forecast that residential construction activity will decline in Australia in the next few years, after having peaked in 2015-16 (see MacroBusiness coverage from last August). Residential construction has already started detracting from economic growth in Victoria, and NSW and Queensland may soon follow (see chart below).

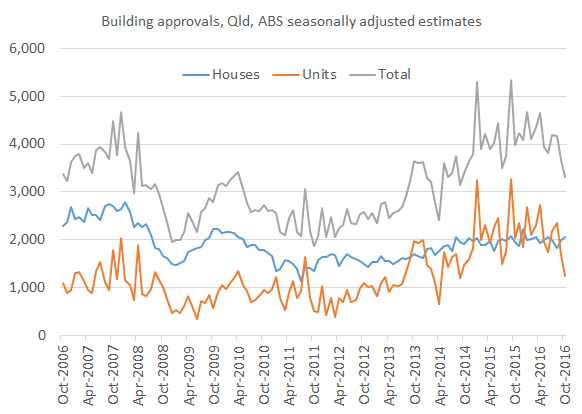

Certainly, building approvals in Queensland for units have fallen in recent months, while approvals for detached houses have remained stable at around 2,000 per month (see chart below and also Pete Faulkner’s post Building approvals down on units).

Queensland Treasury itself flagged the risk to residential dwelling investment on p. 19 of the Mid Year Fiscal and Economic Review 2016-17 released last month:

“The current momentum should see dwelling investment continue to grow at a strong pace in 2016-17. However, the high number of apartments being completed in South East Queensland, as well as tightening in lending practices, may limit growth in dwelling investment in 2017-18 and beyond.”

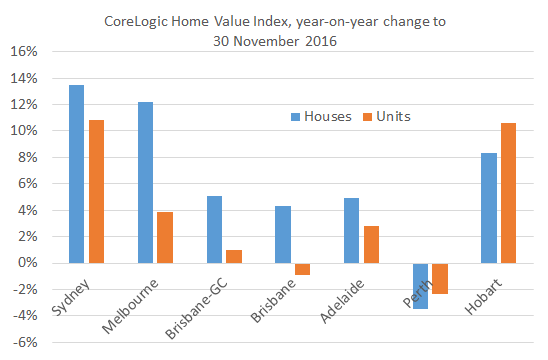

The adjustment of SEQ’s property market and building construction industry to the supply shock will be an important economic development to watch over 2017. Recent data show the adjustment has already begun. CoreLogic’s most recent Hedonic Home Value Index report showed a decline of 0.9 percent in the value of units in Brisbane over the twelve months to November last year (see chart below).

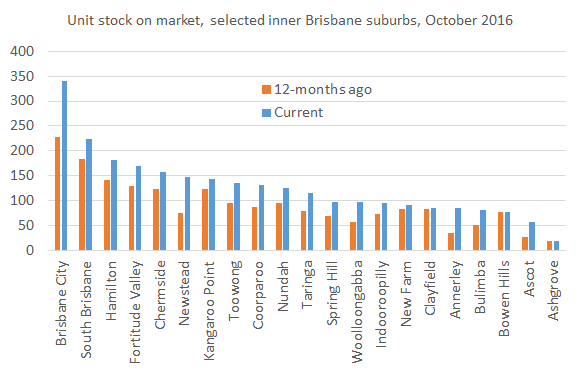

The decline in the value of Brisbane units is unsurprising given the very large increases in stock on the market, particularly in inner city Brisbane, as new apartment buildings have been developed (see chart below based on data reported in the January issue of Your Investment Property magazine).

It will be important to continue to monitor these trends over 2017, as I suspect there is much more market adjustment to come.

Gene

Great article, but I think many of the economic commentators need to put the current situation into perspective. Looking at charts for a couple of years (or even 10 years) can provide some pretty misleading conclusions and lead to some pretty questionable Government intervention. Isn’t it important to put things into perspective?

For our friends in regional Queensland: commodity prices for sugar and beef continue to be above longer-term averages, which should have increased the rate of recovery from the drought; rainfall has been back around long-term trends for a while in most places; the entirely predictable downturn in mining construction activity means that the agriculture sector is no longer squeezed out of capital and employment markets, and: tourism had picked up on the back of a falling AUD. Bottom line is that regional Queensland has now returned to normal after two major anomalies (drought and the mining construction boom). No case for Government intervention.

In SEQ, the rate of job growth in recent years has been significant, and higher than regional Queensland (even accounting for the mining construction boom). While there is a focus on declining dwelling approvals in economic commentary, they are still above longer-term averages. Bottom line is that SEQ has now returned to normal after two major anomalies (property boom and the mining construction boom flow-on). No case for Government intervention.

There is currently a lot of lobbying by vested interests (particularly the construction sector) that will provide a sugar hit to private economic activity (more roads to nowhere, or dams anyone?). But will this simply create a long-term public fiscal hangover, and reduce Government’s ability to react when they really need to? Time to ignore the faux economic crisis and get some perspective…

Many thanks, Jim. Very good points, particularly about the dams! There is also one odd proposal about a new Northern Australian rail line floating around. Regarding regional Queensland, I agree we shouldn’t be providing sugar hits. We need to accept that structural change is affecting regional economies and it’s undesirable to throw money at trying to offset the inevitable decline in many cases.