Prior to the omicron outbreak, I was very confident about the Queensland economic outlook for 2022. I’m still reasonably confident that the state economy will perform well over 2022, but nothing is certain of course. There’s been a bit of worrying news in recent days about hospitality venue closures and shortages of products in supermarkets. Hopefully, those issues are resolved and are only temporary. So much depends on the COVID response, and so far this year the Queensland Government has botched it, alas, with a lack of COVID testing capacity. But let’s assume we get through this COVID wave without a catastrophe that sees people retreat back to their homes and businesses shut down for an extended period.

For my first post of 2022, I’ll run through the state of play for the Queensland economy and what some of the important leading indicators are saying.

State of play

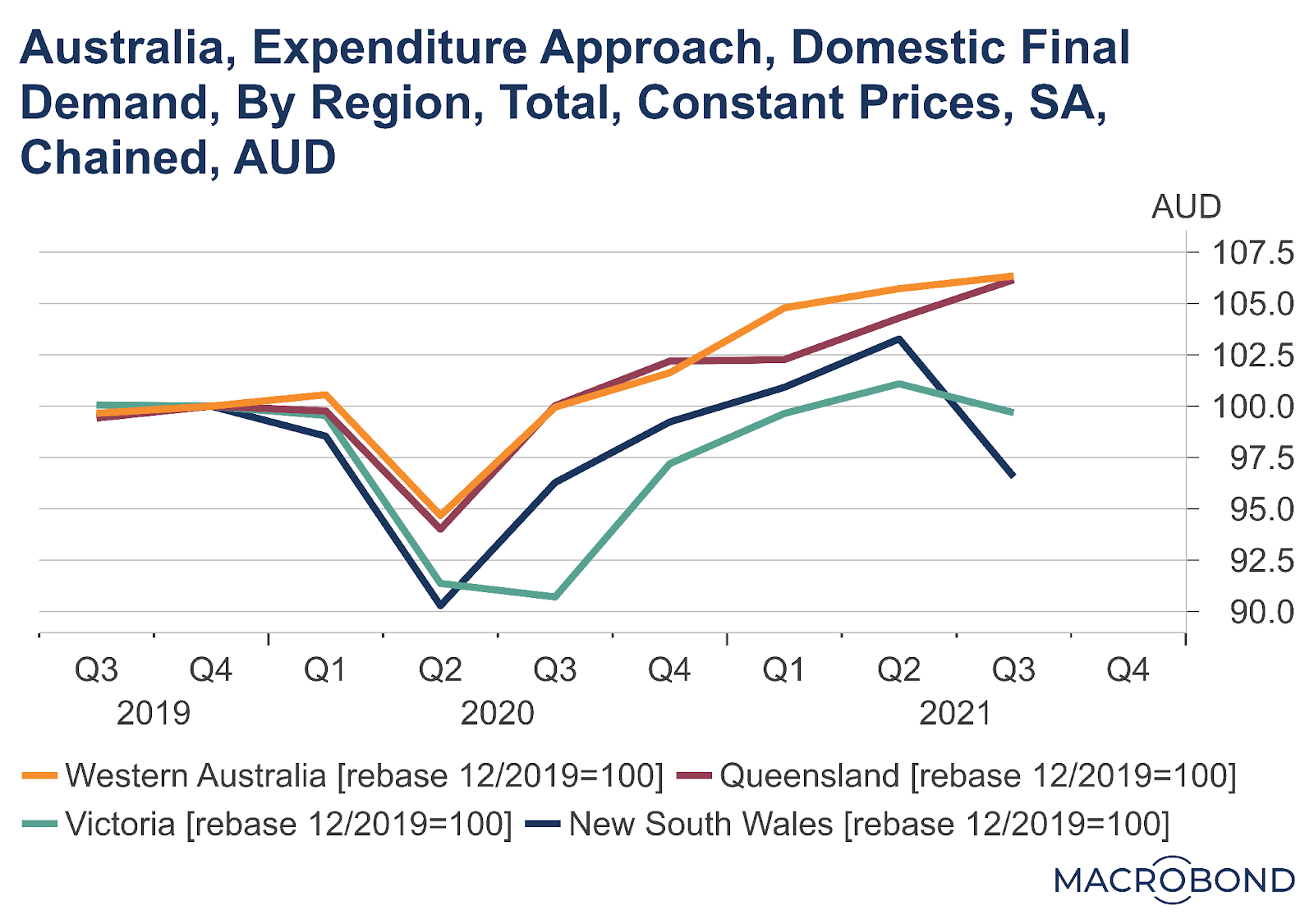

The most recent ABS National Accounts data were for the September quarter, in which Queensland obviously performed very well compared with the other major states, NSW and Victoria, which were locked down for extended periods that quarter. As the Queensland Mid Year Fiscal and Economic Review proclaimed, state final demand in Queensland was 6.4% up on its pre-COVID level, compared with only a 1% improvement for Australia as a whole, which was dragged down by negative results in NSW and Victoria (see chart below).

So Queensland has recovered very nicely from the initial COVID downturn in the first half of 2020. I should note disproportionate contributions to that recovery have been made by government spending and capital investment in renewable energy, as I pointed out in a post last month (Gov’t and renewables making disproportionate contributions to demand growth in Qld).

