Queensland has had more than its fair share of white elephant projects, including the Toowooomba Wellcamp quarantine facility and the Gold Coast desalination plant. The economics and politics of white elephants are considered in a new book from Connor Court Publishing, White Elephant Stampede: Case Studies in Policy and Project Management Failures. One of the book’s editors, well-known local public policy commenator Scott Prasser, is the latest guest on my Economics Explored podcast. You can listen to my conversation with Scott about white elephant projects on podcasting apps including Apple Podcasts and Google Podcasts.

White elephant projects are part of the broader problem of governments managing public funds poorly in many circumstances. A recent example of that is the revelation of $2.8 billion of previously “unforseen expenditure” across Queensland Government departments in 2021-22, as reported by the Courier-Mail earlier this week. Of course, we’ve just lived through a challenging period and some unforseen spending was probably unavoidable. But it does raise the question of whether the state Treasurer and his department are paying close enough attention to the operations of state government agencies. I’ll aim to have a closer look at the budget blowout in a future post.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

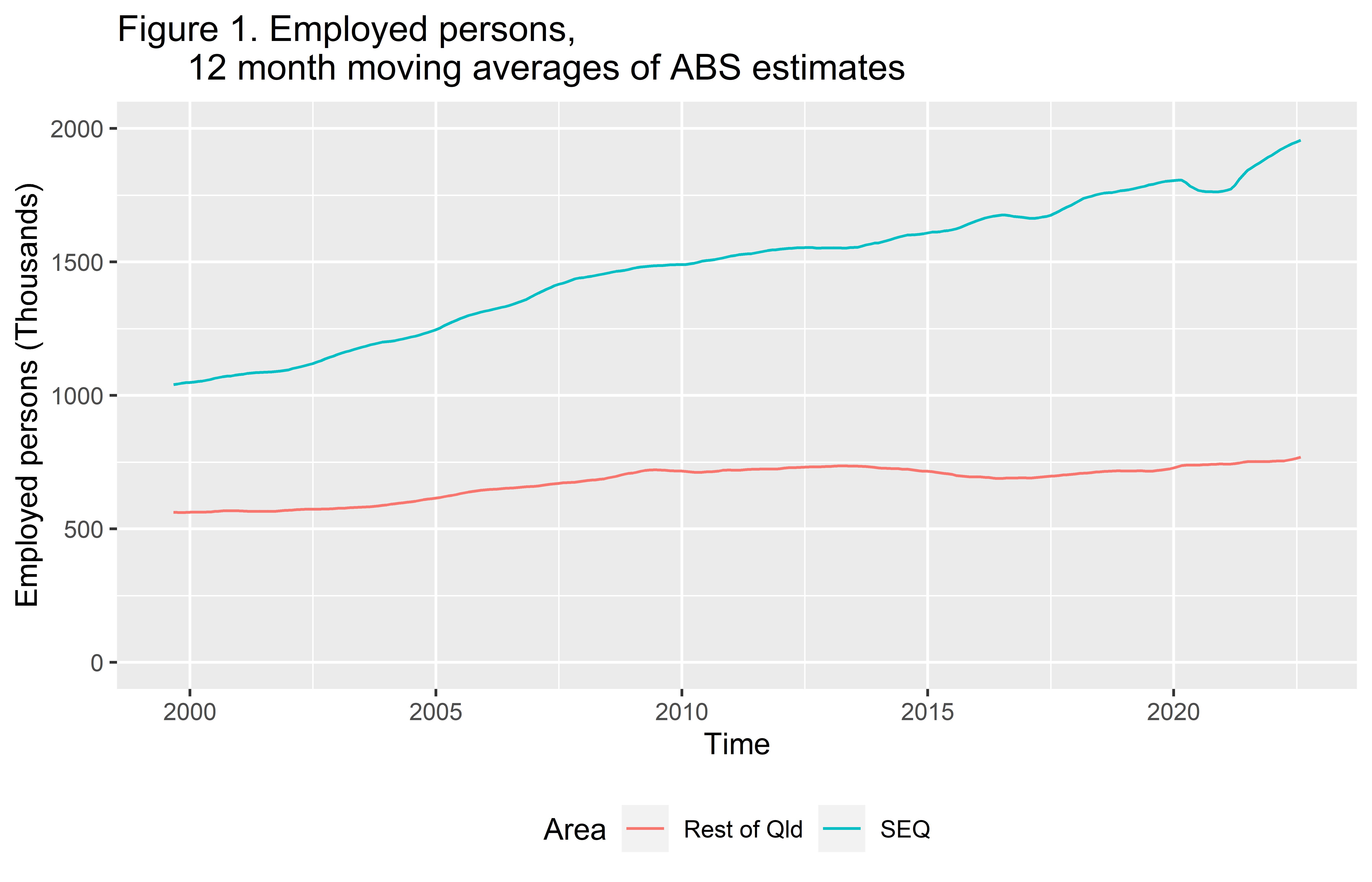

I’ve reported on how the economic recovery has seen large falls in unemployment rates across Queensland, including in most regions (see Remarkable turnarounds for Townsville, Mackay, and Cairns). But I need to acknowledge that employment growth is still overwhelmingly in the South East* as it has been for several decades now (Figure 1). Jobs and people are becoming more concentrated in the South East, and the pandemic doesn’t appear to have stopped that trend. Robert Sobyra of Construction Skills Queensland CSQ) has done some great research on this phenomena (see Why Regions Are Falling Behind – And What To Do About It), and I spoke with him about his research, which covers the whole of Australia, on the latest episode of my Economics Explored podcast. You can listen on major podcasting apps including Apple Podcasts and Google Podcasts. A lightly edited AI-generated transcript of the conversation is available on the Economics Explored website.

Rob presents evidence that the long-run regional divergence is largely a reflection of our post-industrial economy, in which knowledge economy jobs tend to concentrate in big cities. Here’s how Rob explains the divergence:

