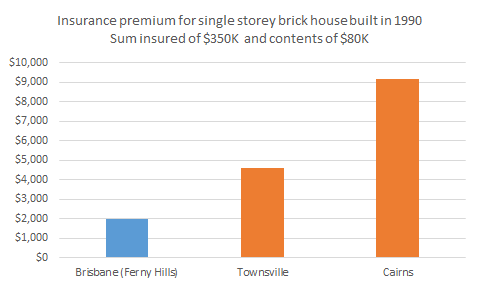

Since Cyclone Yasi, insurance premiums have soared in North Queensland as insurance companies have reassessed the risks of insuring properties in the region. Just how much premiums have increased is illustrated by some figures provided to the Joint Select Committee on Northern Australia by Townsville City Council (see chart below).

These figures were reported on page 133 of the Joint Select Committee’s Final Report Pivot North: Inquiry into the Development of Northern Australia, which was released last week. The figure for Cairns looks extremely high, so I’m unsure if it’s typical. That said, it’s pretty clear from media reports coming out of North and Far North Queensland that there has been a big spike in insurance premiums.

These figures were reported on page 133 of the Joint Select Committee’s Final Report Pivot North: Inquiry into the Development of Northern Australia, which was released last week. The figure for Cairns looks extremely high, so I’m unsure if it’s typical. That said, it’s pretty clear from media reports coming out of North and Far North Queensland that there has been a big spike in insurance premiums.

The Committee is right to see high insurance costs as a barrier to the economic development of the North, but I disagree with its recommendation that the Federal Government consider establishing an insurance office for Northern Australia that would provide subsidised insurance cover. That would be unfair to taxpayers in the rest of Australia, and it would ignore the possibility that insurers are right to be concerned about the risks from natural disasters in Northern Australia. Given these risks, the Government may want to reconsider promoting growth in the North beyond that which would occur naturally. Of course, it’s possible that insurance companies have over-reacted in the wake of Cyclone Yasi, but I think they’re in a better position to judge the risks than the Federal Government.

Thanks to Mark Beath of Loose Change for alerting me that the inquiry report has come out. Mark has commented extensively on strata insurance issues in Far North Queensland since Cyclone Yasi. For example, see Mark’s post:

No, it wont impede, it will make poor people not come which will be fine until the rich people need them!

Thanks. I must do an update on where the insurance issue is at. Conditions in the reinsurance market are considerably improved in the past year with premiums if anything now easing slightly for strata and some further competition entering the NQ market.

I agree with you on the TIO and should also point out that the TIO as a remaining ‘state’ insurer is also the only insurer in Australia not operating under APRA prudential supervision. I don’t think insurance in Darwin is as significantly cheaper relative to risk as many believe. My understanding now is that despite Cyclone Tracy the historical risk in North Queensland and the WA coast is higher.

An issue here also that I like to bang on about is reform of the insurance stamp duty. When the stamp duty rate was hiked in 2013 the spin from Treasurer Tim included an example of an average house in Brisbane which is irrelevant for NQ as indicated in the graph posted above. The incidence of insurance stamp duty falls significantly harder in NQ. The replacement of an inefficient stamp duty with a more efficient broad based land tax would reverse that.

Thanks Mark. I completely agree with you regarding the need to reform stamp duty. An update on the insurance issue in FNQ would be great.

Gene

Agree entirely that Government should not intervene in prices in the insurance market. Also, the current approach to, and use of, stamp duty provides a perverse incentive to self manage risk. Why make the self management of risk in North Queensland even more expensive? The current use of stamp duty might be fiscally expedient, but it is economically dumb.

Insurance premiums are moving towards a better reflection of the risk associated with natural disasters. The insurance sector now has the tools to understand risk better and they are using them when setting premiums. This is a good thing.

I don’t agree that insurance premiums are a barrier to development in Northern Australia per se. Rather, the incorporation of risk (via insurance premiums) simply changes the investment metric. If you think of property as just a bundle of attributes (building, land, location, potential revenues, risk etc.), the increased risk costed into insurance premiums should simply be reflected in reductions in the value of other parts of the bundle (e.g. lower land prices). In an efficient land market, the value of the bundled product should reflect all of the attributes including the lifecycle cost of insurance.

There is currently an information asymmetry problem in the land market. Buyers rarely understand natural disaster risk until after they buy the property and try to get insurance (ouch!). Sellers (and the real estate industry) have a vested interest in suppressing information where it suits their interests. I am always amused (no dismayed) that there is more compulsory attribute information and consumer protection available on a $2 loaf of bread than there is for an auction for a $2 million property.

Thanks for the great comment, Jim. Very good point about levels of consumer protection.