All week we have been hearing the awful news about all the dead cattle in North and North West Queensland as a result of the recent floods. An estimate of around half a million dead cattle has been suggested, although some sources are suggesting it could be much higher. At this stage the ultimate impacts are still unclear, although I understand the state government and industry peak bodies are currently developing estimates of the economic impacts. Given all the figures and claims that are currently being heard in the news, I thought readers may be interested in some facts that can usefully inform economic impact estimates.

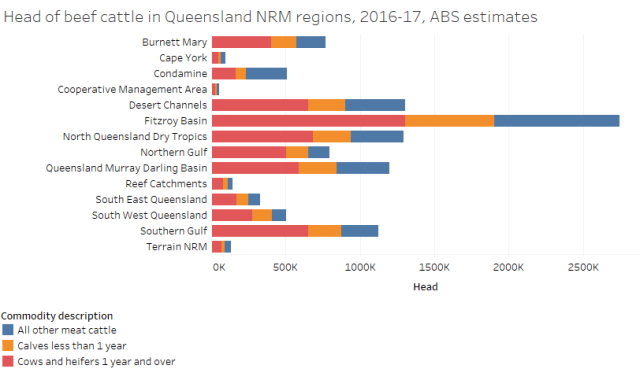

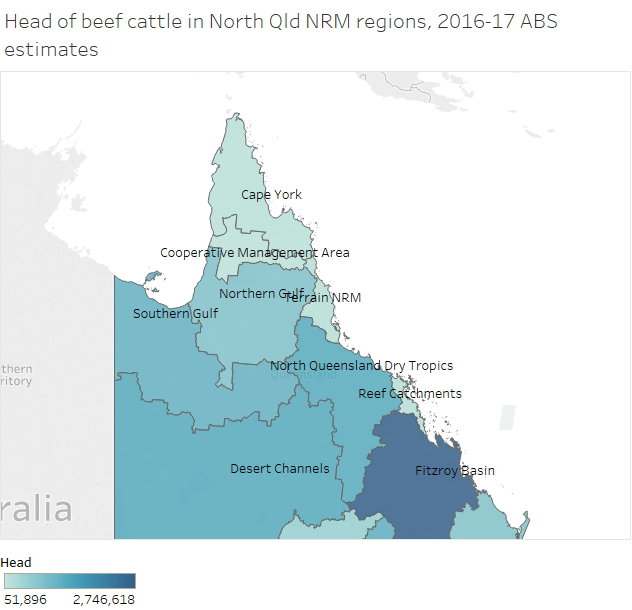

In Queensland, beef cattle numbers are typically around 11-12 million, averaging 11.5 million over 1999-00 to 2016-17. A loss of 500,000 cattle would represent a 4-5% loss of the stock of beef cattle in the state. Of course, the economic impact in the affected regions would proportionately be much higher, particularly if you take into account backward and forward supply-chain linkages (e.g. backward to farm supplies and forward to abattoirs). In the Northern and Southern Gulf regions and the NQ Dry Tropics regions which appear worst affected, there were an estimated 3.2 million head of cattle in 2016-17, so at least one-in-six head of cattle in these regions may have perished based on an assumed loss of at least 500,000 head (see chart below and the map at the bottom of the post so you can see where the Natural Resource Management regions are).

What could this mean for the state economy as a whole? Consider that the Queensland Government’s handy AgTrends publication forecasts a gross value of production of cattle and calves of just over $5 billion in 2018-19. Additionally, it forecasts value added from meat processing at $2.3 billion, the vast bulk of which (at least 80% I would assume) would relate to beef. For simplicity, let’s scale that up by 50% to allow for value added in the transport, wholesale and retail sectors, and let’s say the floods result in a 5-10% loss in activity over 2019. My back-of-the-envelope calculation is that the economic impact of the loss of cattle related to the floods will be around $500 million to $1 billion this calendar year. Queensland gross state product (GSP) in 2019 will be in the $370-380 billion range I expect, so the loss of cattle could shave 0.1 to 0.3% off GSP depending on just how bad the losses are. And given the loss of calves, part of this impact will persist into 2020.

Of course, these are just the losses related to beef cattle. It is expected there will also be losses in the resources, manufacturing and other sectors. For example, Incitec Pivot, which manufactures chemicals and fertilisers, has already announced a hit to earnings from the closure of the rail line between Townsville and its Phosphate Hill source of supply (see this SMH report and SBS report). Such losses will be an additional drag on economic growth. I expect these negative impacts will, in the short-term, only partly be offset by repair and reconstruction activities.