My research suggests the single biggest cause of regional divergence is that our economy is creating a lot more high-skilled than middle-skill jobs these days, and the vast majority of them are located in big cities.

For example, mining giants like Rio Tinto and BHP are rolling out fleets of autonomous trucks that are run out of cutting-edge remote operations centres. Whereas old-fashioned truck drivers would be located in towns near mines, these new centres are invariably set-up in major cities.

What does this mean for the regions in the long-term, particularly if we shift away from coal and lose all those tens of thousands of jobs supported by coal mining in the regions? Are the regions doomed to fall ever further behind SEQ? Or will the huge level of capital investment in renewables and storage (e.g. pumped hydro) required to decarbonise the economy generate a lot of regional jobs? Check out the conversation for Rob’s thoughts on this issue, and let me know what you think.

Consider that CSIRO research for CSQ (see Queensland’s Renewable Future), which Rob alerted me to in our conversation, suggests Queensland needs a 50X increase in renewable energy assets by 2050. Whether this is feasible, both technically and economically, is an open question. Incidentally, I’ll aim to cover the state government’s energy plan in the future, as there is much skepticism regarding just how achievable it is (e.g. see Graham Young’s comments).

*i.e. Brisbane metro, hinterland, Gold Coast and Sunshine Coast but excluding Toowoomba.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

One of the biggest challenges facing advanced economies is maintaining reliable and reasonably priced electricity as we decarbonise to combat climate change. This year we’ve seen some ominous signs that this may not go well. The war in Ukraine has reminded us we’re still highly dependent on fossil fuels, and disruptions to supply are very costly. European electricity prices are now soaring as Russian gas supply is restricted and it’s looking like a bleak Winter for Europe, something I identified as a downside risk to the global economic outlook in a generally positive Queensland economic update I gave at the Brisbane Club last Tuesday. You can download my slides via the link below. The scary European electricity prices chart is on the last slide.

