The Australian Government is right to be looking at reforming the rules around negative gearing, as the current rules appear to be distorting the market and encouraging excessive borrowing for investment properties (as well as denying the Government significant amounts of tax revenue). Negative gearing as a principle is fine, and is essential for the consistent treatment of debt and equity finance, but the highly concessional treatment of capital gains means that negative gearing strategies are very attractive to property investors. In its Re:think tax discussion paper from last year, the Treasury gives an excellent summary of the issues (Box 4.2):

“A property is said to be negatively geared when the mortgage interest repayments exceed the net income from the property (rental income minus other deductible expenses such as property agent fees, insurance, gardening, land tax and depreciation). In these circumstances the taxpayer can apply this ‘loss’ against their other income, such as salary and wages. This strategy is only financially effective where the taxpayer expects a future capital gain more than offsetting this ‘loss’. Generally only 50 per cent of that capital gain is subject to tax upon realisation, which the Financial System Inquiry’s final report noted could encourage ‘leveraged and speculative investment’ in housing.

So, ideally, the capital gains tax discount of 50%—which is arguably too concessional in Australia’s low inflationary economy—should be lowered, as it is distorting the market. There is certainly a distortion to correct, a distortion which is demonstrated by two odd facts.

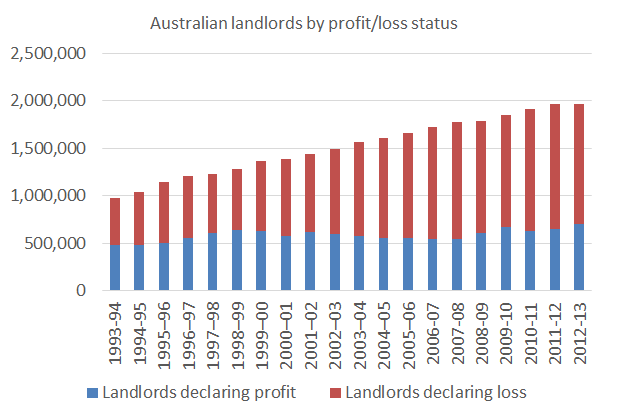

First, the majority of investors in rental properties are declaring net losses on their properties to the ATO (see chart below based on ATO tax data).

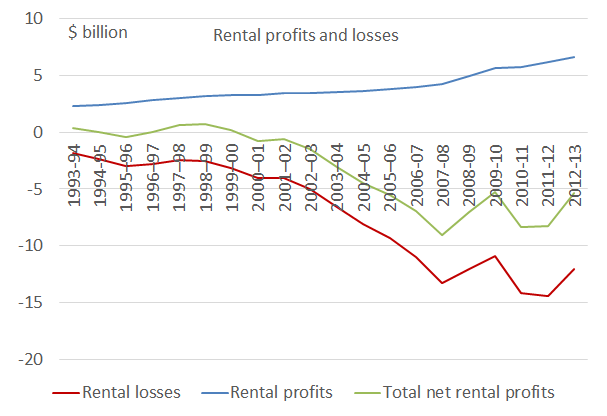

Second, as noted in Treasury’s tax discussion paper (p.64), “deductions claimed for investment properties as a proportion of gross rental income have increased over the last 15 years and are now greater than gross rental income.” So Australian households, in aggregate, are declaring a net loss on their rental properties, excluding capital gains (see chart below). That is, they are relying solely on capital gains to make money on their investment properties. This seems like a very odd situation, driven by the highly concessional tax treatment of capital gains that was introduced in 1999, and arguably should be addressed by the Government in its upcoming tax reforms.

Gene

Great post. I’m wondering if there is actually any rational reason for the capital gain tax discount at all? Is the treatment of capital gains on property investments any different from a capital gains on shares? I would have thought consistency in capital treatment across investment classes would be more efficient.

Good post Gene, for too long I have been frustrated by CGT being left out of the tax debate. A gain is income, why in Australia we always want to define different sorts of incomes and attach special tax arrangements is baffling.

Thanks for the comment, Glen. There is an argument for some discount because part of the capital gain is simply due to inflation. But in a low-inflation economy the current discount appears excessive.

The initial capital gains ta regime introduced in 1985 did index gains to the CPI. I don’t see anything wrong with a return to that methodology. Note also that under the discount method CGT can be payable in some circumstances even when there is no real gain after inflation.

Yes, returning to that methodology would make sense. Thanks for the comment Mark.

Hi Gene I agree this issue should be included in the tax debate mix.