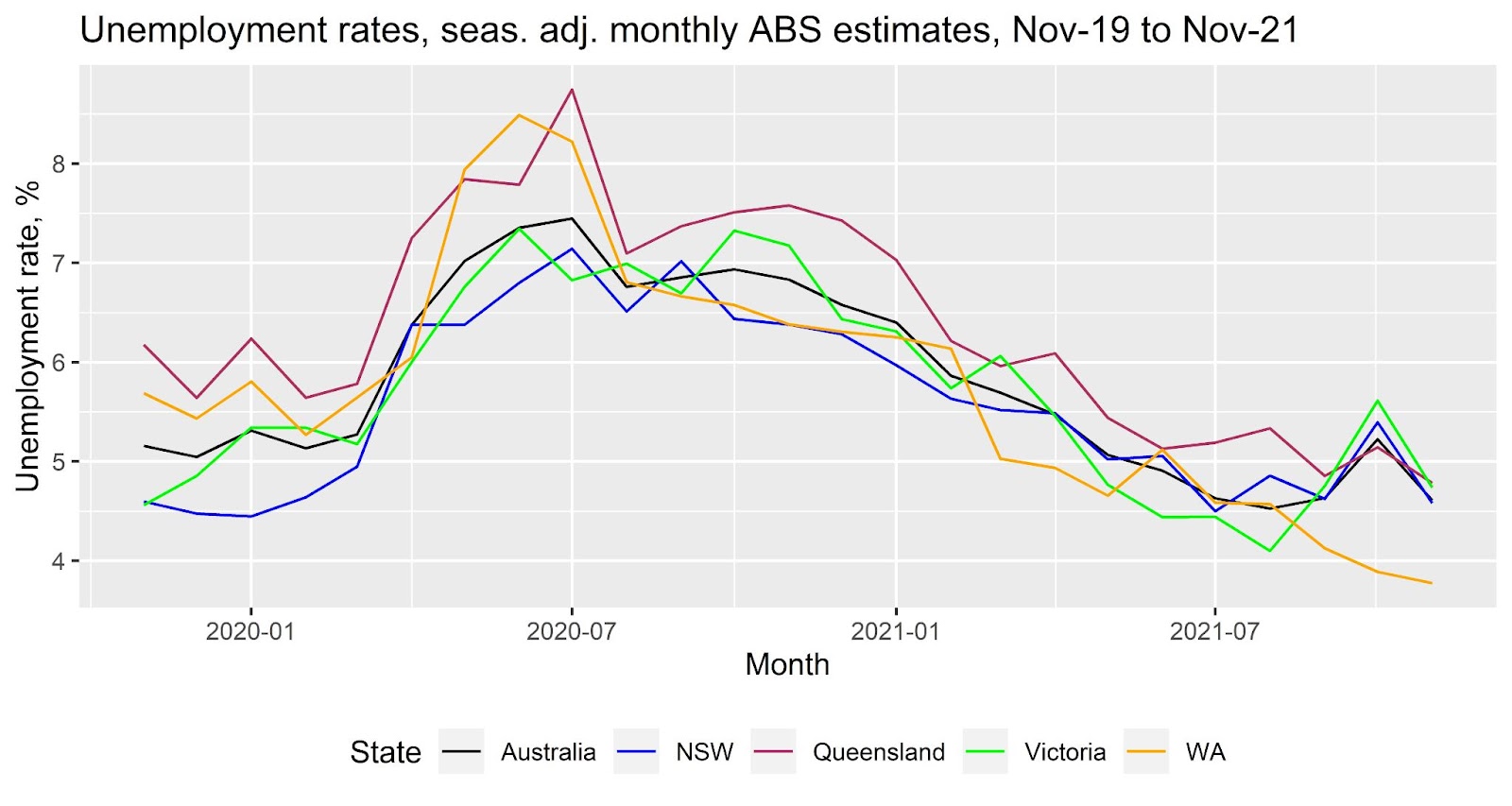

The robust recovery and also the lack of new overseas immigrants adding to labour supply have pushed down Queensland’s unemployment rate to 4.8%, not much higher than the national average of 4.6% (see chart below).

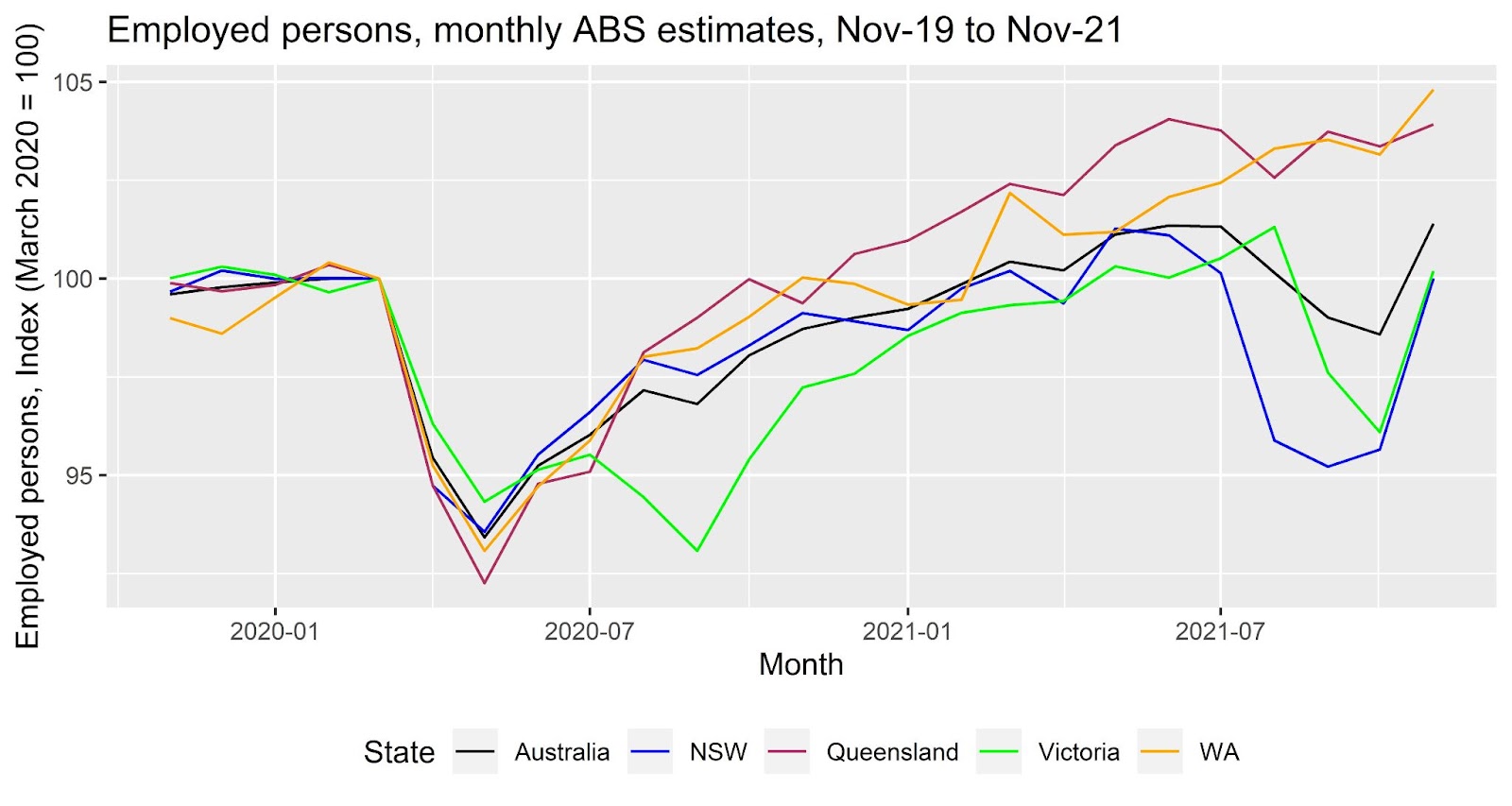

Employment is 3.9% higher than its March 2020 level (see chart below).

