This guest post by my good friend and fellow Queensland economist Dr Brendan Markey-Towler makes some excellent points regarding Queensland’s economic recovery from the COVID-recession – e.g. consumption spending has been goosed up by government benefits and, apart from in housing, private sector capital investment levels aren’t encouraging. It goes without saying that views expressed are Brendan’s and should not necessarily be attributed to me. GT

Six houses, alike in dignity… not much else

by Dr Brendan Markey-Towler

A global pandemic has helped us rediscover the Australian constitution. We look at the economic impacts of a 21st-century Premier’s Plan.

- We look at key economic indicators across the Federation to evaluate the effects of Covid-19 and associated policy on economic recovery.

- Queensland has the strongest overall recovery, but probably thanks to the effect of government stimulus in a comparatively open economy.

- New South Wales probably displays the most robust recovery, with modest but consistent indicators and leading the nation in private business investment recovery.

Australia was envisioned as six states that delegate certain powers upward for defence, foreign relations and to regulate a trading bloc. The states were intended to be the primary policymakers. For instance, the “Premier’s Plan” to combat the Great Depression was led by the states, each implementing their own response within a coordinated national plan.

Mr Xi Jinping has helped us rediscover our constitution. The response to Covid-19 has been a 21st-century Premier’s Plan; the states each implementing their own policy within a coordinated national response. This provides us with a great case study of economic Federalism in 21st century Australia.

There is no such thing, really, as an “Australian economy”. Rather there are six roughly correlated city-state economies, each with a vast interior. The ABS collects data on each, and though the sampling error is higher than national data, we can still roughly evaluate each state’s success in facilitating post-crisis recovery by indexing indicators to the first quarter of 2020.

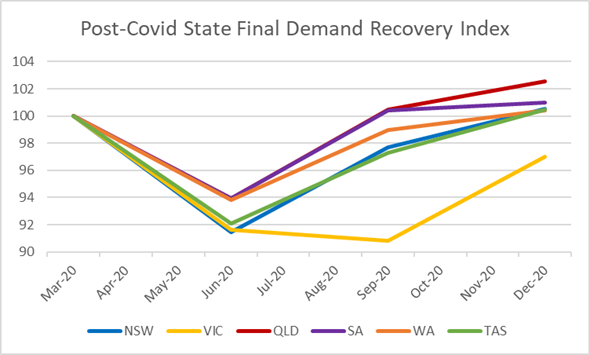

In terms of State Final Demand (a metric of overall aggregate expenditure), we clearly see that Victoria is paying the price for its extended lockdowns and restrictions. It is the only state not to have fully recovered. Queensland leads the Federation, just under 3% above pre-crisis state final demand.

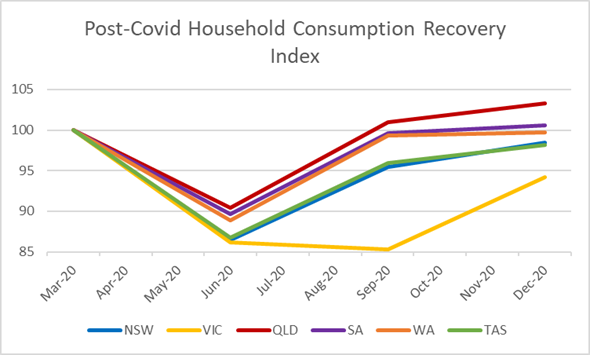

Breaking this down, household consumption provides the “bedrock” for State Final Demand across the Federation simply because it is so large. We clearly see that the five States which avoided extended lockdowns and restrictions have been able to take advantage of the massive JobKeeper and JobSeeker supplement programs and fully recover pre-crisis household consumption and then some.

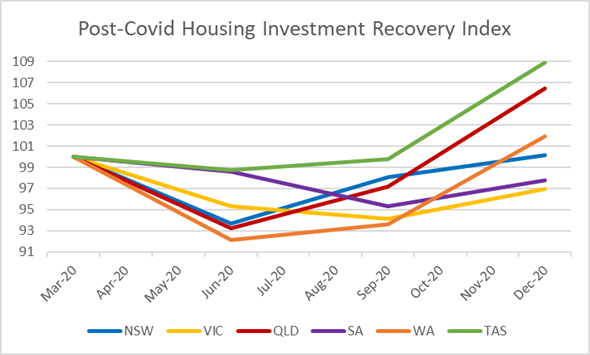

We see a similar, even stronger effect in the housing market of the mid-tier states (Queensland and Western Australia) and Tasmania. We believe the dizzying strength of their housing investment reflects significant state and Federal subsidies in comparatively unrestricted housing markets.

