Last Wednesday, RBA Deputy Governor Guy Debelle addressed the ESA (Qld) business lunch at the Brisbane Hilton on the topic of low inflation.* The Deputy Governor took the audience through the different components of the consumer price index (CPI) and showed the large contributions that increases in cigarette and energy prices have made to inflation in recent years, and also that these increases have been offset by declines in many retail prices due to greater competition and technological improvements, keeping inflation low overall.

While Debelle’s speech was highly informative, it was something he only briefly mentioned, and which was not actually in his official speech, that interested me the most: the debate about whether house prices should be included in the CPI. Debelle noted that housing costs are reflected in the CPI in two ways: new dwelling construction costs and rents. He said that house prices themselves are not included, but why that is so could form the topic of another speech. For economists already familiar with the CPI data, that may well have been a more interesting speech, as it would have prompted a discussion of the appropriateness of the RBA’s current methodology for setting monetary policy.

Recall that the RBA sets the overnight cash rate, which influences longer-term interest rates, with a view to targeting 2-3% CPI inflation over the business cycle. It is important, therefore, that measured CPI inflation provides as accurate a gauge of underlying inflation as possible, otherwise monetary policy could be too loose or too tight, destabilising the economy.

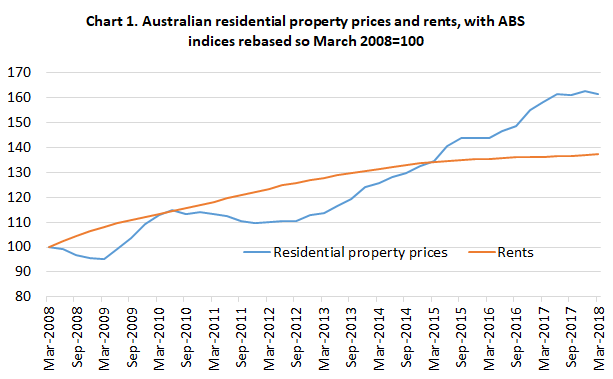

As house prices are not included in the CPI, the RBA may not adequately consider them in its formulation of monetary policy. The RBA could set monetary policy too loose, with a low cash rate, encouraging a housing boom with high house price inflation, even though rents may be increasing at a much lower rate. But, as it is rents that are included in the CPI not house prices, the RBA may miss the signal that its monetary policy is too loose. This is arguably what has happened in Australia since 2012-13 (see chart 1). In his latest column in the AFR Weekend, leading financial economist and investor Christopher Joye made the excellent observation:

…the RBA had recklessly underestimated the impact of its 2012 and 2013 rate cuts on house price growth and credit creation, which would precipitate a bubble and the need for unprecedented regulatory constraints on lending…

Those regulatory constraints by APRA have worked, and Sydney and Melbourne house prices are now falling, after having reached absurd levels. Hopefully the adjustment will be relatively smooth without an adverse impact on the broader economy. Of course, that is not guaranteed. Consider the related risk to the economy from the reset of a large number of interest-only loans for investment properties to traditional principal-and-interest loans over the coming years. This reset could lead to cash flow problems for many investors and forced sales of properties, putting further downward pressure on prices and possibly curtailing household consumption expenditure, with macroeconomic consequences (e.g. see this AFR article from April).

In my view, the RBA has patted itself on the back too much regarding the success of its inflation targeting regime, and it should consider alternative approaches, such as nominal GDP targeting or an approach which augments inflation targeting with a mandate to promote financial stability, as discussed by Warwick McKibbin and Augustus Panton in an RBA conference paper from April:

25 years of inflation targeting in Australia: Are there better alternatives for the next 25 years?

Finally, I should note it’s probably unnecessary to include house prices in the CPI, although the RBA should pay greater attention to house prices than it has historically. Statistical agencies such as the ABS arguably have valid grounds for excluding house prices from the CPI. For instance, houses are an investment, rather than a typical consumption good, and the CPI is intended to measure consumer prices. The larger issue is the appropriate monetary policy framework, particularly the extent to which central banks take into account credit conditions and asset prices in their monetary policy decisions. By focusing excessively on CPI inflation, which the CPI inflation target of 2-3% prompts the RBA to do, the RBA arguably failed to restrain the excessive growth in house prices we saw in recent years. Over the next few years, we will see whether that misjudgment will have adverse macroeconomic consequences.

* I am a Vice President of ESA (Qld), but this post contains my personal views, which should not necessarily be attributed to the society.

The APRA regulatory constraints have been underestimated by economic commentators (and I suspect regulators) who are not property investors. For many years property investors were assured by banks that their interest only loans will be rolled over into another interest only loan, and invested on that basis. The news that it would now become a principal and interest loan on a loan term significantly shortened by the interest only period is creating shock waves as investors have to sell properties. Luckily for them high migration has increased demand for owner-occupied properties, reducing the blow. But many property investors may not yet be aware of the shock coming as their interest only loans cease in the next couple of years.

