In Queensland, our over-reliance on the public sector continues, according to the September quarter National Accounts figures from the ABS, which have reinforced concerns about the strength of the national economy and various state economies, including Queensland’s. The National Accounts revealed a Queensland economy in which domestic sources (i.e. excluding exports) are barely contributing to growth (see my QEW post on the new data). State Final Demand grew by only 0.1% in September quarter.

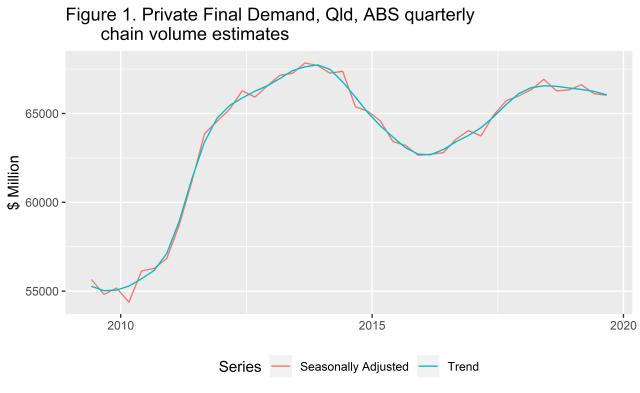

In his analysis of the latest National Accounts data at his Conus blog, Pete Faulkner has made a striking observation, which I’ve illustrated in Figure 1:

“Growth in the domestic QLD economy is almost exclusively from the public sector with the private sector as a whole now declining. Indeed, the total private sector has seen (slight) declines in all of the past 5 quarters and is now 0.7% below the level seen in the second quarter of 2018.”

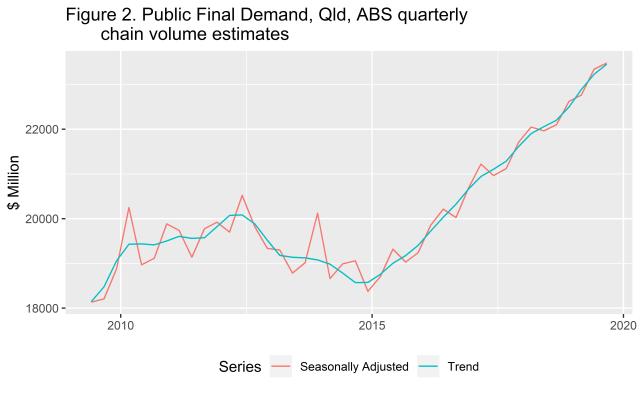

Pete goes on to note “The Public sector, over the same period, has increased by 6.5%”, which I’ve illustrated in Figure 2, but please note the different y-axis scales on the two charts. Queensland Treasury in its National Accounts State Details briefing has observed “Public final demand continues to be the main driver of SFD [State Final Demand] growth”.

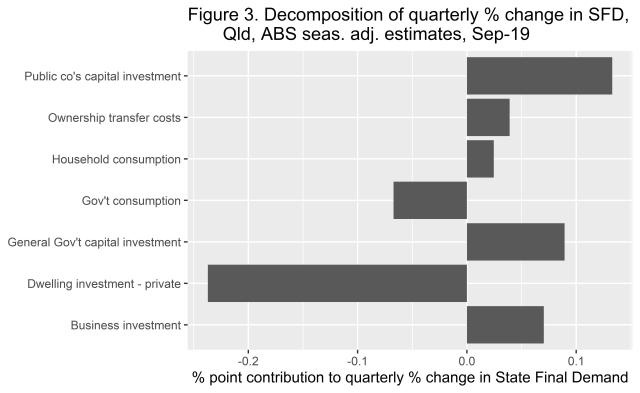

In Queensland, the end of the apartment building boom has meant that private dwelling investment continued to subtract from State Final Demand in the September quarter (Figure 3). Government capital investment has been adding to demand, but this was partly offset in September quarter by a fall in general government consumption expenditure (i.e. non-capital expenses including on employees), due to a 2.7% fall in State and Local expenditure, related to extra-high expenditures earlier in the year due to flood remediation works (see the ABS commentary).

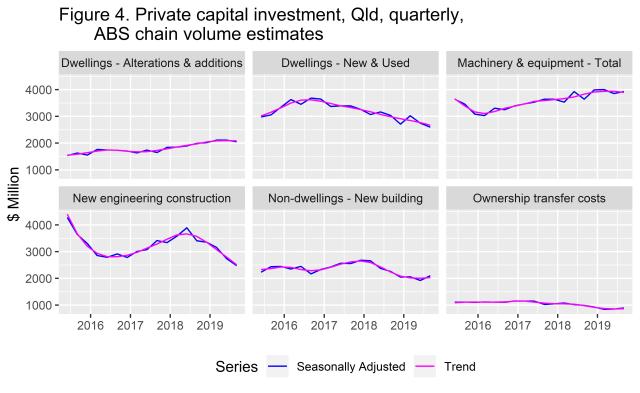

While it was once a major contributor to growth in the Queensland economy, during those mining investment boom years in the first half of the decade, private sector engineering construction activity has been falling and continued to do so in September quarter (Figure 4).

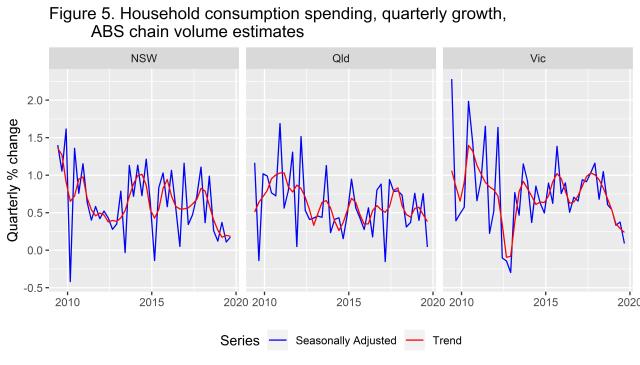

Queensland businesses aren’t investing at the levels we need for a healthy economy and consumers aren’t confident and spending money either. We’ve seen growth in household consumption expenditure fall to such a low quarterly growth rate that it rounds to 0.0% in the seasonally adjusted data (Figure 5).

At a national level, exports contributed positively to growth, but that appears to have been a result of strong growth in exports out of WA. According to the balance of payments data published the day before the National Accounts, credits for goods and services exports out of Queensland were 2.5% lower in real terms in September quarter than June quarter, using the seasonally adjusted data. So don’t expect exports to have saved the Queensland economy in September quarter. I should note that debits for imports of goods and services fell, too, and by slightly more than exports, so net exports (i.e. exports minus imports) might end up boosting Queensland’s September quarter GSP growth rate marginally above the extremely weak 0.1% estimate for State Final Demand growth.

Queensland’s labour market appears a lot better than the National Accounts would suggest, with employment still growing, albeit modesty according to ABS Trend estimates reported by Queensland Treasury in its Labour Force briefing. It’s likely the impacts on the labour market will show up with a lag, as empirical data suggest they do, so we need to watch how the labour market begins 2020. The National Accounts data and recent ANZ job ads data suggest it won’t be a great start to the new year.