In Australia, our National Electricity Market (NEM) had a near death experience in June and was temporarily suspended by the Australian Energy Market Operator (AEMO), which had to assume command and control, central-planning style, to keep the lights on. In the latest episode of my Economics Explored podcast, I speak with local energy expert Andrew Murdoch of Arche Energy about what happened in June and whether it could happen again. Are renewables coming into the system too quickly? What’s happening with batteries? Will Australia be able to cope with the retirement of coal-fired power stations? And what about all the EVs that will need charging? These and other questions are tackled in a frank and fearless conversation.

You can listen to the episode on Apple Podcasts, Google Podcasts, or other podcasting apps. Additionally, on the web version of this post, you can listen via the embedded player below.

Andrew is generally optimistic about our ability to manage the transition to greater renewable energy, but he certainly does appear to appreciate the risks, as this observation of his (at around 47:10 of the episode) illustrates:

“Looking forward, we’ve got 8.3 gigawatts of coal plant scheduled to be taken out of the market between now and 2029. It’s 2022 now. So that’s a lot of firming capacity that needs to be developed in that timeframe. If I look at the various different committed projects that are in the system at present…that only adds to 1.32 gigawatts of dispatchable generation required to cover that 8.3 gigawatts of retiring capacity. So there is a bit of a deficit there in terms of project firming projects that are available.”

That looks like a big challenge to me. The reliability and cost of electricity will very likely remain one of the top economic and political issues for the rest of the decade.

Please have a listen to my conversation with Andrew and let me know what you think.

Callide power station, near Biloela, Queensland.

Note: I changed the podcast episode title and the title of this post after publishing both. On reflection, meltdown wasn’t a good way to describe what occured in June.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