That said, repair and reconstruction activities are expected to be substantial. I’ve just seen an estimate of $606 million of damages associated with the Townsville floods reported by the Courier-Mail. The related repair and reconstruction expenditures will occur over a few years as suggested in the article.

Queensland Treasury is currently forecasting economic growth in 2018-19 at 3%. Given these floods and all the discouraging economic data we’ve seen lately, I expect Treasury would revise this forecast down, to either 2.75 or 2.5%. Given the adverse economic impacts, as well as the costs of repairing infrastructure, the Queensland Government’s fiscal deficit in 2018-19 will probably increase from the $2.6 billion currently forecast by the Treasury.

Update: Since I published this post I have noticed an estimate from AgForce of a $500 million loss of livestock associated with the floods, as reported in the Brisbane Times:

Qld floods damage bill estimates top $1 billion

In a future post I will explain how we need to be careful when discussing economic loss and economic impact estimates, as they are not necessarily comparable. A good explanation in the context of US Hurricane Harvey can be found here:

How natural disasters affect US GDP

This Brookings post by eminent US economist Martin N Baily is also useful:

Very good summary Gene. It’ll be interesting to see what happens to shelf beef prices over the coming months, or even year or two.

Yes, it will be. We could certainly see double digit price increases if the adverse supply impact is 10% or more. Thanks for the comment Stephen.

Gene I don’t think we will see too much of a change in shelf beef prices in Australia due to the floods. More and more the northern cattle are mostly live export these days through Townsville or Darwin ports as they adapt well to the Asian conditions, so numbers will reduce to these markets. The largest processing plant in the north is JBS in Townsville which is predominantly export ground beef, or boxed beef as it is sometimes called, so again the drop in available cattle will probably effect this market more than local supply. If you walk into 90% of butchers in Townsville for example the beef actually comes from processors down south, predominantly the Darling Downs and Northern NSW.

So supermarket prices will more reflect conditions elsewhere? I suspect there may be milk producers asking why their supermarket prices have been attributed to global milk factors while beef prices are not. Not a statement. Just a question.

Note: The AA Co supply chain feeds both ways and to the south through the Comet feedlot.

Glen, thanks for the useful info. Great comment.

Note: the milk comment above was related to memory which I now think was ex ACCC Stephen King subsequently at Monash and why milk prices are related to global prices with Victoria as the lowest cost producer. Now deleted? I mentioned AACo as the largest Australian landholder and beef producer. Mostly export but also through southern feedlots at Comet and Dalby. Academic question: Why are beef and milk prices so different at the supermarket?

Only a month ago from excellent ABC Rural reporter Tom Major in Townsville:

https://www.abc.net.au/news/rural/2019-01-10/townsville-live-cattle-exports-boom-in-first-half/10692860

“Meat and Livestock Australia’s Mick Kingham, from Charters Towers, said live export had been critical to maintaining values as pastoralists run out of feed options.

“Certainly, live export is underpinning the feeder weight market, it’s certainly helping to keep slaughter weight cattle prices quite high,” he said.

“Some cattle are lacking weight to sort of even make feedlot weight, there’s been a large exodus of cattle onto live export [ships].”

Mr Kingham said the wet season had so far failed to bring rains to most of northern Australia, with minimal demand from those re-stocking.”

Look I do know I am being a bore but. I can’t forget my time in Emerald and a grazier complaining to me that rain hadn’t helped because the cattle were just snipping the tops off the grass. Yes its true!

Thanks Mark for all the useful info and comments. I want to look into these issues further and will try to do so when I get the chance.

Insightful, useful and timely information. Well done, Gene 👏

Thanks Simon. It’s still early days in estimating the impacts and hopefully we’ll get a lot more clarity in the next few weeks.

Still waiting for Propertyology to correct a previous mistake on vacancy rates in Cairns. Despite being pointed out it was not corrected in the published agenda?

It’s been a curious climate situation for us up here with a heavy early wet season. AA Co update that four or their properties are either extremely of materially impacted while the rest in NT or elsewhere in Qld are rain deficient. Darwin has had a poor wet season so far while Fairbairn Dam near Emerald is below 15%. It certainly isn’t the 2011 La Nina which is also what the BOM have said and have also released a special climate statement: http://www.bom.gov.au/climate/current/statements/scs69.pdf

I’m no expert on supermarket beef prices except for a keen eye on specials but my understanding was that it can sometimes be counterintuitive. Rain = restocking and reduced supply; drought = destocking and increased supply. Then again I can’t see anything in ant activity at my place which would indicate a serious wet season so apparently the ants are confused too.

Thanks for the info and the comments Mark.