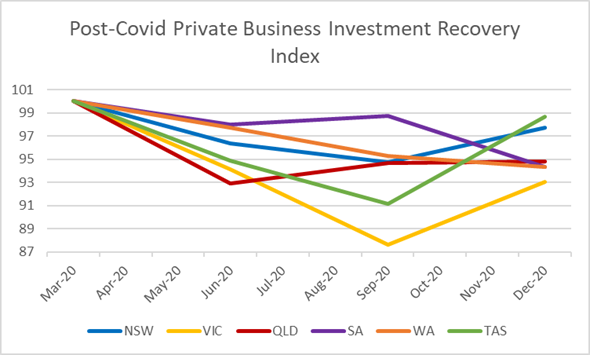

Turning our attention to private business investment, we begin to see a different story. This is important because private business investment is the key driver of prosperity, allocating resources to expand future economic capacity.

Here Queensland and Western Australia are over 5% below pre-crisis levels and show no signs of recovery. This is particularly concerning for Queensland, as it was displaying stagnant and declining private investment pre-crisis. We believe this is due to the uncertain business environment created by public health policies that focus exclusively on caseload mitigation using hard interstate border closures as a first resort and widescale lockdowns as a second.

New South Wales leads on this key indicator, with private business investment just over 2% below pre-crisis levels and recovering. This is likely due to public health policies that seek to balance virus mitigation and economic sustainability. New South Wales invested massively in world-class contact tracing and targeted quarantines to make good on a commitment to no further wide-scale lockdowns. The only other states where we see recovery are special cases: Tasmania attracts a tiny proportion of national business investment, and Victoria is recovering from a catastrophic decline.

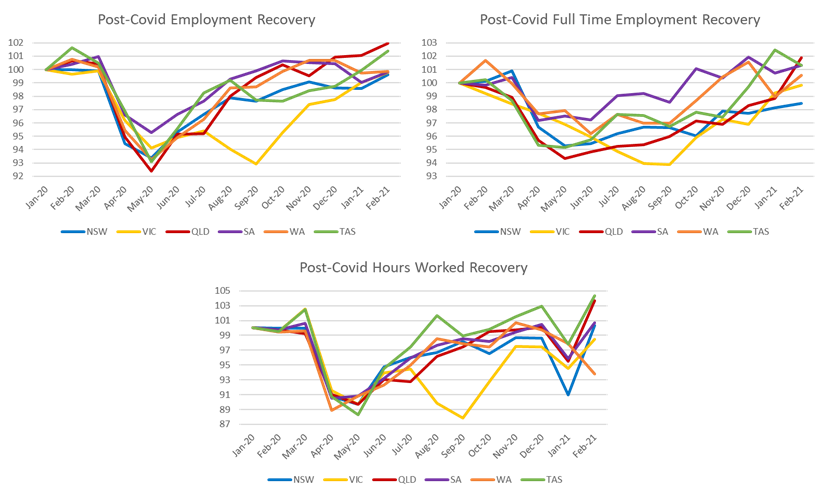

In the labour market, New South Wales is a little behind on employment and full employment levels. However, it comes in meaningfully behind only Queensland and Tasmania on hours worked and has displayed the more consistent recovery across all metrics.

Conclusions

Queensland displays the strongest recovery in household consumption, housing investment, and hence (albeit only recently) the labour market. But it displays little recovery in private business investment, suggesting its recovery can be attributed to the effect of massive government stimulus in a relatively unrestricted economy behind its big, beautiful border wall. It probably outperforms Western Australia due to the latter’s wall being so strong as to nearly constitute secession.

New South Wales on the other hand displays the more robust recovery with moderate but consistent recovery across all indicators and leading the national recovery of private business investment. New South Wales may be slightly behind overall, but slow and steady will probably win the race.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com

We are not Post-Covid yet ! Far from it.

Hi Katrina, I agree. Brendan appears to have been using post-COVID as a shorthand for post-COVID recession, which hopefully we are post. Of course, with the end of JobKeeper and the vaccine rollout delay, we can’t take that for granted. Thanks for the comment.