Whoever looks after the Queensland Premier’s Instagram account is a social media grandmaster (e.g. see the post below). The regular reminders of the imminent end of JobKeeper on 28 March are contributing to pressure on the federal government to implement a replacement scheme for tourism and hospitality, which it absolutely needs to do, unless it wants to send Cairns into an economic depression and risk the recovery of many other tourism-dependent regions in Australia. Of course, the Premier’s Instagram posts are also a political mind trick, distracting people from the fact the state government’s past interstate border closures have been a contributing factor to the financial strains felt by many tourism and hospitality businesses across Queensland.

The imminent end of JobKeeper is the big risk to Australia’s economic recovery, and we need to keep it in mind when interpreting the National Accounts released by the ABS yesterday. The December quarter National Accounts showed stronger than expected growth in the December quarter of 3.1%. That said, the Australian economy was still 1.1% below where it was in December quarter 2019, meaning things definitely aren’t back to normal yet. In per capita terms, GDP was 1.8% below its December quarter 2019 level.

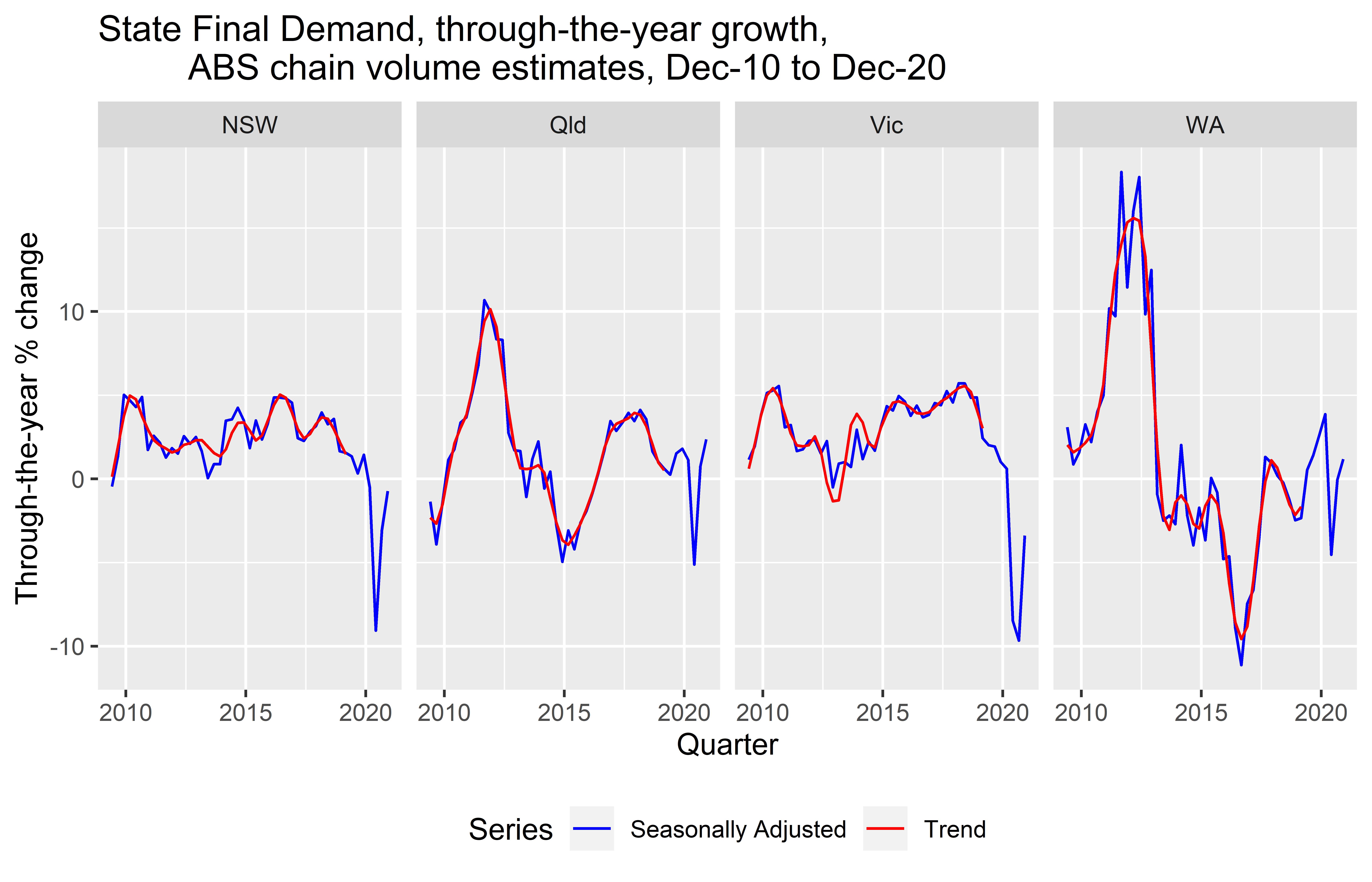

Queensland performed better than the rest of Australia over 2020 and ended the year with the highest through-the-year growth rate (2.4%) among the states (e.g. see chart below). I suspect our resilient mining and agricultural sectors helped Queensland cope with the COVID shock better than most, along with the state government continuing to grow the public service at a high rate.

In its State Details briefing, Queensland Treasury has a solid analysis of Queensland’s December quarter performance in terms of the expenditure components of State Final Demand (which doesn’t include exports or subtract imports from spending components in which it’s included). Treasury rightly highlights the importance of a surging building industry to Queensland’s recovery:

Dwelling investment rose 9.6% in the December quarter, driven by a 10.1% rebound in new and used dwellings. Although this component had been in a long-run decline since the end of the apartment construction boom, low interest rates and generous government incentives have spurred a recent surge in activity in this sector. Strong recent building approvals data suggest the increase in construction activity will continue in coming quarters.

Meanwhile alterations and additions rose a further 9.0% in the quarter. The pandemic has seen Queensland residents choose to increase investment in their current homes, with alterations and additions investment now up 21.9% since June quarter 2020.

Overall, yesterday’s National Accounts confirmed that Australia is recovering much better from the COVID recession than expected. But, of course, the National Accounts were for a quarter which finished two months ago, and they are old news now. Big risks remain, particularly from the imminent end of JobKeeper. On the so-called fiscal cliff, check out the excellent briefing from Dave Rumbens from Deloitte a few weeks ago.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com