Pauline Hanson’s opinion piece in yesterday’s Australian arguing against the Turnbull Government’s planned company tax cut (and in favour of state government payroll tax cuts instead) may well mean the end for the Turnbull Government’s planned cut. Hanson’s article highlights the impact of dividend imputation, which is designed to avoid the double taxation of corporate income (i.e. taxing company profits and then taxing dividends to shareholders) which occurs in many countries such as the US. As Nicholas Gruen explained in an insightful 2006 CEDA paper Tax Cuts to Compete (p. 17):

Because imputation means that company tax operates as a withholding tax against Australian shareholders’ personal tax liabilities, company tax itself has little distributional significance.

That is, dividend imputation means that the benefit of a company tax cut would be offset to a large extent for domestic shareholders. Dividends may increase, but shareholders would receive fewer franking credits (relative to what they would have at a higher company tax rate) to reduce their personal tax liability. Foreign investors didn’t receive any benefit from Australian franking credits in their own jurisdictions anyway, so logically foreign investors would receive most of the immediate benefit of any company income tax cut. That said, domestic investors receive some short-term benefit due to improved company valuations (as the company tax cut allows greater retained earnings) and the fact capital gains are taxed at a concessional rate.

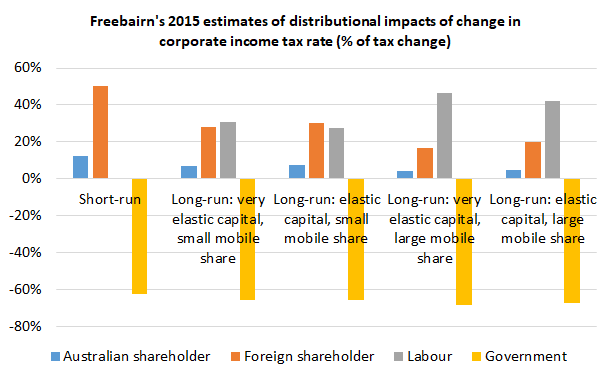

In the long-run, domestic and foreign investors as well as workers are expected to benefit from a company tax cut, as a lower cost of capital associated with a lower company tax rate leads to an increase in capital investment and higher labour productivity. This may take several years, possibly up to a decade, to have a noticeable impact. The best and most convincing analysis I have seen regarding the potential impacts of a company income tax cut was written by University of Melbourne Economics Professor John Freebairn and published in the Australian Economic Review in 2015: Who pays the Australian Corporate Income Tax? Freebairn’s analysis should be compulsory reading for anyone wishing to comment in the company tax debate. Regarding a company income tax cut, Freebairn notes (on p. 357):

In the short run, non-resident investors are large winners at the expense of government revenue. In the long run, some of the short-term benefits to shareholders are eroded, one-half or more of the benefits goes to higher wages and about one-third of the first-round loss of government revenue is recaptured.

Freebairn acknowledges the magnitudes of the benefits of a company income tax cut depend on the extent to which capital is mobile between Australia and other economies, and this is uncertain. So he provided a range of estimates based on various assumptions about capital mobility which all tend to show large shares of the benefits of company tax cuts going to workers, while foreign shareholders receive a greater share of the benefits than domestic shareholders, in the long-run (see figure below). Freebairn’s estimates show that 30-35 percent of the revenue forgone by the company tax cut comes back to government via income tax and other taxes.

The fact that it is expected only a small proportion of the benefits of a company tax cut accrue to domestic investors (and no benefit accrues to labour in the short-run) goes a long way to explaining why the Turnbull Government has found it so difficult to promote its company tax plan. That said, there is little doubt there would be long-run economic benefits from a company tax cut, provided the Government can keep its budget under control and rein in public debt. Of course, I acknowledge a company income tax cut would make this more difficult, particularly given the “starve the beast” hypothesis (i.e. tax cuts compel later spending cuts) doesn’t have much empirical support. From a budget management perspective, the proposed company tax cut is concerning, so the Turnbull Government needs to be very confident it will provide the large economic benefits it is expecting.

