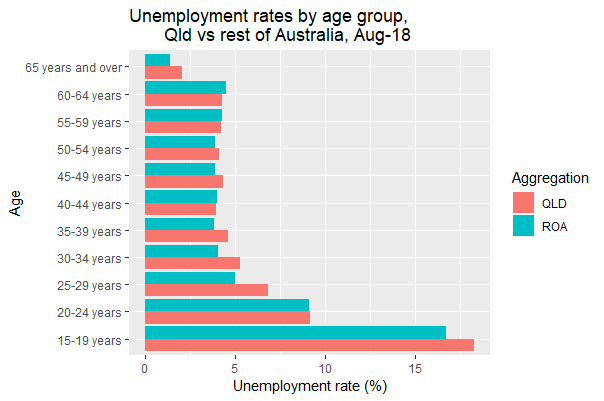

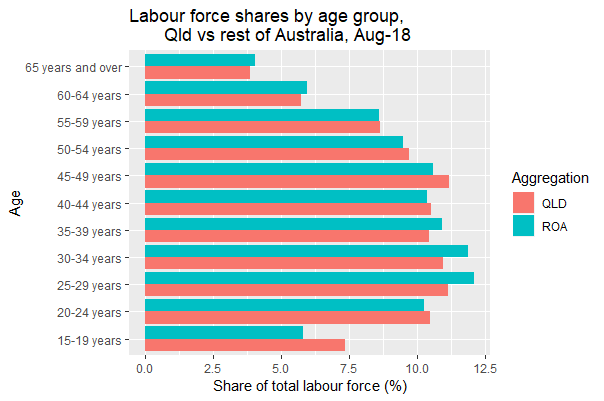

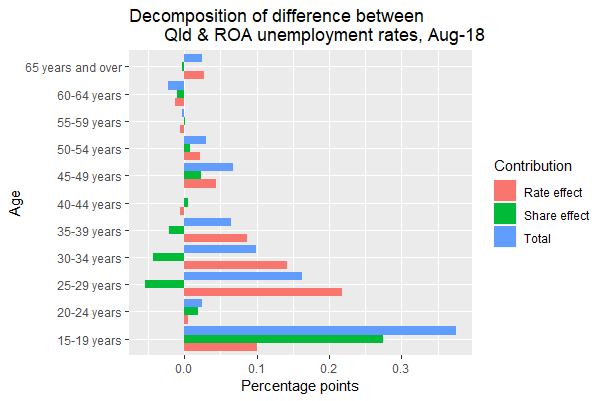

Regular reader Mike Willis made an excellent comment regarding my previous post breaking down the difference between Queensland’s unemployment rate and the rate for the rest of Australia, with Mike observing:

Am I correct in guessing that the relative deficit of 25-40 yo [year old] workers (the negative green “share effects” in these ages in your third graph) is related to the “brain drain” effect? IE: that tertiary qualified workers have to move interstate to find attractive work that suits their qualifications?

If my guess is correct, then that is the scariest observation in your data! The Queensland economy needs to find attractive value-adding enterprises to attract and retain that bright generation.

There is much truth in Mike’s observation. As I noted in the post, the jobs market for professionals has been relatively weak in Queensland in recent years. Indeed, Queensland Treasury’s occupational employment briefing for September quarter reported a 0.4% decline in employed persons classified as professionals compared with 3.4% growth nationwide through-the-year.

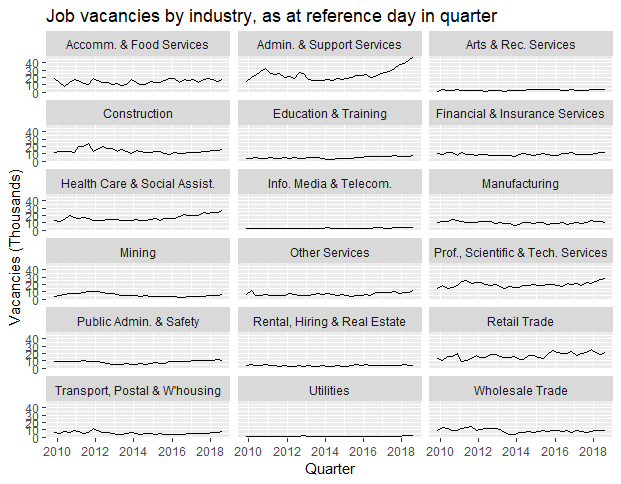

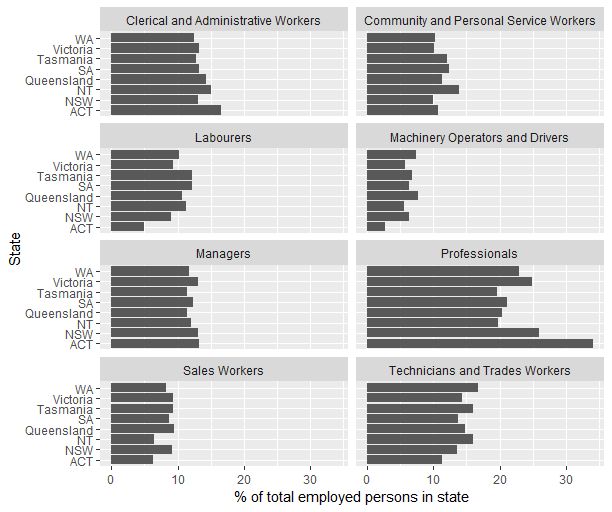

ABS Labour Force Survey data reveal Queensland has a much lower share of its workforce in professional jobs than other states. Professionals account for just over 20% of all employed persons in Queensland, compared with 26% in NSW and 25% in Victoria. That is, one-in-four employed persons in southern states is a professional, compared with only one-in-five in Queensland. See the facet plot below of the occupational shares of total employment by state/territory for September quarter 2018. The data are based on four-quarter moving averages of the original ABS data.

The facet plot also shows Queensland leads the states (i.e. not including the territories) in clerical and administrative workers, which is no doubt related to our bloated state public service.

Finally, I should note I agree with Mike that Queensland’s economy “needs to find attractive value-adding enterprises”. The best way to do this would be to set taxes and regulations on all businesses as light as possible, rather than by continuing the futile approach of providing special payroll tax holidays and other incentives to the favoured few fashionable businesses and international film productions. Special deals for the favoured few mean other businesses and households have to pay higher taxes than otherwise. For my previous comments on the futility, inefficiency, and unfairness of this type of industry assistance see:

Is Scottish Superstar BrewDog’s Arrival Good for Brisbane’s Brewing Scene?