In an opinion piece published Monday, the Courier-Mail’s Des Houghton rightly highlighted the huge challenge new Queensland Treasurer Jackie Trad faces in reining in spending, particularly given the significant burden placed on the budget by the interest on general government debt:

With state debt forecast to top $81 billion in two years Queenslanders will be paying in excess of $10 million a day.

In fact, I’m told the daily interest rate bill may have already topped $10 million.

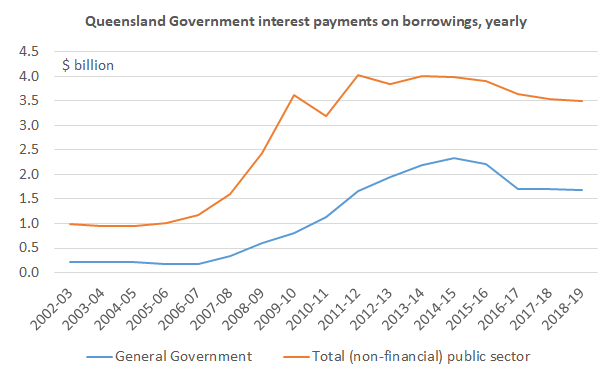

According to the latest Report on State Finances, in 2016-17, total Queensland Government interest expenses on borrowings were $3.637 billion. Note that this amount has fallen from its peak a few years ago as the Queensland Treasury Corporation has refinanced debt at lower interest rates (see chart below, noting the figures for 2017-18 and 2018-19 are Queensland Treasury forecasts). The total interest bill includes interest expenses by the general government sector and government-owned corporations. In daily terms, interest payments are indeed around $10 million. The daily interest bill would be even higher if the imputed interest on the government’s superannuation liability were added on. This was an estimated $510 million in 2016-17, and would bring the daily interest bill up to $11.4 million.

On the distinction between general government and government-owned corporation debt, see my October post:

Looks fine to me. What do you think the optimal level of debt is? It’s just a transfer anyway to owners of State government bonds.

Thanks for the comment Cam. Yes, it’s a transfer but the bulk of the transfer would go to beneficial owners outside of Queensland. Regarding the optimal level of debt, I don’t think a precise number can be put on it, but I’d at least be aiming for a debt lower than 100% of total revenues, so we could get our AAA credit rating back. This would mean a total debt of no more than $67 billion in mid-2021, compared with the currently projected $81 billion.