The construction industry is very important to the Queensland economy, and it employs nearly 10 percent of all workers (see Queensland Treasury’s Employment by Industry brief). One part of the broader industry, residential construction, has grown strongly in recent years, owing in part to the huge amount of apartment construction activity in Brisbane. But activity in residential construction has always been expected to fall back as projects were completed, and indeed it has been doing so. Private dwelling construction in Queensland in December quarter 2017 was 5.8% lower than in December quarter 2016. In contrast, non-residential construction activity is recovering nicely from its post-mining-investment-boom slump, with private non-residential construction increasing 11.6% over the same period. Growth in non-residential construction has therefore offset the adverse impact of the recent slowdown in dwelling construction on the state economy.

But what does the future hold? To gain some insight, we can examine building approvals data, the latest batch of which (updated with February data) were released last Wednesday by the ABS. Broadly speaking, as discussed below, the outlook is positive, based on recent approvals data and expected public sector capital works (e.g. Cross River Rail) and resources sector developments, possibly including the Adani mega mine (see this recent AFR article), although many observers remain doubtful it will ever proceed.

Non-residential construction

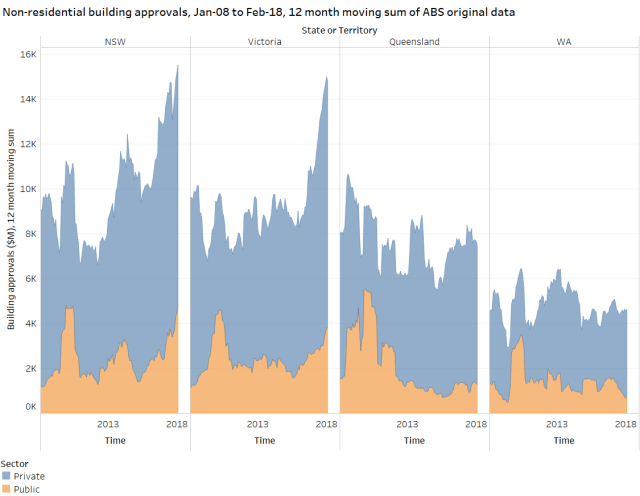

Non-residential building approvals have been at higher levels over the last couple of years after recovering from the trough in 2014-15 (chart below). This gives us reason to be confident about non-residential construction activity, although Queensland has not experienced the massive surge in non-residential approvals seen in NSW and Victoria.

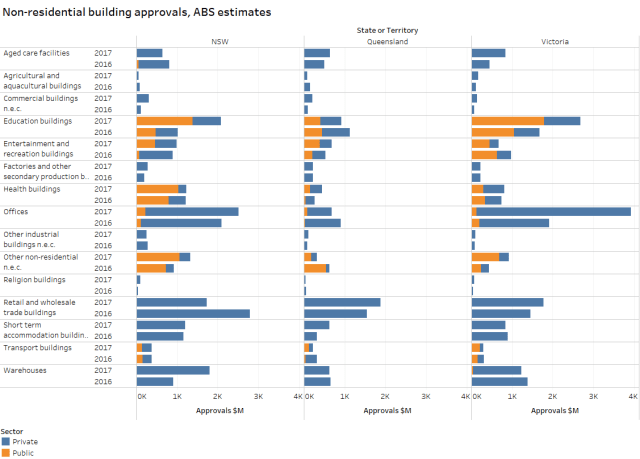

A closer look at the non-residential building approvals data reveals a large part of the recent surge in NSW and Victoria was associated with buildings for education in the public sector. Also, Victoria has seen a doubling in the value of approvals for office buildings. Regarding Queensland, what struck me about the data is that we are disproportionately intending to invest in new retail and wholesale trade buildings, which strikes me as odd given recent trends in the sector.

Incidentally, Master Builders Queensland has a good summary of the outlook for non-residential construction in its 2018 Building Industry Outlook (p. 7):

2018 will see improvement in the demand for non-residential construction work with increased investment in a number of key industries that have been performing well.

The tourism industry will continue to perform well, requiring further investment in hotels and other short-term accommodation…Retail and wholesale trade buildings which is the largest source of demand for non-residential work, has already seen an increase in building approvals which bodes well for the coming year.

The office market will continue to work through an excess of supply and the industrial segment will see no growth.

Note that the non-residential approval figures I refer to above do not encompass engineering construction activity, such as that associated with roads, bridges, rail lines, and earthworks. But we can be confident regarding engineering construction activity due to increasing state government capital works spending (expected to increase from $7.9 billion in 2017-18 to $9.8 billion in 2018-19 according to the 2017-18 MYFER) and positive developments in the resources sector.

The Queensland Resources Council (QRC) provided me with a brief update on its sector earlier this week. Key points included:

- According to IHS, Thursday’s coking coal price was USD 197.95—one year ago the price was USD 155.25

- Four new coal mining leases were recently granted to Stanmore Coal securing 210 jobs

- The Palaszczuk Government has awarded two preferred exploration tenders to two junior exploration companies, Metroof Minerals and Sojitz Coal; Metroof was awarded 86 square kilometres while Sojitz Coal received 45 square kilometres; both areas are within 60km south-east of Middlemount

- Queensland based coking coal company Vitrinite, owners of several assets in the Bowen Basin, has signed an agreement with Japanese trading company Itochu Corporation to fast-track development of the coking coal Karin deposit

Developments such as these reinforce my confidence in the sector.

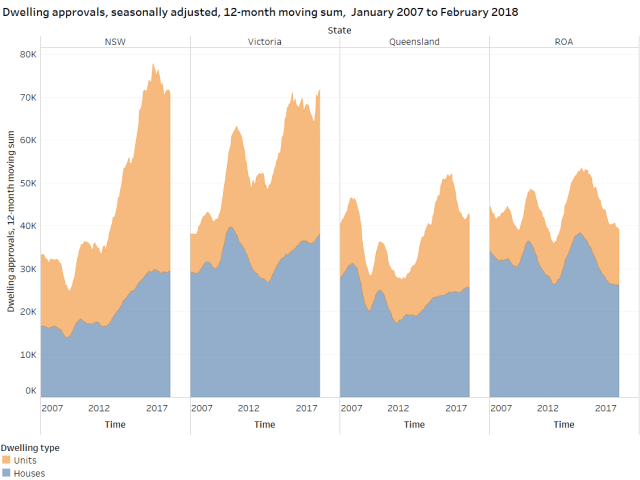

Residential construction

Regarding residential construction, Queensland’s new home approvals are on an upward trend (see chart below) and this will offset to some extent the decline in apartment construction. This was foreshadowed by Queensland Treasury last December in its 2017-18 Mid Year Fiscal and Economic Review (p. 8):

With the value of work in the pipeline now easing, it is expected that dwelling investment will fall in 2017-18 and 2018-19. However, a recent pick-up in approvals for houses, combined with a strengthening in population growth, suggests the decline in dwelling investment will likely be modest when compared with previous housing cycles.

Overall, Queensland residential building approvals appear to be at reasonable levels, while they have soared in NSW and Victoria.