At the Guardian, Gareth Hutchens criticises some market economists for their forecasts of a correction in house prices in 2016, while house prices in Sydney and Melbourne actually grew at double-digit rates. Market economists Saul Eslake and Stephen Koukoulas have attempted to explain the divergence between their forecasts and outcomes by referring to unexpected RBA cash rate cuts and higher than expected population growth, among other factors. I would suggest they should have simply said the market has stayed irrational longer than they expected.

What we are seeing in Sydney and Melbourne is a property price bubble, in which a mania has gripped property buyers. This type of mania afflicts markets from time-to-time, and we should not think we are immune to it in Australia. Famous historical examples of market manias are the Dutch tulip craze, the South Sea bubble, the US stockmarket before the 1929 Great Crash, Tokyo real estate in the 1980s, and the US housing market before 2007-08. In Sydney and Melbourne, we now have property markets dominated by a mixture of speculators and people gripped by a fear of missing out, people who want to buy a property before it becomes even more ridiculously over-priced.

The mania could continue so long as people can access cheap debt and can meet mortgage repayments, but eventually constraints will be reached (or possibly rationality will prevail) and price growth will stop. And we will see a re-evaluation by the market of property prices, particularly given price growth has been massively ahead of the growth in rents. The most recent CoreLogic Hedonic Home Value Index report (available for download from CoreLogic) notes:

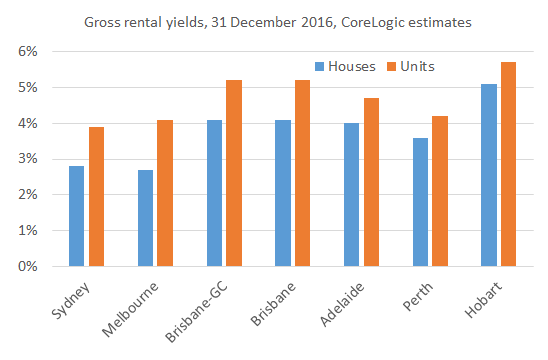

“Over the growth cycle to date, Sydney dwelling values are up 69% while rents have increased by approximately 10%; this has caused the gross dwelling yield to fall from 4.5% in June 2012 to the current record low of 3.0%. Similarly, in Melbourne, dwelling values are 51% higher over the cycle to date, while rents have risen by a much lower 9.6%. The divergence between dwelling value growth and rental growth has compressed Melbourne’s gross yield profile to a new record low of 2.9% from 3.8% in June 2012.”

Gross rental yields as low as this in Sydney and Melbourne are unsustainable (see figure below). Generally, they would only be tolerated by an investor who expects a large capital gain in the future. But the likelihood of that diminishes every time current property prices reach even more unsustainable levels.

In a rational market, there should be a close link between property prices and rents, as rent signals the market value of the services provided by a property. Of course, low interest rates are relevant, and perhaps investors are coming to accept lower returns generally, but why should Sydney and Melbourne property investors accept much lower yields than those in other markets?

The massive divergence between the growth of property prices and rents is a big clue that the Sydney and Melbourne property markets are very likely suffering from irrational exuberance.

Gene

I’m no macroeconomist, but does too much capital tied up in residential property constrain household consumption expenditure, reduce savings, crowd out job-creating investment, and ultimately slow economic growth? These risks will only get worse when rates eventually return to normal levels. If so, shouldn’t economic policy considerations go a bit further than affordability for first home buyers and a bit of glib talk about an overheated market in Sydney and Melbourne?

Yes economic policy considerations should certainly go further. I’ll cover the macro implications in a future post. Thanks for the comment.

Gene, a question for you, more so than a comment, that links the housing bubble with the pension changes…

There has been a strong economic case made (thought it is politically difficult to sell) for placing a cap on the value of the principal residence used in the aged pension assets test. The national average price, or some margin above that, has been proposed.

Would imposing that cap also reduce housing price pressures in the major urban centres, ie: Sydney and Melbourne – by providing an incentive for retirees to sell their high value residences and move to lower cost accommodation to fund their retirement?

If the housing stock in these areas is freed up in such a way, it could allow developers to increase the density of these residential areas and help younger people to purchase residences or rent at lower cost.

It might even be a boost for the regions, which have been relative losers in the current environment. New affordable retirement housing in regions would allow retirees to free up cash to provide for retirement – and provide a jobs boost where it is needed.

It seems to me that the current model gives an incentive to over-invest in the principal residence and reduce other savings. Even in the new 2017 pension assets test, harbour-side multi-millionaires can obtain a part pension, if they reduce their non-house assets to $800,000 per couple.

Just a thought – but one with a high degree of political risk, I suspect!

Yes the current system definitely gives you an incentive to over invest in the family home. Indeed I recall Ross Greenwood saying on the today show after the most recent pension asset test changed you should put all your money into the best family home you can afford! Thanks for the comment and the policy suggestion which makes sense to me.