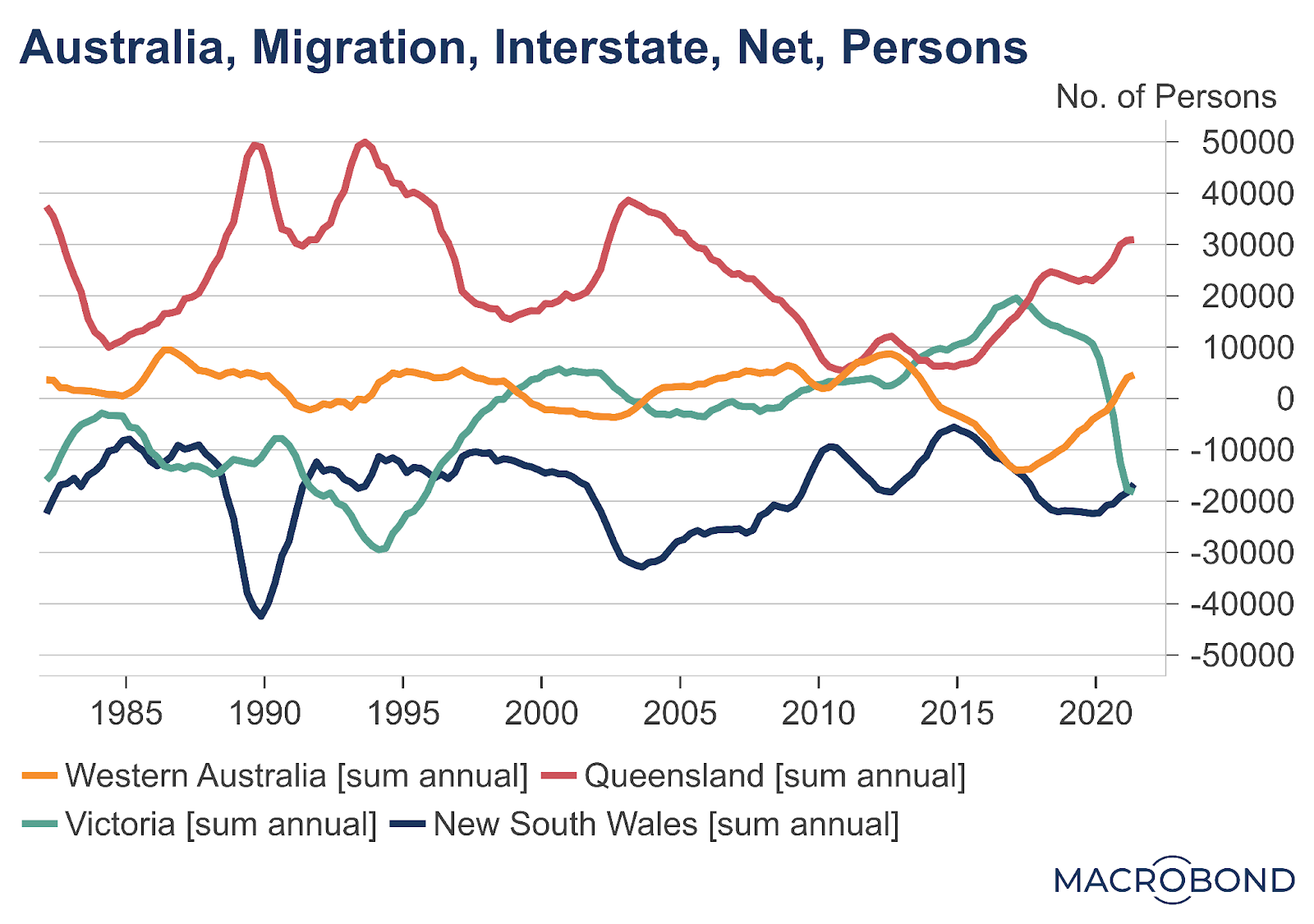

While we haven’t been gaining people from overseas, Queensland has experienced a pick up in interstate migration, which can be taken as a vote of confidence in the economic outlook or Queensland’s (up until now) superior COVID performance to the rest of Australia. Queensland gained over 30k people in 2020-21 from net interstate migration, while NSW and Victoria lost 17k and 18k people (in net terms) respectively (see the ABS report National, state and territory population). Queensland’s population increased 0.9% compared with a national average of 0.2%, which was dragged down by a 0.7% fall in the population of Victoria, which was a pretty awful place in 2020-21 given the COVID outbreaks and the lockdowns imposed by the Victorian Government.

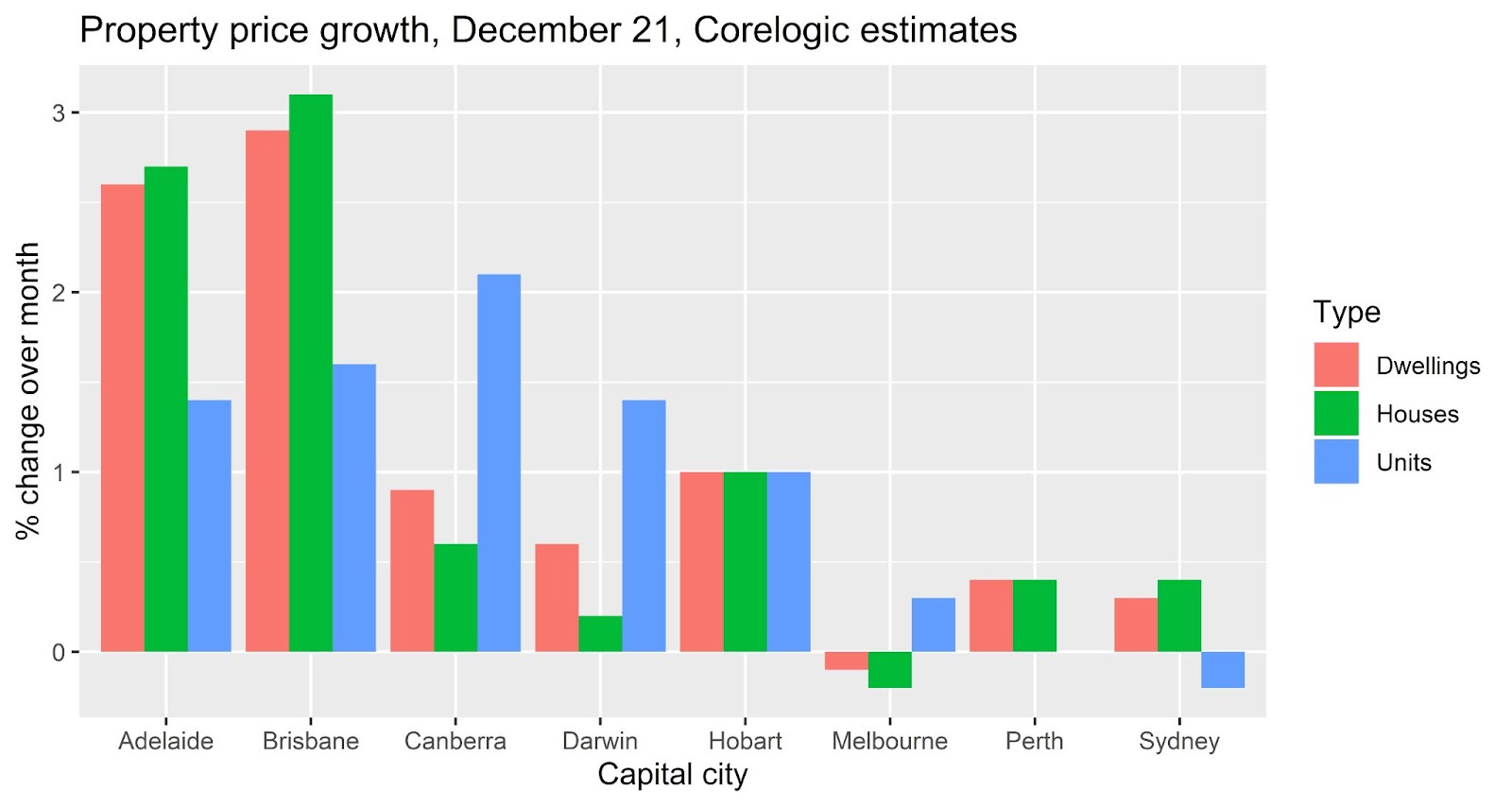

Alongside strong housing credit growth, interstate migration to Queensland is contributing to extraordinary property price growth. Brisbane housing out-performed housing in all other markets in December (see chart below).