There are couple of things that will affect your analysis, including: the majority of people negative gear to attempt to grow an investment to the point of being positively geared, the expansion in net losses could be due to a low growth in property prices as the road to positive gearing could take 10 – 15 years and the net gain for an individual will have to look at the persons overall income as the personal tax write down could be enough to make the negative gearing positive.

As you would probably agree, there are many parts of tax and income that interact which need to be considered in the discussion.

Not sure why everyone is down on negative gearing related to housing and not other investments like shares.

Thanks for the comment BJR. Certainly the prospect of eventually getting a positively geared property motivates many people but it’s the chasing of capital gains that appears to explain the huge growth of negative gearing in property over the last decade and a half. I don’t have a problem with negative gearing in principle, but the discount given to capital gains for taxation purposes appears too generous and that is encouraging a lot more negative gearing than is probably optimal.

>

I am firmly of the belief that CGT discounting should be applied with longer qualification periods. The current 1 year qualification period for 50% CGT relief simply encourages speculation and quick turnover in markets that are subject to high demand. If there is nil CGT relief for property assets held less than 5 years then short-term investors would be forced to pay a fair tax on profits and long term investors would not be disadvantaged. There should be no CGT relief for sales of unimproved land.

I’d like to see a continuation of the $ value graph through to the current low interest period because much of the residential stock held by the same investors for more than 4 years will now be much closer to neutral gearing.

Hi Gene, A couple of points (1) if CGT discount was removed, partially or totally, the government would not get back all of the ‘lost’ tax revenue. The number of owner-investors would decline to those comfortable with the lower likelihood of profit at the new level of discount. (2) And that would also push up rental rates. I lived in the US for a decade (where negative gearing against personal salary and wages isn’t allowed, ad you would know) and it’s incredible the difference in rental property availability, especially at lower socioeconomic levels. The result is mass government provision of such housing – creating ghettos, rather than our dispersal of such housing thru neighbourhoods providing children with varying role models in their streets and local schools (with only some government provision). I think there’s economic benefits with our negative gearing approach that aren’t being valued.

Thanks Gene, a very interesting article. I tend to think the problem is with the capital gains concessions, rather than negative gearing. While negative gearing is obviously largely driven by the expectation of capital gains, the size of the losses may also reflect declines in rental yields resulting from changing property market conditions. For instance, a lot of relatively unsophisticated investors who bought investment properties in mining towns at the height of the boom have experienced reductions in rents of around 30-40% in the last three years with high turnover and vacancy rates. While obviously investors need to take responsibility for their own investment decisions, it would seem a bit unfair not to allow those who are making significant losses on their investment properties with no prospect of capital gains to at least be able to offset their losses against their other income.

Tax Reform – Keep it Simple Stupid.

The Australian Tax System needs a complete overhaul – the system of collection of taxes is simply riddled with concessions, distortions, loop-holes that have encourage rorting and tax avoidance on a massive scale.

There is no point in collecting tax, if you just give it back in concessions and handouts. Australians are so addidicted to tax rorts and tax avoidance they will pay more to accountants in fees and banks in interest to avoid the equivalent amount of tax.

Here is the ‘KISS’ Keep it Simple Tax reform

The Australian Government needs to earn $430 B per year to cover it spending, that is $20,000 person.

There is no point in collecting tax if they just going to hand it back to the people they collected it from.

Superannuation – Scrap all tax concessions on superannuation contributions savings. Superannuation Savings is compulsory – you don’t need concessions to encourage it. The rich will always save for their retirement without concessions, the poor aren’t getting any concessions anyway. Scrap them all.

Negative Gearing – Scrap Negative gearing. It only encourages irresponsible investing, and over investment in property, as the taxpayer will pick up your losses. Your investments make a loss – bad luck – you pay for the losses. You’ll quickly sort it out.

Work Deductions – rorting so pervasive it has slipped beyond the control of the ATO. Scrap them too.

Capital Gains – Scrap the 50% discount. Earnings are earnings, tax should be paid at the owners tax rate, with the earnings spread over the period the assets was owned.

Grandfathering – Scrap the biggest tax rort – Grandfathering. This just encourages people to look for rorts, and get in early, knowing they will be protected by Grandfathering provisions. Change the tax laws. change it for everybody – perhaps allow 2 year transition for people to re-assess their investments.

Tax Rates – Scrap the differential in tax rates between trusts, companies and individuals. These only encourage rorting and tax avoidance. Tax rate should be set annually by the reserve bank to raise the required budget expenditure – say 30 % – and this moves up and down depending on government policy. Rate gets to high, vote out the government.

Scrap the complexity, reduce the rorting and the tax avoidance. Let people make better decisions without distortions from the tax collection system.

Yes I agree there are a lot of torts and we need fundamental tax reform. Thanks for the comment, Katrina.