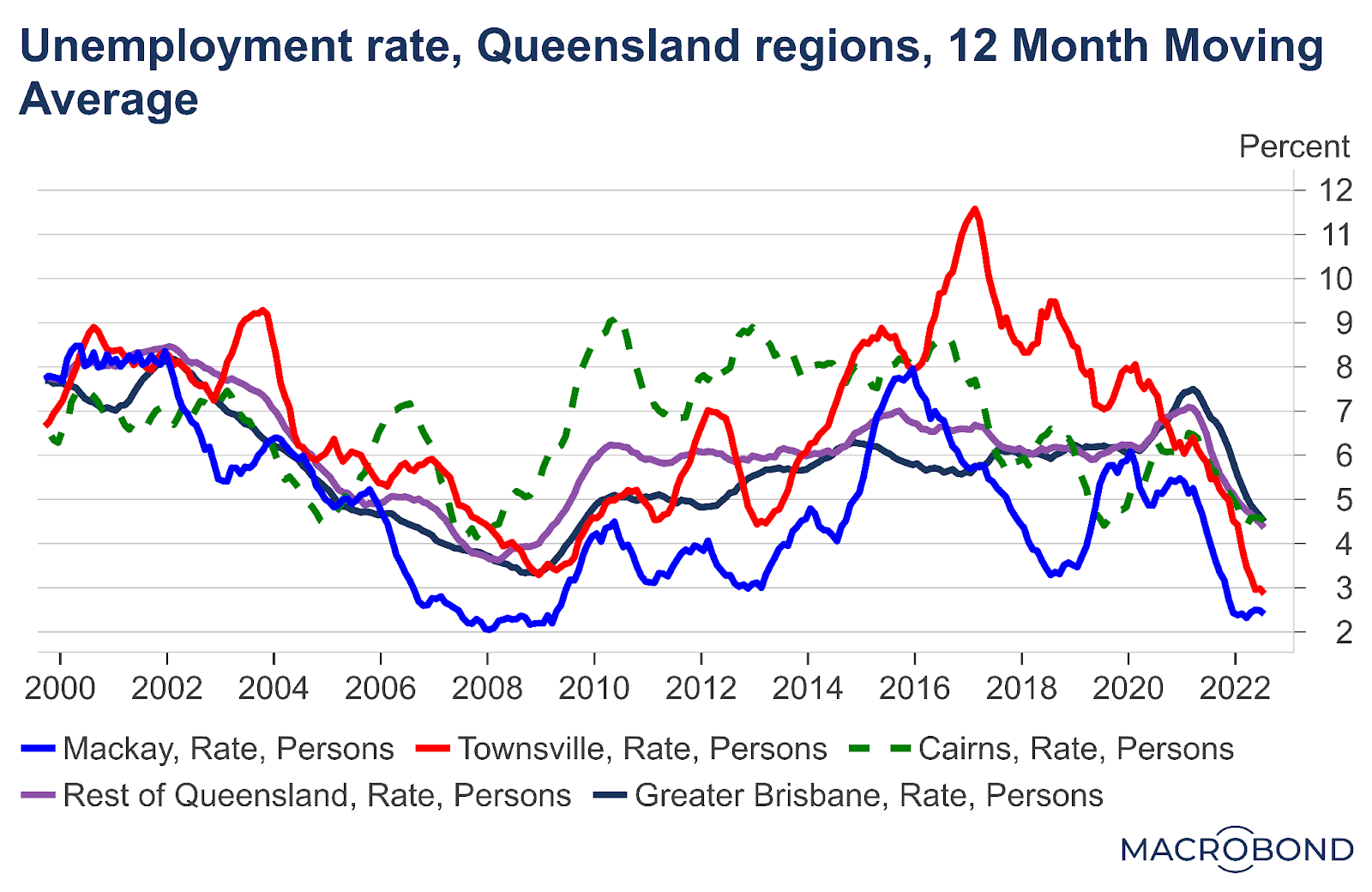

In my upcoming Brisbane Club presentation on Tuesday, one chart I’ll show is of selected Queensland regional unemployment rates, highlighting how the economic recovery generally and a booming mining sector have translated into some extraordinarily low unemployment rates in some regions. Regions such as Townsville, Cairns, and Mackay are experiencing rates of unemployment far below highs experienced last decade (see the chart below). The improvement in my hometown of Townsville is particularly remarkable.* The ABS’s estimate of the 12-month moving average unemployment rate for Townsville in July was 2.9%. Compare that with unemployment rates of 11-12% five years ago.

In a small number of regions, unemployment rates remain high, most notably Logan-Beaudesert and Queensland Outback, and Wide Bay (see chart below). I suspect this is partly related to the disproportionate numbers of disadvantaged people living in these regions, including Indigenous and low-skilled, long-term unemployed people. Structural change, including a declining manufacturing sector and mechanisation in agriculture reducing the need for on-farm labour, are also probably relevant. You can find the data behind this chart in the Queensland Government Statistician’s Office’s handy Regional Labour Force briefing.

One thing to keep in mind is that, while the numbers make sense in terms of what we know has been happening in state and regional economies, there is a large degree of uncertainty regarding the figures or point estimates to use the jargon. The estimates are derived from the Labour Force Survey and the ABS would only be surveying, at most, a few hundred households in many of the regions for which data are presented. I’ll aim to examine the size of the sampling errors in a future post.

Finally, if you’d like to attend the Brisbane Club Economics in Conversation event on Tuesday 6 September from 5pm I’m speaking at, alongside former state government finance minister Rachel Nolan and current shadow Treasurer David Janetzki, then please let me know and I can arrange it with the Club. Tickets are $65, but there will be plenty of drinks and finger food, as well as some great speakers, of course.

*Hat tip to JCU Adjunct Professor Colin Dwyer for alerting me to what the most recent labour force data have been showing for Townsville.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

This century’s great trends in the Australian economy are evident in the National Accounts data (Chart 1):

a halving of the relative economic contribution of domestic manufacturing, partly due to the car industry shutdown;

the periodic resources booms which have propelled the mining sector to a higher average share, but one which is volatile and dependent on commodity prices; and

the continued growth of the post-industrial economy and services sectors, with ever-growing health care and social assistance (e.g. NDIS) and professional services industries.

On his Substack Australian Economy Tracker, fellow Queensland economist Brendan Markey-Towler has commented regarding the Australian economy over the last decade as follows:

“To put it somewhat tritely: Australia is less and less a country that derives its wealth from making and building things, still a country that makes its wealth by digging stuff out of the ground and renting houses, and more and more a country that consults and cares.”