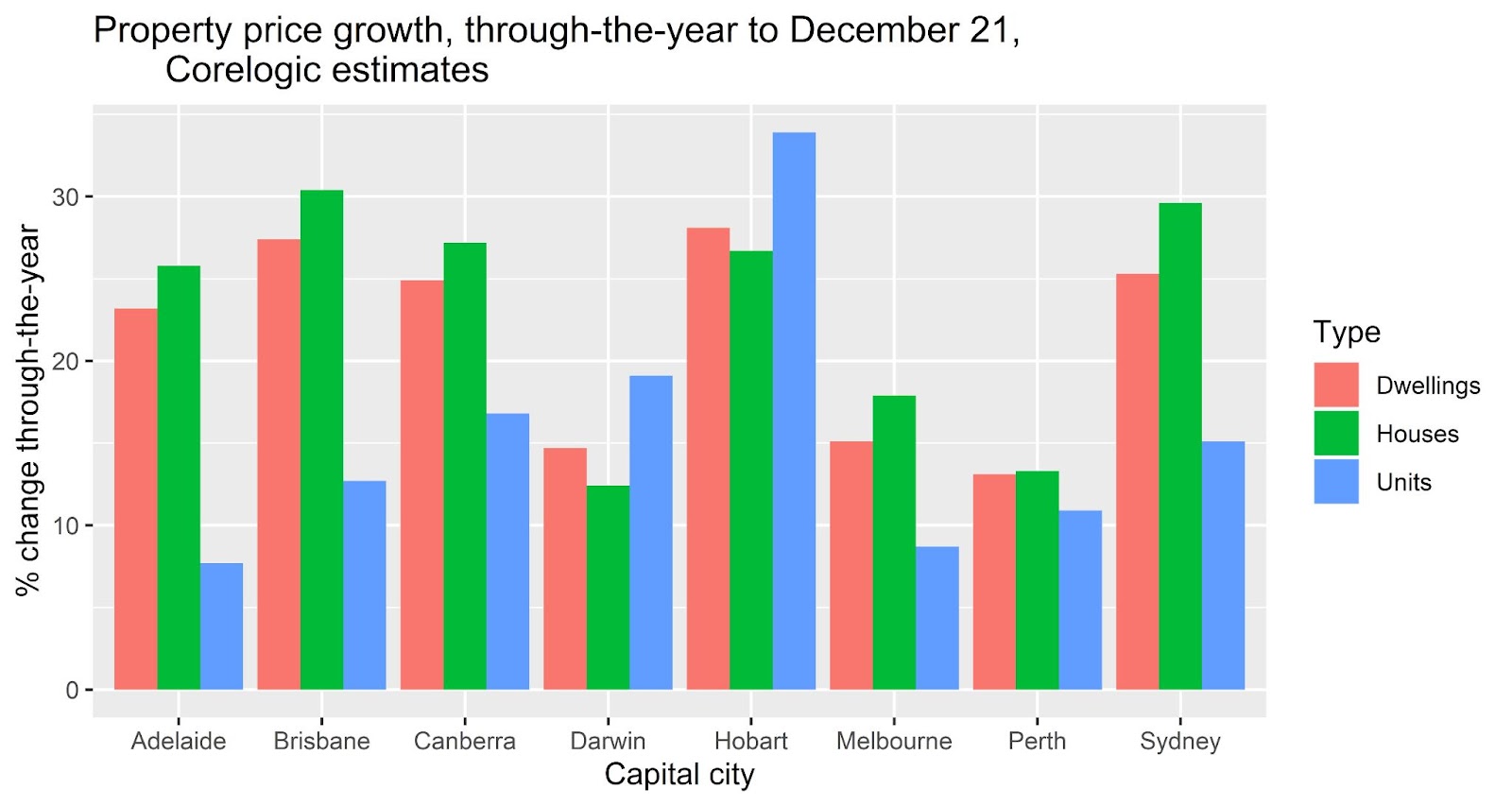

As is well known, property prices experienced double-digit growth across Australia in 2021 (see chart below). Market watchers are expecting lower growth rates in 2022. The market is cooling in NSW and Victoria, where prices have got to very high levels, but it hasn’t shown signs of cooling in Queensland yet. Corelogic’s media release on its December data observed:

Brisbane and Adelaide, along with regional Queensland, are the only broad regions where there is no evidence of value growth slowing just yet, with the monthly rate of growth reaching a new cyclical high in December.

CoreLogic’s Research Director Tim Lawless said: “These regions show less of an affordability challenge relative to the larger capitals, as well as better support for housing demand with Queensland in particular showing strong interstate migration. Additionally, we haven’t seen the same level of supply response seen in other regions, with the trend in advertised supply remaining well below average in these markets.”

