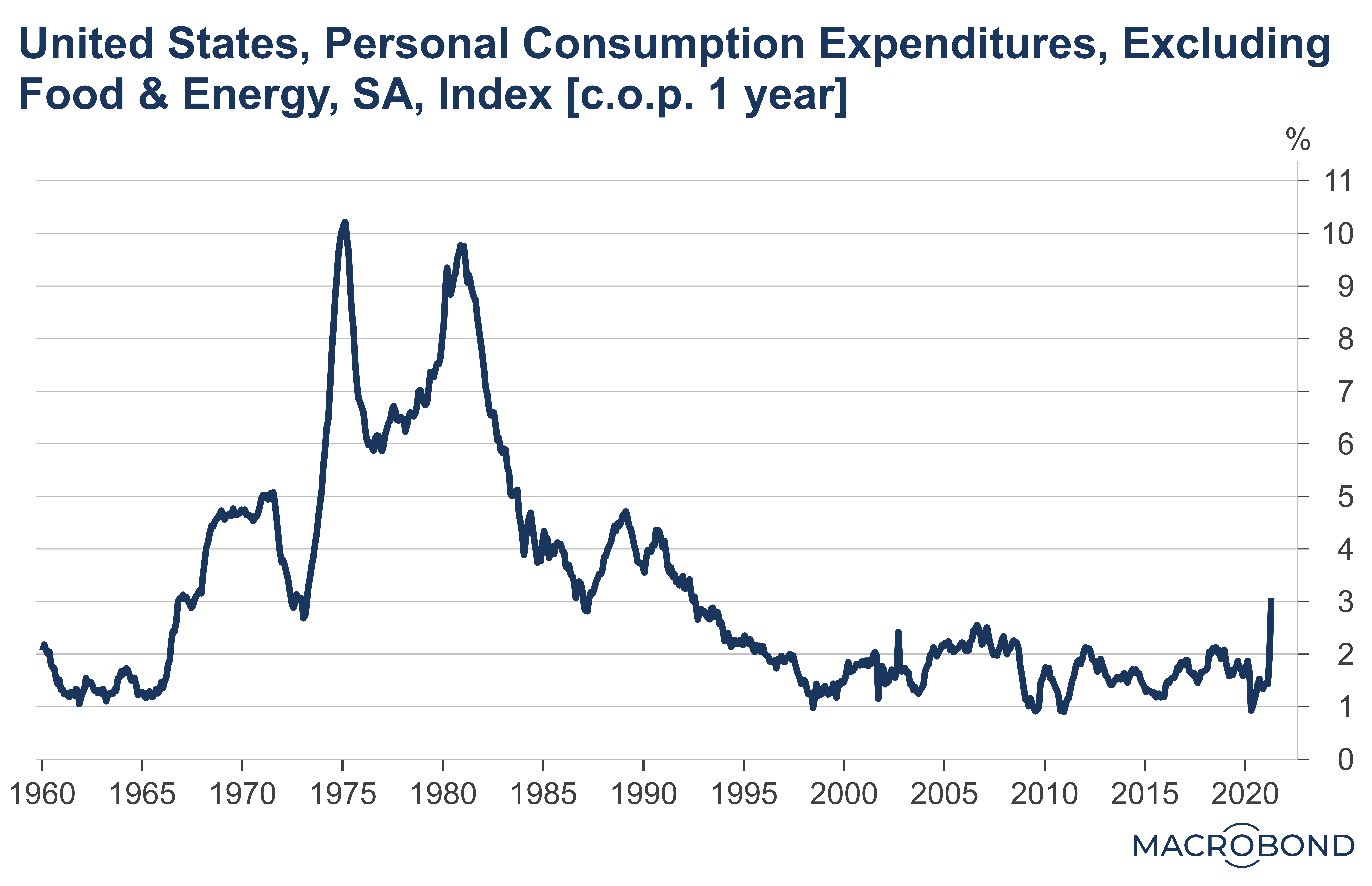

Setting off an inflationary spiral is one of the big risks with the mega-stimulus measures and Quantitative Easing or money printing we’ve seen in the responses of governments and central banks to the pandemic. This month, we’ve seen some higher-than-expected readings of inflation in the US, with the latest being the core Personal Consumption Expenditures (PCE) Index, which was up 3.1 percent through-the-year to April 2021, the biggest increase since the early nineties (see chart below).

There is a lot of disagreement about whether we should be worried about inflation. For instance, Harvard Professor and former US Treasury Secretary Larry Summers is concerned President Biden’s budget could overheat the US economy (check out this Bloomberg interview). That said, as the Financial Times Coronavirus Business Update email noted today:

Investors were relatively sanguine about the inflation data, which merely confirmed their belief that the recovery was stoking a rise in prices. Global government bonds, sensitive to rises in inflation that could diminish their returns, remained steady.

That is, the markets reacted to the latest inflation data with a collective “whatever”. Time will tell whether that’s a sensible reaction.

Last week, for my Economics Explored podcast, I spoke with someone who is concerned about the potential for spiralling inflation, my regular guest Darren Brady Nelson. You can now listen to our conversation which I’ve published as EP89 CPI inflation concerns with Darren Brady Nelson.

Regarding the outlook for inflation in Australia, let’s see how this current COVID outbreak develops and whether lockdowns over Winter will suppress the economy and any inflationary pressures.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com.