I spoke with Brendan about his Substack article earlier this week and our conversation is now available as my latest Economics Explored podcast episode “GDP & the National Accounts: What they are and why they matter”, available on all good podcasting apps, including Google Podcasts and Apple Podcasts. Please give it a listen and let me know what you think about the conversation.

Among other things, we talked about the contribution to the development of GDP and the National Accounts made by Colin Clark, whose UK National Accounts estimates were used by John Maynard Keynes in his General Theory. Clark spent the 1980s as a research fellow at UQ and earlier was a Queensland public service mandarin in the 1940s.

I was very impressed by Brendan’s enthusiasm for the National Accounts. He reminded me just what an outstanding intellectual achievement they are and how important they are to understanding our short-run economic performance and longer-term trends.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

The RBA is in the spotlight at the moment as there’s a risk its monetary tightening will crash the housing market and broader economy. Arguably, it should have acted earlier to raise rates and to stop its quantitative easing. Even though inflationary pressures were obvious from late 2021, the Bank still insisted the cash rate could remain at 0.1% until 2024 and it continued its QE (i.e. buying government bonds with money created from thin air) until February this year (see the RBA’s Christopher Kent’s speech From QE to QT – The next phase in the Reserve Bank’s Bond Purchase Program | Speeches | RBA). Having let inflation accelerate more than it should have, the RBA now has to tighten much more than it would have otherwise.

So it makes sense the Albanese government is reviewing the RBA. Peter Tulip, Chief Economist of the Centre for Independent Studies and a former RBA and US Federal Reserve economist, has been one of the loudest and most informed voices calling for changes to the RBA. I had a great discussion with Peter on episode 149 of my Economics Explored Podcast a few weeks ago. You can listen to the episode via the embedded player below or via podcasting apps including Google Podcasts and Apple Podcasts.

I’ve cut some clips of the video of my chat with Peter and uploaded them to YouTube. First, here’s Peter explaining why the RBA review is necessary – i.e. among other reasons, other central banks are regularly subject to review and Peter thinks the RBA has made some big monetary policy mistakes in recent years, keeping interest rates too high before the pandemic and costing the economy hundreds of thousands of jobs.

In the second clip, Peter talks about his main recommendations for the RBA which he hopes the review will pick up.

In Peter’s words:

“Number one, we want more monetary policy experts on the board.

Number two, we want those members to be individually accountable. That means public votes and public explanations of decisions.

And third, the bank needs to be more open and transparent. And, in particular, it needs to give clear reasons for its decisions, and why alternatives are not taken.”

Peter also would like an explicit full employment target and clear direction from the government regarding whether the central bank should target financial stability (e.g. where it could have higher interest rates to prevent households accumulating too much debt). Peter thinks the RBA has gone wrong when it was too worried about financial instability, and it should leave that job to APRA. I’m unsure I agree with Peter on this, but I do agree the government should be explicit regarding what it wants the RBA to target.

Incidentally, the RBA review was the subject of an excellent panel session at the Conference of Economists in Hobart last month, one of the best conferences I’ve ever been to, despite it having been a super-spreader event at which I picked up COVID. Panel member ANU Professor Warwick McKibbin, a former RBA board member and one of the world’s leading macroeconomic modellers, suggested that the monetary policy rules for the RBA will need to accommodate (i.e. look through) any increases in prices coming from greenhouse gas mitigation policies. The prices of many products will need to rise to bring about greenhouse gas mitigation targets. It would not be appropriate for monetary policy to target these price increases, and it would be counterproductive, as it could deter necessary investment in low-emissions technologies in Warwick’s view. This is certainly an issue for the RBA review to consider.