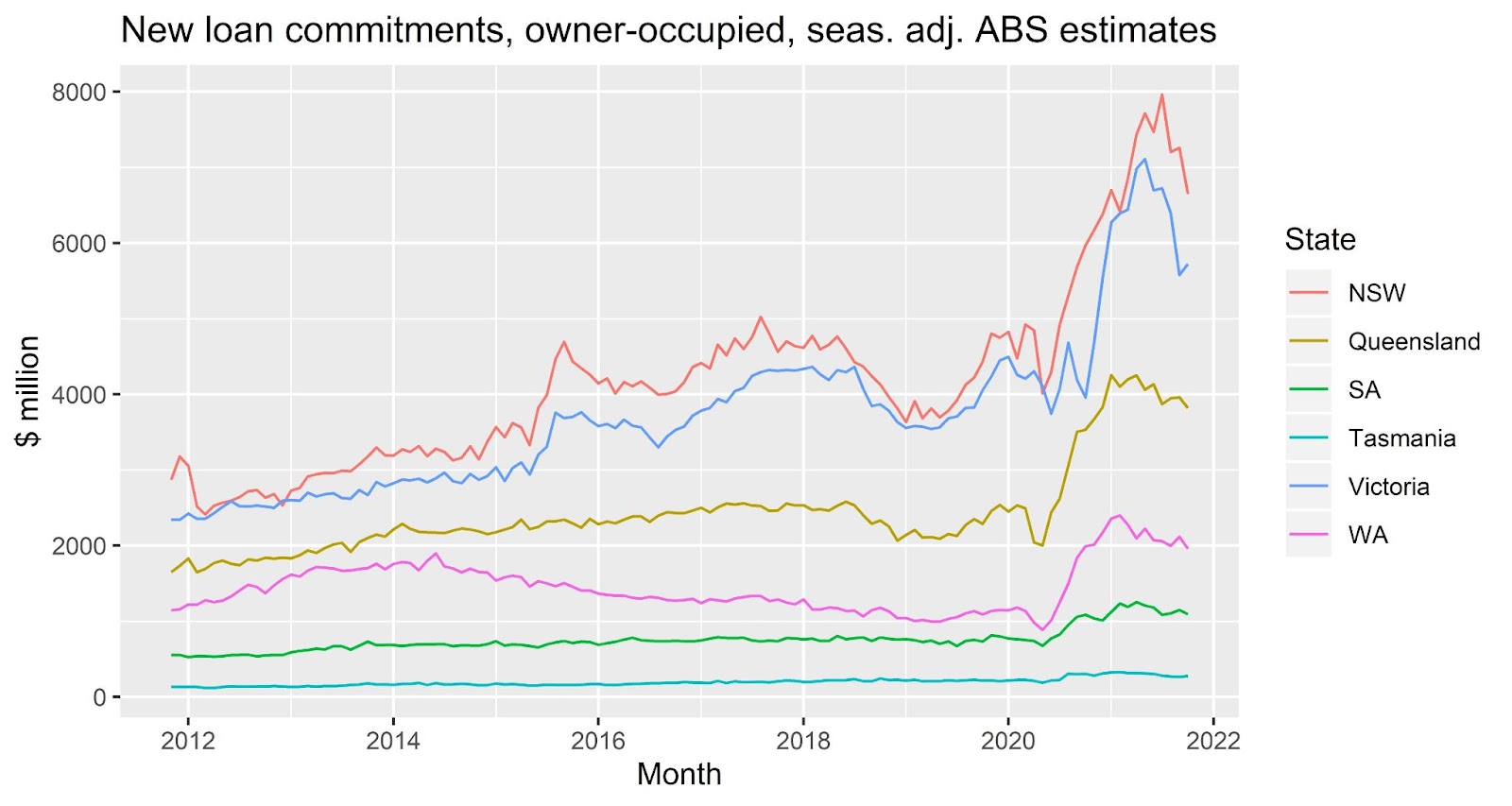

Lending for housing remains high although it’s coming off its peak for owner occupier lending, more so in NSW and Victoria than in Queensland (see chart below, showing monthly ABS estimates up to October 2021).

That said, lending to property investors is still increasing in Queensland (see chart below), and as a result total lending for housing (excluding refinancing) is still at a record high. In Queensland, in seasonally adjusted terms, total lending was $5.92 billion in October 2021 compared with $4.40 billion in October 2020 and $3.30 billion in March 2020, the month usually taken as the pre-COVID baseline. As is well known, one of the extraordinary features of the pandemic has been the massive growth in housing credit and property prices, driven by a combination of ultra-loose monetary policy, government incentives, and a fear of missing out (FOMO).

Future interest rate increases are likely to contribute to a slow down in property price growth. These are to be expected given expectations of accelerating inflation. That said, there is a divergence of views between the financial markets and the RBA. As reported in The Australian on Monday, Australian markets betting on three interest rate rises this year. Incidentally, banks have already started increasing fixed interest rates, as they are expecting floating rates to increase over the terms they offer fixed rate mortgages (see NAB says Merry Christmas with another rate rise). In defiance of market expectations, the RBA Governor has said he doesn’t expect to increase the cash rate next year. Of course, depending on how things go, the RBA may be forced to if the core inflation measure (2.1% through-the-year to September quarter) accelerates to beyond the target range of 2-3%.

Leading indicators

Now that we’ve reviewed the current state of play (or as close to current as we can get given available official data), it’s time to consider some leading indicators of activity.

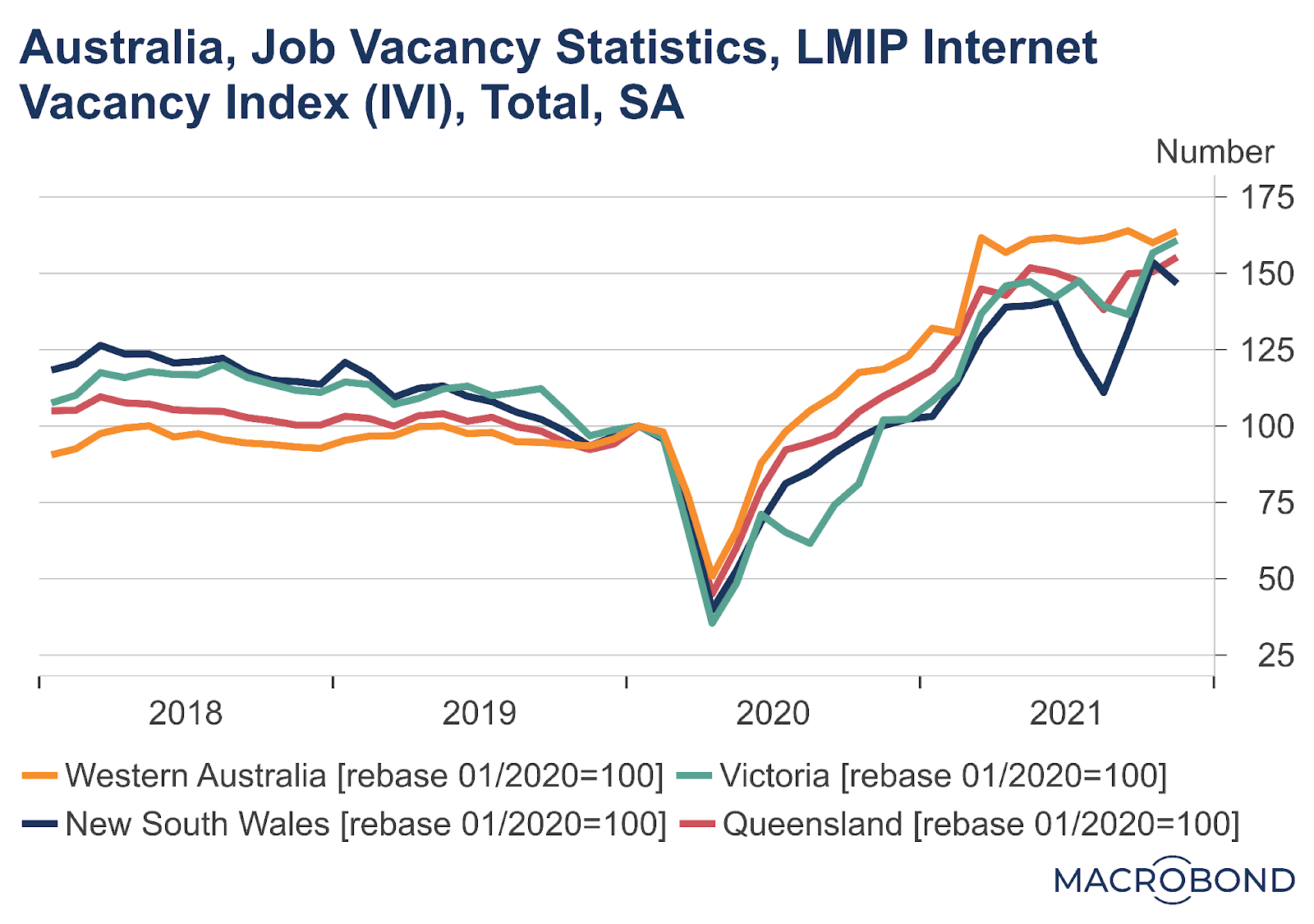

First, job vacancies have been very strong, partly because employers have had to fill positions vacated by foreigners who’ve gone home during the pandemic. The data in the chart below are the National Skills Commission’s Internet Vacancy Index data and are current up to November 2021.