While the exact magnitudes of the impacts of the company tax cut would be uncertain, I don’t think the fact that positive economic impacts exist should be controversial. The ABC’s Emma Alberici was rightly criticised for her recent opinion piece, which didn’t fairly reflect the large amount of high quality analysis by the federal Treasury, Chris Murphy and other economists that has already be done on the impacts of a company tax cut.

For example, see Chris Murphy’s study The effects on consumer welfare of a corporate tax cut in which Murphy estimates long-run gains to GDP of 0.7-0.9 percent and in the real wage of up to 1 percent. And consider that Murphy’s modelling doesn’t take into account the impact of the Trump tax cut, which is undeniably another reason Australia should consider cutting company tax. Incidentally, Murphy (on p. 23) effectively counters the finding made in a Victoria University study that a company tax cut could decrease gross national income (even though it boosts GDP) by noting some of its model parameters appear odd and it did not correctly model the impact of dividend imputation.

Based on the analysis by Murphy, Freebairn and others, I disagree with Professor Fabrizio Carmignani from Griffith University, who has recently written a Conversation piece titled There isn’t solid research or theory to support cutting corporate taxes to boost wages. Unfortunately, Fabrizio has ignored the economic modelling of a company income tax cut conducted by leading economists such as Chris Murphy and John Freebairn.

Finally, I should acknowledge that, in the CEDA paper by Nicholas Gruen I referred to above, Nicholas argued in favour of abolishing dividend imputation entirely and cutting the company tax rate to below 20 percent. This would certainly lower the cost of capital and boost investment much more than the Turnbull Government’s proposed cut, but I have reservations about it. It would introduce a bias in favour of debt finance, as Nicholas acknowledges in his paper (p. 23), and it would imply an increase in the taxation of dividends paid to many Australian shareholders. Nonetheless, given the apparent failure of the Government’s current plan to cut company tax, Nicholas’s plan is certainly one that should be assessed among alternative options.

Gene

Tax policy is way above my pay grade, but has anyone looked at the option of a cut in payroll tax vs. a cut in income tax and how it stack up. If investment decisions are influenced by the whole tax burden (as they supposedly are), surely policy makers should be looking at all of the possible ways to reduce the tax burden (even if the Commonwealth had to compensate the States).

Perhaps an equivalent reduction in payroll tax could be more beneficial as it: a) boosts employment / wages (the relative price of labour vs capital changes); b) removes distortions in the labour market due to the payroll tax (different thresholds and rates depending on business size and location), and c) doesn’t have some of the same problems as a reduction to the company tax.

I’ll leave this to bigger brains than me to sort out as I simply don’t know. But I think Pauline Hanson’s alternative deserves a look. I cannot believe I just said that….

Thanks for the comment Jim. I agree Hanson’s alternative deserves consideration. Regarding your question, I think KPMG’s excess burden estimates for different taxes for the Henry tax review are relevant:

The estimates suggest payroll tax has a slightly higher excess burden than company tax, so it appear cutting payroll tax might be a reasonable alternative to cutting company tax (although then there is the problem you alluded to regarding the fact payroll tax is a state tax).

Thanks. Glad you are on top of these things.

Gene this going to play out to be a major issue for corporate Australia over the next few years, Given the size of the US economy many companies in years to come will have more earnings in the US than Australia, Boral, Hardies, Bluescope are just a few examples where an expanding US presence will result in many companies either looking to incorporate in the US or at the very minimum declare earnings and pay tax in the US if there is a considerable tax advantage to do so, either way Australia will miss out on the investment, taxes paid and associated employment. Secondly companies from the US selling into Australia will have a cost advantage over Australian companies operating under a higher tax regime here. Whilst there won’t be instant ramifications for Australia not lowering its corporates tax rates the effects over a longer period will be very damaging to our economy and leave many of our corporates with very difficult decisions to make which won’t be popular with the public.

I agree. Excellent comments. Many thanks Glen.