Of course, we still don’t know exactly what explicit or implicit carbon taxes Australian industry will be facing over coming decades yet. The Parliament has passed a 43% emissions reduction target by 2030. But we don’t know the details of how this will be enacted and to what extent it will be enforced through the so-called Safeguard Mechanism, under which big polluters would need to buy Australian Carbon Credit Units to meet their obligations. This is a way of imposing a carbon price or carbon tax without explicitly imposing one. I pity Chris Bowen, the Minister for Climate Change and Energy, who has to implement the government’s overly ambitious policy, which appears politically suicidal in the long-run to me. It’s not enough to satisfy the Greens but could impose large enough costs that it loses votes in the centre. Bowen was on Katharine Murphy’s Guardian Australian Politics podcast recently and noted he’d be releasing a discussion paper on how they’ll implement the target very soon. Expect the climate war to start up again after that paper is released and the costs to industry and households of greenhouse gas mitigation become clearer.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

Hidden in a note to its economic forecasts table in the state budget was the extraordinary estimate from Queensland Treasury that, in nominal dollar terms, the state economy expanded 22% last financial year, 2021-22 (see the chart below based on estimates prepared when updating my interstate debt comparisons slide deck). Queensland’s Gross State Product was nearly $450 billion in nominal dollar terms in 2021-22, an increase of around $80 billion, largely due to crazily high coal prices. In real or volume terms, adjusting for price increases including coal price increases which have blown out the value of exports in dollar terms, the economy only expanded 3% according to Queensland Treasury’s estimates.

A lot of the additional GSP will have gone to mining companies as profits, to be shared among both domestic and foreign shareholders. That said, in 2021-22, the state government received $9 billion in royalty revenue compared with the original forecast of $3 billion, and mining workers would have benefited, too, with reports of higher wages and sign-on bonuses (see the QEW article linked to previously).

The huge positive boost to Queensland’s economy that we saw in 2021-22 is consistent with Morgans Chief Economist Michael Knox’s view covered by John McCarthy in his recent InQld article Better than the gold rush: How Australia is booming while share prices plunge. Of course, we now need to see how the economy reacts to the RBA hiking interest rates, and we’re expecting a half-percentage-point (0.5%) increase in the overnight cash rate today. As I’ve covered in a previous post, consumer confidence has fallen in recent weeks, probably due to recent interest rate hikes (see Consumer confidence indicators are very concerning).