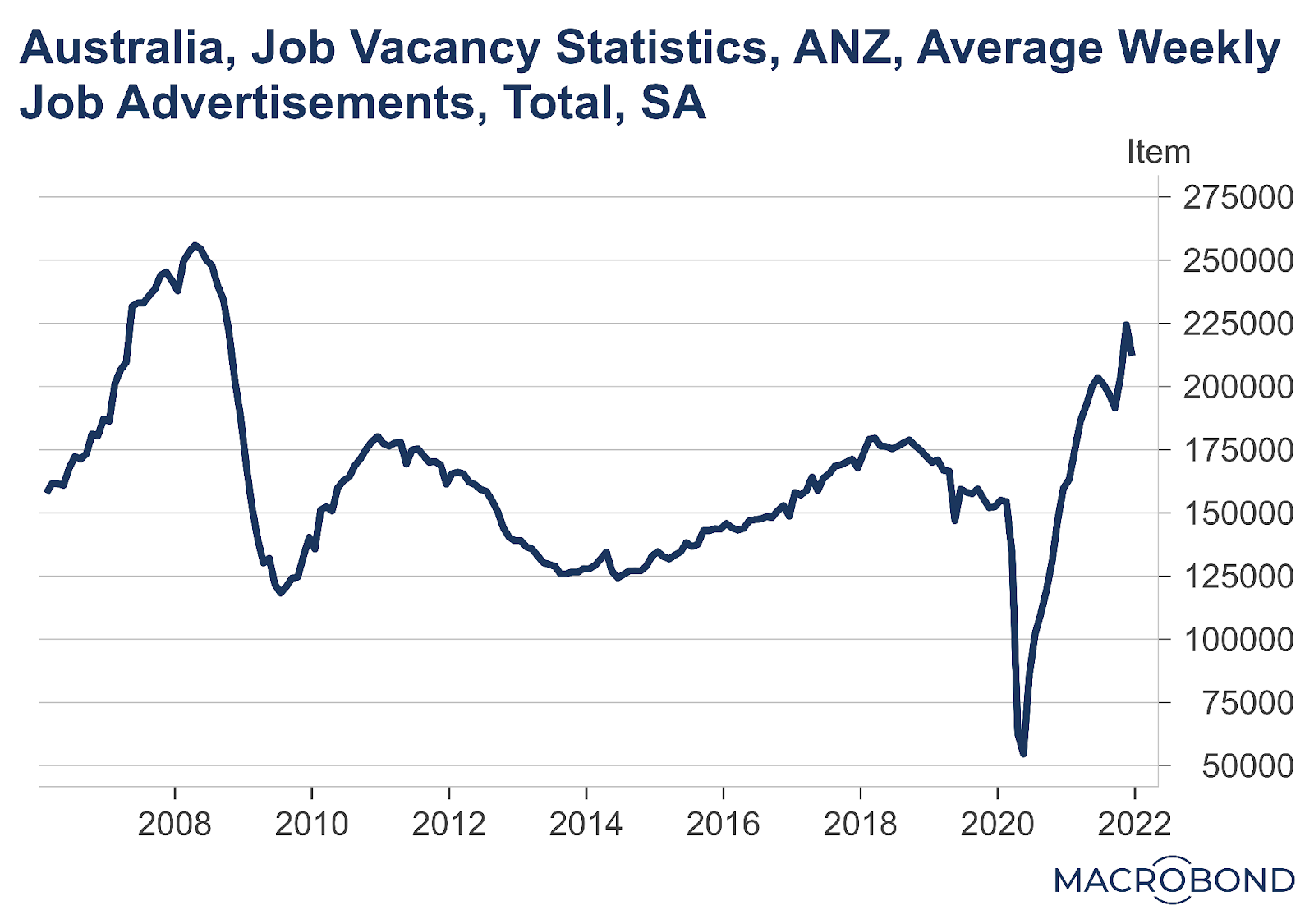

ANZ job ads data for Australia show a fall in job vacancies in December, but vacancies remain much higher than pre-pandemic levels (see chart below).

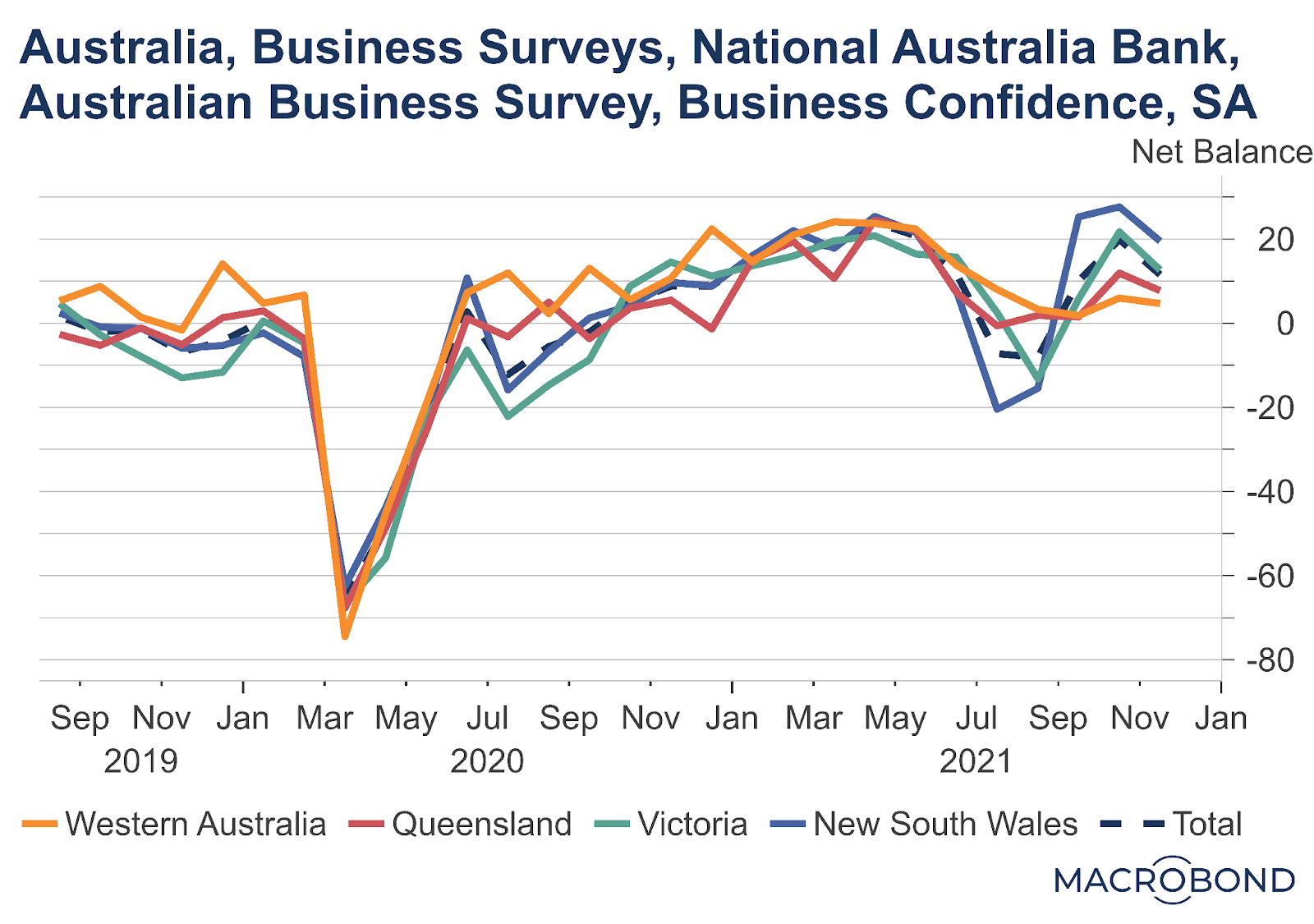

Second, business confidence remained significantly in positive territory in November, although Queensland businesses were less confident than those in southern states (see chart below).

