In today’s Financial Review, economics correspondent Jacob Greber observed:

The RBA has gone more than seven years now without raising interest rates, the longest span since the official cash rate was introduced in the early 1990s.

Indeed, on Melbourne Cup day in 2010, the RBA Board surprised the market and decided to lift the bank’s cash rate target to 4.75 percent, but since then it has had to progressively cut the cash rate target, which is now at 1.5 percent. You can see how the cash rate target has changed over time at the RBA website.

According to one prominent Brisbane-based market economist, we may not see the wage and CPI inflation that would prompt the RBA to raise rates until at least the second half of 2019, when he projects the Australian unemployment rate will finally fall below its long-run natural rate of around 5 percent. Morgans Chief Economist Michael Knox has written an excellent note on Why the RBA won’t hike rates any time soon. He notes:

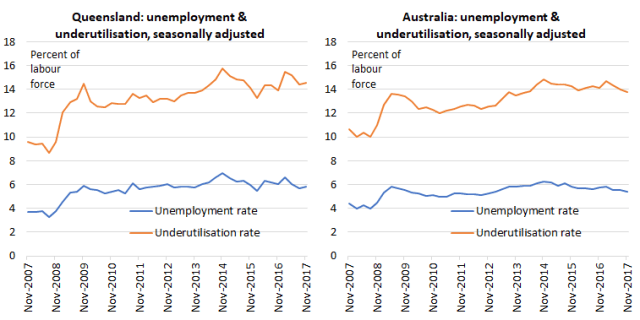

Why is it that the decline in Australian unemployment is so slow? One reason might be the high level of under-employment. The ABS tells us that when we include the number of people in part-time employment who want full-time jobs, then their estimate of underemployment in November 2017 rises to 8.3%. As employment grows, there is an additional source of supply of labour from this pool of under-employment. This acts to slow the decline in unemployment. It also acts to slow the increase in full time wages.

The national (seasonally adjusted) underemployment rate of 8.3 percent identified by Michael Knox adds to the unemployment rate of 5.4 percent to give a total labour underutilisation rate reported by the ABS of 13.7 percent. This underutilisation rate is significantly higher in Queensland at 14.5 percent (see charts below). Underutilisation of the labour force has been a persistent concern in Australia since the financial crisis, and it may indeed take some time yet for the economy to return to more normal rates of labour utilisation.