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

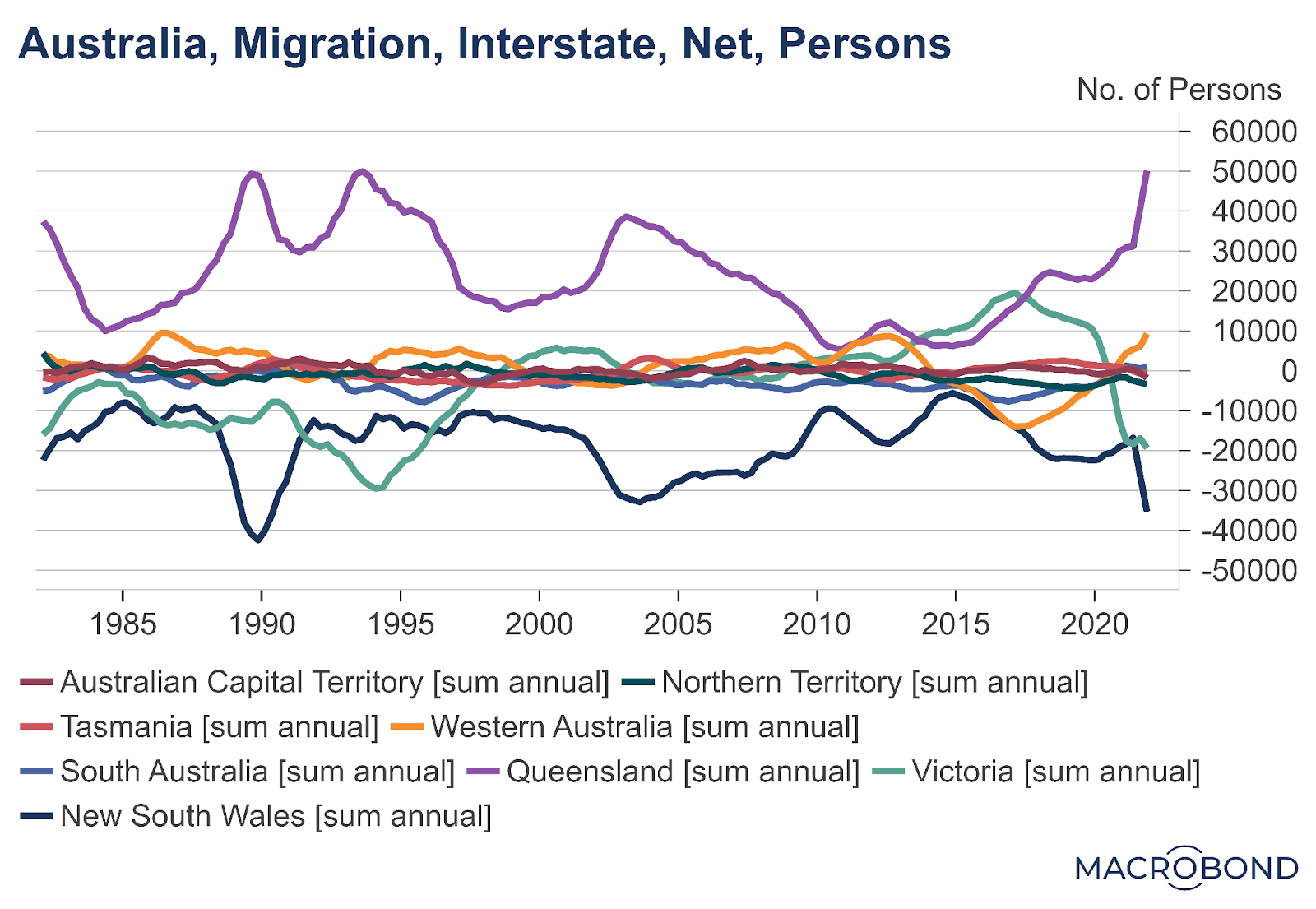

It’s been an extraordinary day of news for Queensland today, with:

a) record net interstate migration over a twelve-month period of just over 50k, and record quarterly net interstate migration of 19k in December quarter 2021, revealed in the ABS’s latest population report (see chart below*); and

b) the publication of Peter Coaldrake’s hard hitting integrity review, which has confirmed what many of us have suspected for a long time about the inner workings of the Queensland Government – i.e. the excessive influence of lobbyists, a public service manipulated for political purposes, etc. – and has made some excellent recommendations which, to her credit, the Premier has agreed to implement.

With all these new Queenslanders (i.e. approx. 1,000/week if we use the 12 month gain, or nearly 1,500/week if we use the December quarter gain), it’s good we’re finally going to improve government accountability and integrity. Better late than never, of course. One recommendation which blew me away – given I’ve worked as a public servant at both state and federal levels and understand just how radical a measure this is, although apparently it’s been adopted in NZ and is wildly successful – is the presumption that cabinet documents should be made public in a timely fashion. This is the specific recommendation:

Cabinet submissions (and their attachments), agendas, and decisions papers be proactively released and published online within 30 business days of such decisions.

Well done Peter Coaldrake. Now it’s time for the government to follow through.

*Note that although we’re breaking records in terms of the number of people, the proportionate contribution of net interstate migration to state population was higher during previous peaks in the 1990s when we nearly got to 50k/year and had a smaller population.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

If you know of any postgraduate students at a Queensland university who are interested in political science, then please pass on the details of the Australasian Study of Parliament Group – Queensland (ASPG-Q) essay prize:

Here’s a note I was sent the other day by the Secretary of the Australasian Study of Parliament Group James Gilchrist regarding the prize:

We’re seeking entries for our prize for parliamentary scholarship, where the winner gets a $1,000 prize…The prize recognises outstanding research or analysis into the institution of parliament. All postgraduate students enrolled at any Queensland-based university can submit an assignment of up to 10,000 words on this theme.