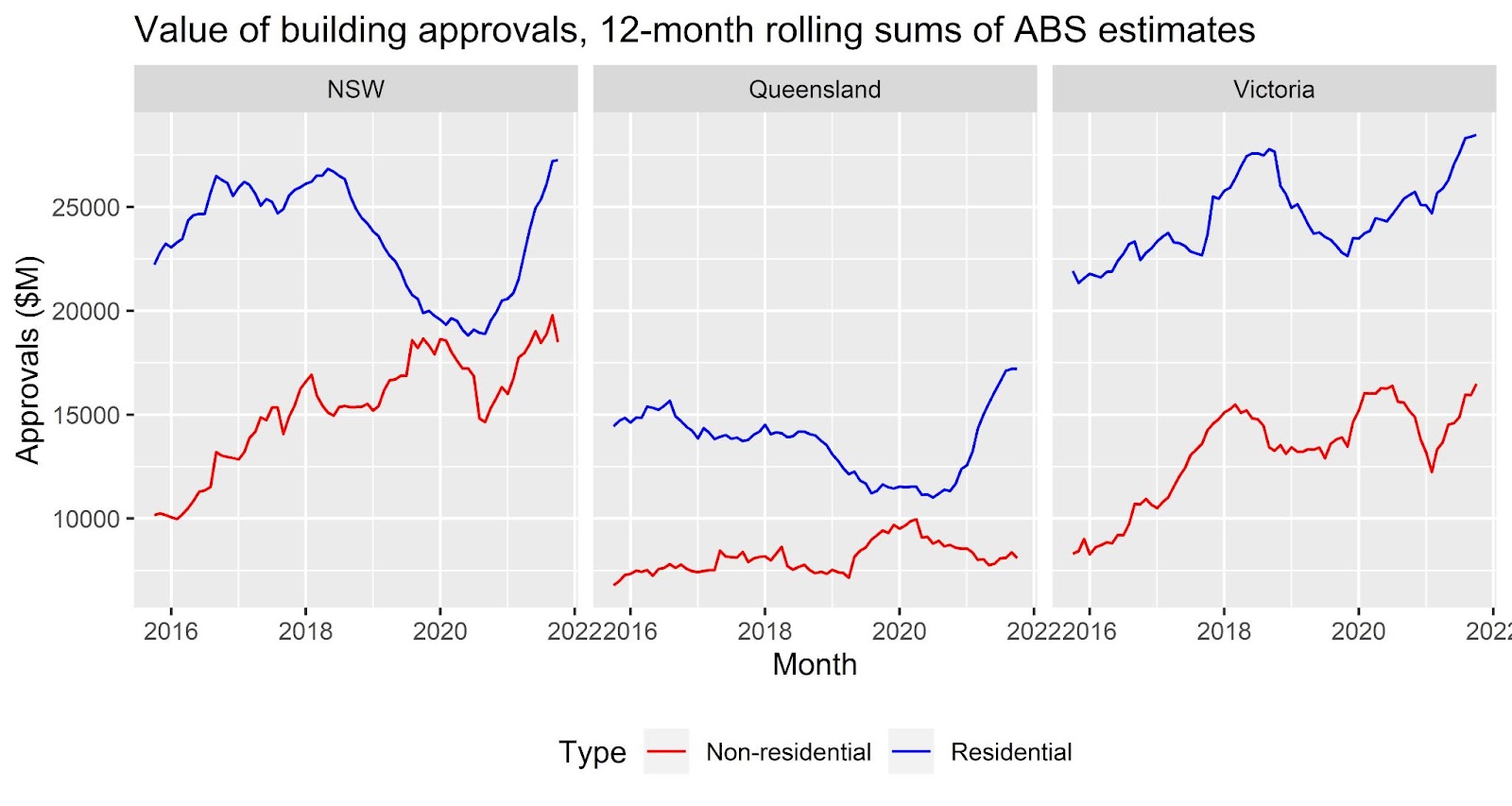

Regarding the construction industry, an important bellwether for the economy, residential building approvals have been strong (see the chart below using ABS estimates up to October 2021), but non-residential approvals haven’t seen the same sort of pick up in Queensland as has occurred in southern states.