(Personally I was lucky to sell an investment property at the Melbourne market peak to owner occupiers – recent migrants. I have friends and family selling investment properties to avoid the cash flow shock.)

Thanks for the comment David. Good timing re. your Melbourne investment property.

Thanks for the post Gene,

I wonder whether you need to ‘unpack’ what I think you’re getting at into what seems to be its two constituent parts. I think you’re saying that there are two things that monetary policy should target and they’re the inflation target (assuming some agreement on how to measure inflation) and financial stability.

That seems reasonable to me. If so, isn’t one first order issue coming to grips with what to do when they’re in tension? It seems to me they’ve been in tension with each other since the Asian reaction to the Asian crisis in the late 1990s – which was to massively increase savings rates and so export unemployment to the rest of the world.

That gave Greenspan and others a problem which was that, to hit their targets, they needed to bring interest rates down low which blew bubbles of various kinds. If you believe Minsky, perhaps monetary policy is always threatened with this dilemma – that economic stability breeds bubbles and so breeds instability.

In any event, the question becomes what do you do when you decide to defend long-term financial stability when it’s in some tension with your other concerns – inflation and (by implication) unemployment? As I see it, there are at least two issues that those calling for higher rates need to address.

The first is that old business about costs and benefits. If higher interest rates now will lower the risk of financial instability later, how much will they lower it, what are the benefits of so doing, and what are the costs? The one attempt to do this that I’m aware of was by Lars Svensson. In this paper, the former Riksbank Deputy Governor, compared the costs of higher rates– increasing unemployment by around 1.2 percentage points – with its benefits – the marginally smaller likelihood and severity of a possible future downturn. The result? The costs of higher rates outweighed the benefits 200 to one. The Riksbank subsequently reversed policy pioneering negative repo rate – relatively successfully.

Now you can disagree with that figuring, but it seems to me that you have to go through some process of reckoning with the costs and benefits. So who, in the Australian debate is arguing this in terms of relative costs and benefits, rather than assuming it away by somehow collapsing it all into the question of setting the right interest rate or some other approach that doesn’t reckon with the costs of an interest rate that keeps the labour market from clearing? (Genuine, not a rhetorical, question by the way.)

Secondly I don’t think we can assume that this is a simple choice. Let’s say we think financial stability is very important. We still think that the inflation target and, by implication above NAIRU unemployment, are important. So these things need to be traded off to some extent. I take it the argument of Chris Joye et al is that we’ve already traded off too far at a 1.5% cash rate.

The problem with this is that it keeps interest rates at a low level longer than they’d be low than the alternative, which is aggressively easing monetary policy to get the economy growing again. So the policy of leaning against one’s inflation target and giving more weight to financial stability is now quite possibly implicated in a longer period of low interest rates than a more aggressive policy of easing.

This is in fact the situation we’re in. You can object to how low the RBA went – down to 1.5% – but its current policy takes us where I’m talking about. And it seems like a pretty good way to blow bubbles. For probably about five years now, official forecasts have been for inflation not to rise out of its band and for unemployment to rise, flatline or fall very gradually. So if you’re thinking of borrowing to invest, now looks like a pretty good time. Rates will stay low for a long time. Is this more bubble resistant than getting rates down to zero, with a quite substantial exchange rate response, so that we can get them heading up as soon as possible – to keep those borrowing to invest a little more focused on downside risks in a year or two? My guess is that this lowers the risk of blowing bubbles.

I mentioned this to an RBA board member at the RBA dinner in Melbourne last March. I asked if this question had ever been raised on the board. They said no, but that it was the best question they’d heard in a year or so. What concerns me here is not that the bank might be wrong, but that the bank in its public accounting for its decisions and its publication of research papers doesn’t seem to be leading this discussion or trying to really structure that discussion so that we can have the best chance possible of getting to the right answer. It’s all much more by the seat of the pants.

One further thought. If people really are concerned about the prospect of bubbles, wouldn’t this also lead them to be arguing for more expansive fiscal policy so we can get this risky period of low-interest rates behind us and nip any bubbles in the bud as soon as we can – as well as returning the budget to surplus once we’ve restored the economy closer to capacity? But I don’t see that happening. Do you? If I’m right about this – and I’m not reading all the commentary on the cash rate so I may be missing something – then perhaps the explanation for where people come out on these issues has more to do with their temperament and their tendency to being ‘hawks’ or ‘doves’ on monetary policy, than it does with the more formal arguments they voice?

Good piece Gene, can I republish?

Graham

What is the likely effect on house prices if the ALP is elected (which seems likely) and abolishes negative gearing?