The assignment must have been written between April 2021 and the closing date of 3 October 2022. Course coordinators, lecturers and supervisors can also submit their students’ essays.

Potential essay topics which come to my mind include:

whether Parliament is avoiding its responsibility for providing good government for the people of Queensland by delegating substantial powers to unelected bureaucrats such as the Chief Health Officer (see Qld CHO emergency powers extension bill submission); and

Looking up toward the balcony outside the chambers of the Queensland Parliament, Queensland Parliament House, corner of Alice and George Streets, Brisbane. The Tower of Power, 1 William St, soars into the sky in the background.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

Reading the Courier-Mail’s latest state budget reporting, quoting Cameron Dick as a self-proclaimed Robin Hood Treasurer, it’s clear the state government no longer gives a damn what business thinks. It’s gone full-on economic populist with its royalties hike ($1.2bn over four years) and its payroll tax hike ($1.4bn over four years) masquerading as a Mental Health Levy, as if mental health problems are the fault of business alone. I would argue that, by providing jobs, business overall is making a great positive contribution to mental wellbeing. We know from decades of empirical research that unemployment is a major life stressor and contributor to mental illness.

In fairness, I should note the state government is providing some relief to businesses with payrolls of under $10 million, but overall it’s increasing the burden of payroll tax on Queensland business collectively. Over the forward estimates to 2025-26, the Mental Health Levy will bring in $1.4 billion while its payroll tax relief for smaller businesses is only worth $210 million (see page 25 of Budget Paper 4).

The state Treasurer argues that it’s only fair that big business ($10M+ in payroll by his definition) pays more, given it has done well in recent years, especially with the overly generous JobKeeper. Sure, vertical equity, that those with a greater ability to pay should pay more in tax, is a well-established principle of taxation. But governments need to be mindful they don’t unduly burden business with additional taxes that either: a) reduce their profitability and capacity to invest and expand, costing jobs b) they pass onto consumers by hiking prices, contributing to inflation, and reducing their interstate and international competitiveness, or c) they pay for partly by paying their workforce less than otherwise in the future.

Tax per capita remains lower in Queensland than in NSW and Victoria, but we lost the Low Tax State label, for the state with the lowest tax burden, over a decade ago, and SA, Tasmania, and NT now have lower tax burdens (see Chart 4.5 on p. 97 of Budget Paper 2).

Regarding royalties, one point I forgot to mention in yesterday’s post is that Queensland’s royalty regime was already delivering a greater share of the value of our minerals to taxpayers than those in other states, according to Michael West Media estimates produced last year:

“Western Australia, Australia’s largest commodity exporting state, captures just 5% of its commodity export value as royalties.

In comparison, over the past 10 years, Queensland’s royalty scheme has collected double that – 10% of the total commodity export value. In fact, in 2020, royalty payments reached a record 15% of export value.

Queensland is followed by the Northern Territory at 8%, New South Wales at 7% and South Australia at 6%.”

It wasn’t obvious we were missing out and needed higher royalty rates, but the Queensland Government needs to fund its various SEQ-centric vanity projects such as Cross River Rail and Olympics infrastructure, and the miners looked like an easy target. After all, many of them are foreign-owned and they’re contributing to climate change they were probably thinking in 1 William Street.

Finally, one of my long-time regular readers has asked me:

“My question on the energy generators… Qld Govt is going to reap huge dividends from them but nothing will be passed onto Qld tax payers… why is this so?”

This is well observed (see Chart 1). While the Government is providing a one-off $175 cost of living rebate, as announced last month, it can’t do much more because it needs to fund the aforementioned vanity projects as well as fix up the state hospital system, among other problems. I’d also note that current financial year (i.e. 2021-22) dividends are less than previously forecast last December as the Government is allowing government-owned corporations to retain some of their profits for reinvestment in new assets and refurbishment of existing assets (i.e. to ensure we have working generators and a reliable power grid), as the Government notes on page 160 of Budget Paper 2.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.