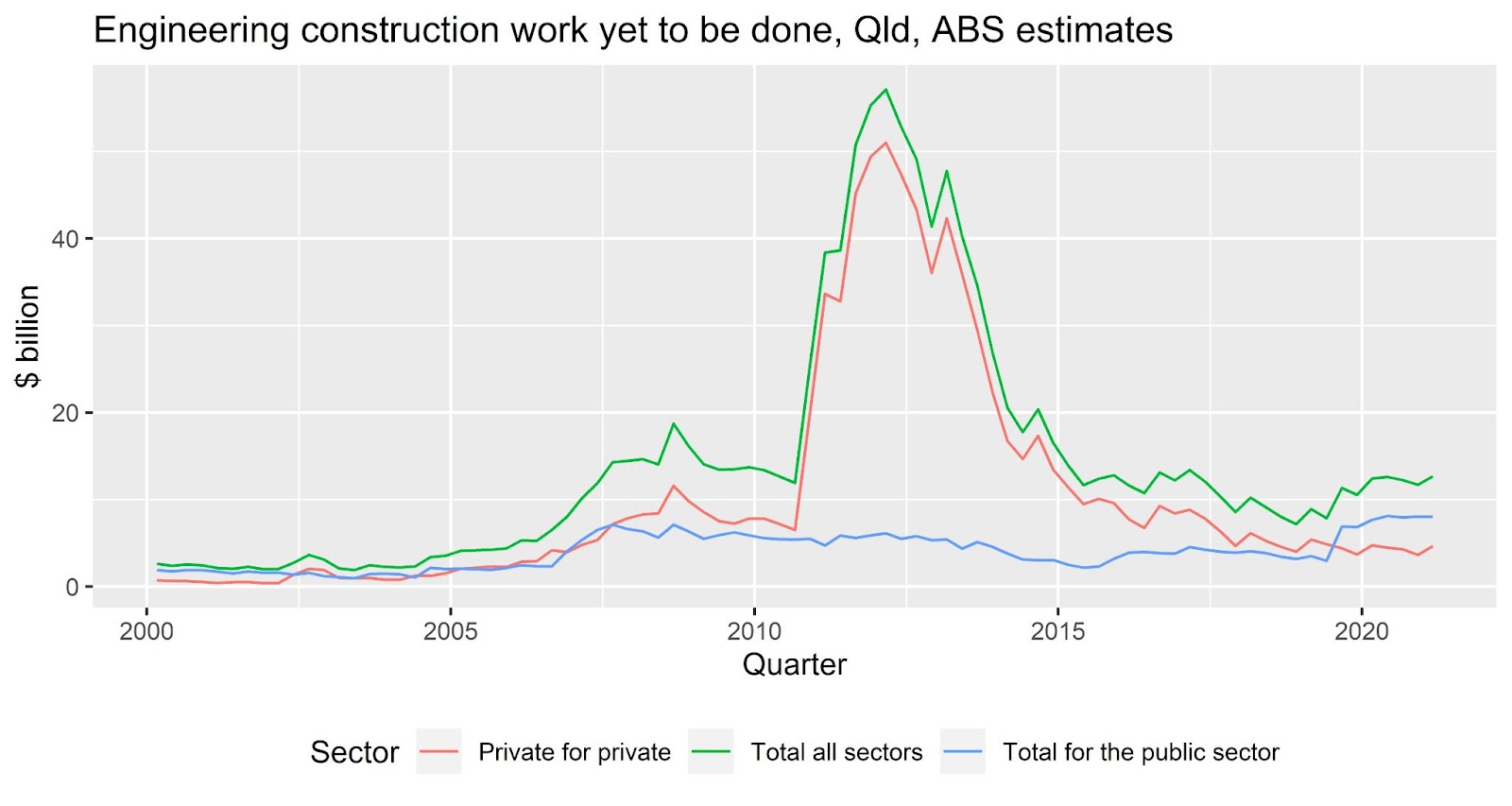

Engineering construction work yet to be done (i.e. the infrastructure “pipeline” of work) has been at a higher level than in recent years due to major projects such as Cross River Rail (see chart below, noting the latest ABS estimate was for June quarter 2021), but it’s nowhere near the super high levels seen during the boom years last decade when the Curtis Island LNG plants were being constructed. It’s also lower than it was during the Bligh Government’s infrastructure splurge in the late 2000s, and that discrepancy would be even larger if I’d used real (i.e. inflation-adjusted) rather than nominal data.

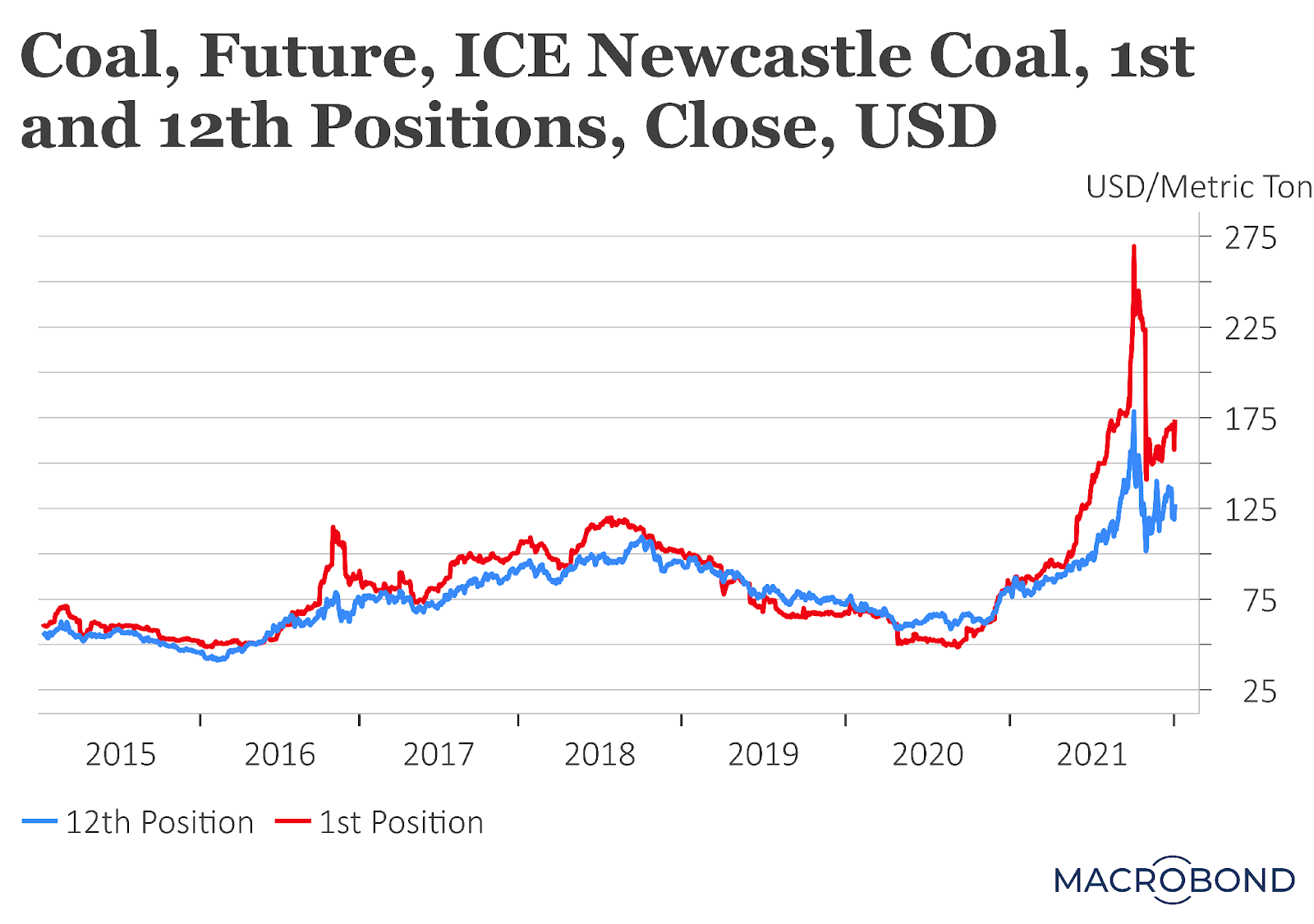

Coal prices

Given its importance to many of Queensland’s regional economies and to the state Treasury through royalties, it’s important to consider the outlook for coal. In the charts below (see the first chart below for coking coal, the second chart for thermal coal) using futures prices up to 4 January, the 1st position line gives an indication of what coal is currently selling at and the 12th position line gives an indication of market expectations of the price in twelve months’ time. While current prices have fallen from their peaks, they still remain high, especially for coking or metallurgical (i.e. steel making) coal. Prices are expected to fall over the next twelve months, but would still be pretty good.

Conclusion

Queensland Treasury’s Mid Year Fiscal and Economic Review was right to note the state’s strong economic recovery and Queensland’s superior performance to other states. The current state budget forecasts are for good, but not exceptional economic growth (3.25% in 2021-22 and 2.75% in 2022-23). These forecasts seem reasonable to me. We’ll have a growing economy, but not one which is growing at boom year rates (e.g. the 5.8% growth in 2011-12 or the 6.8% in 2006-07).

Generally, Queensland’s economic outlook is good, but no one has a crystal ball, particularly during this time of omicron. There are big risks to the global and domestic economic outlooks, from Evergrande and China, and from COVID. I’ll be watching these things closely and updating my views, if necessary, on this blog in the coming weeks.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.

It won’t get any better while we still have people needing to get tested.

The policy to get tested while not having sufficient testing facilities means staff can’t gets tested and thus cannot work, resulting in the collapse of the supply chain.

The issue is made even worse by the termination of those who are unvaxxed meaning there is now even less health service operators available.

Are you sure the graph isn’t upside down?