The ½ percent GDP contraction in September quarter that the ABS published last week has raised a lot of questions about the current state of the economy, and whether the Government should do more in terms of economic reform or fiscal stimulus.

Regarding fiscal stimulus, I agree with Finance Minister Mathias Cormann’s view reported in the Brisbane Times that it would be undesirable. It is very possible that the September quarter result was an aberration caused in part by volatile public sector capital expenditure numbers, and that there will be a bounce back in December quarter (see the decomposition of GDP growth in Queensland Treasury’s latest National Accounts brief). That said, it is clear the Australian economy is not as healthy as we thought it was earlier in the year, and the outlook for business investment is concerning.

Fiscal stimulus has historically proven to be ineffective or counter-productive in stabilising the economy. There are at least two major problems with fiscal stimulus.

- First, there are recognition, decision and implementation lags, which mean that fiscal stimulus will likely impact an economy after the need for it has passed, risking an over-heating economy on the upswing.

- Second, by increasing government borrowing, fiscal stimulus can put upward pressure on interest rates, attracting foreign capital into the country, leading to a currency appreciation, discouraging exports and encouraging imports (i.e. impacts that act in a direction contrary to the fiscal stimulus).

The second point is the well-known critique derived from the Mundell-Fleming model, which Tony Makin has effectively used in critiquing the Rudd Government’s fiscal stimulus packages in response to the financial crisis, most recently in a paper commissioned by the Treasury. Makin is correct the National Accounts data show that what appears to have saved the Australian economy at the time of the crisis was actually a depreciation of the currency in 2008, related to interest rate cuts by the RBA, and a boost in net exports, rather than the fiscal stimulus.

I should note that while I largely agree with Makin’s ex post analysis, I was working in the Treasury in 2008-09, and at the time I thought fiscal stimulus was warranted given the expectation that Australia would receive a huge adverse shock from the global financial crisis. Treasury officials thought that the crisis was of such an exceptional nature that it warranted it a strong and timely response. Treasury was well aware of the traditional problems in implementing fiscal stimulus packages, and Treasury Secretary Ken Henry reflected that wisdom in his famous advice to the Government that it should “go hard, go early and go to households”. I recall I had some reservations about the size of the second stimulus package in February 2009, but I had no doubt a stimulus package was necessary based on the economic outlook at the time. In my view, given the extraordinary circumstances at the time of the financial crisis, fiscal stimulus was appropriate ex ante, although it now seems to have been unnecessary and undesirable ex post.

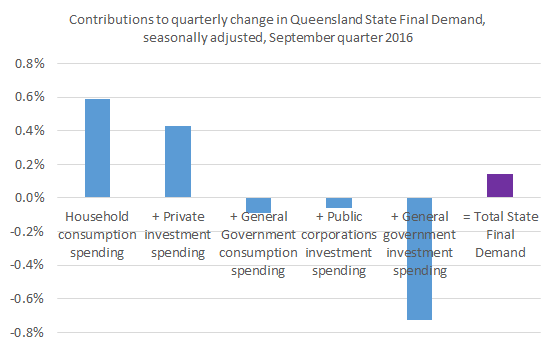

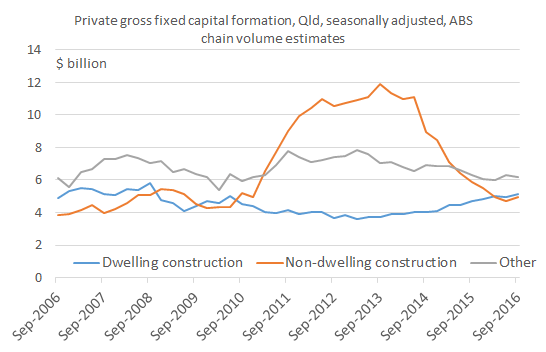

Finally, returning to the September quarter National Accounts figures, Queenslanders should take comfort from the fact that Queensland’s economy appears not to have contracted, registering a slight increase in State Final Demand in the quarter. Encouragingly, private sector capital investment is increasing, with non-dwelling construction activity starting to grown again after its steep decline at the end of the mining boom (see charts below).