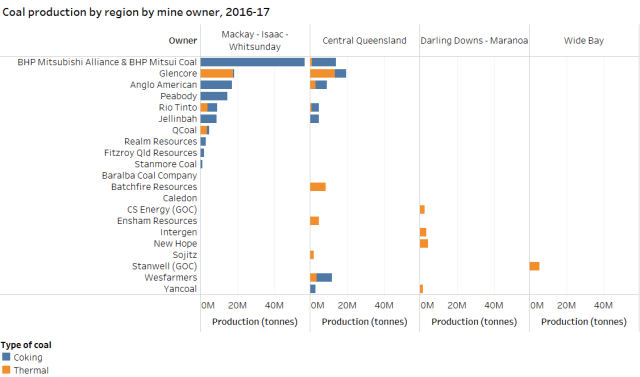

The recent Financial Times report Development bank halts coal financing to combat climate change, reprinted in this morning’s AFR, should prompt some serious long-term thinking from the Queensland government and local governments with regional economies heavily dependent on coal mining, particularly Mackay’s (also see this Reuters report which isn’t pay-walled). While two-thirds of coal production in Queensland is of coking coal (see chart below), there is no doubt there would be a large adverse shock to regional economies if there was a big shift worldwide away from thermal coal for energy generation.*

The FT report reminded me of the potentially major implications the worldwide shift against coal and related developments in solar PV and battery technologies could have for the Queensland state budget. Indeed, this issue is discussed in my new book Beautiful One Day, Broke the Next: Qld’s Public Finances since Sir Joh and Sir Leo. Comments regarding the government-owned corporations (GOCs) in energy generation and distribution from former Under Treasurer Mark Gray, reported on p. 167 of the book, are revealing as to why the Treasury was very supportive of the Newman government’s Strong Choices privatisation program:

According to former Under Treasurer Mark Gray, senior Treasury officials considered that the future income streams from GOCs were seriously at risk from technological change and possible policy responses to climate change. The energy assets were seen as particularly vulnerable, due largely to developments in solar and battery technologies which could reduce the reliance of households on electricity generated by the state-owned CS Energy and Stanwell and distributed by Energex and Ergon Energy, now Energy Queensland.

Furthermore, according to Mark Gray, in late 2014, at presentations on the Strong Choices privatisation program to potential investors, such as superannuation and sovereign wealth funds, Queensland Treasury officials were already being asked about the impact of technological change on the future profitability of GOCs and the risk of assets being stranded.

For more revelations and insights into Queensland’s recent state financial history, please consider reading my new book. The official book launch is next Wednesday evening at the Connor Court Book Room on Boundary St, West End, Brisbane:

Connor Court Christmas Party and launch of Gene Tunny’s Beautiful One Day, Broke the Next

* I prepared this chart for a Lytton Advisory report on Extended Payment Terms for the Resource Industry Network that I co-authored wrote Craig Lawrence.

Several elections ago I queried a local Greens candidate on why they were opposed to the sale of assets they didn’t want anyway. The response was somewhat delayed and confused.

Strong Choices was a political mistake because it lumped everything together on a choice between public and private. Even John Quiggin has stated this needs to be considered on a case by case basis.

My recollection is that very early Campbell Newman was concerned about the transmission assets as a natural monopoly. Problem is that the transmission assets are where the money was. Problem also that these may no longer be the natural monopoly they were once thought even a scant few elections ago.

Excellent points. Thanks Mark

Gene, on a world basis I expect there will be thermal coal demand for some time to come say 30 years. As QLD coal is a premium higher energy, lower ash and sulphur product it may be the last to be removed from the market. As banks, stop project financing mining companies may need to look more at equity financing. For those who take on some risk the rewards could be very good. As coal is on the nose generally but not the coal market the returns to company cash flow is high but company valuations are low. I have a small investment in a South African thermal coal producer listed on the ASX. The returns are excellent. I suspect we will see more of this.

Good points and info Russell. Thanks for the comment.