I am delighted to publish a guest post by my old friend and former Treasury colleague Joe Branigan on the recent upgrade to the outlook for Queensland’s credit rating from Moody’s. GT

Moody Blues

by Joe Branigan

Moody’s Investor Services has upgraded the outlook for Queensland’s public finances from negative to stable. This is undoubtedly welcome news for the Queensland Government and its liability manager the Queensland Treasury Corporation. And there’s nothing like a boost of confidence for Queensland in this somewhat miserable post mining boom decade.

However, in my view we need to keep the champagne chilled in the QTC boardroom fridge for a little while longer. The problem with Moody’s analysis is that it focuses too much on the short-term boost to revenue from the recent (and welcome) increase in coking coal prices as well as the initial boost to growth from LNG exports. Moody’s implicitly assumes that both of these factors will continue indefinitely. In fact, neither factor in isolation has much to do with Queensland’s long-term structural budget position, especially because of the way the Commonwealth Grants Commission discounts Queensland’s GST allocation every time the rivers of royalty revenue flow a little too fast for the CGC’s liking.

When you look through the fluctuating resource prices and one-off budget measures, such as the superannuation payment holiday and loading the Government Owned Corporations (GOCs) with debt, it is clear that Queensland has a structural budget problem that can only be addressed by consistently restraining spending growth in the general government sector to below long-run average revenue growth, not just next year but for the next generation.

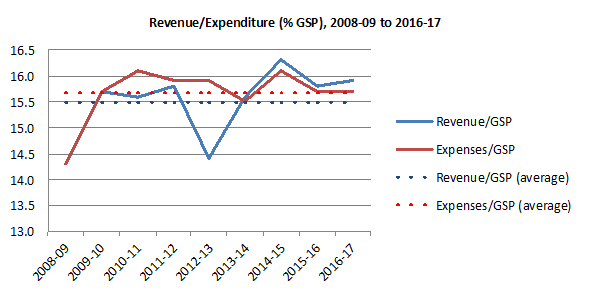

The latest Queensland Treasury forecasts from the 2016-17 Mid Year Fiscal and Economic Review (released December 2016) show net debt in the General Government sector rising from $2 billion in 2016-17 to $9 billion in 2019-20. That is, the Government’s financial position continues to deteriorate. MYFER also assumes that the Queensland Government will manage to keep expenses growth to 2.1% per annum for the rest of this decade. Remember that this 2.1% needs to not only account for wages growth but also the growth in the number of public servants. In my view, this is an impossible expenditure growth trajectory.

And the fact that Queensland Treasury forecasts a fiscal deficit for the rest of this decade means that the government must continue to rely on ‘balance sheet management’ to reduce debt in the General Government sector. As I’ve said before the problem with these one-off accounting gymnastics is that they’re one-off. There’s only so much blood that can be drawn out of a GOC before its concrete and steel skeleton curls up and rusts away.

Moody’s also falls into the trap of comparing the current budget with the ‘worst of the worst’ years when Queensland lost its AAA rating in 2009 rather than evaluate Queensland’s public finances against best practice. It says:

“The affirmation of the Aa1 ratings reflects Queensland’s financial performance, which, although it is still registering deficits (on a net lending/borrowing basis), has shown improvements in recent years, following a period of large and consecutive budget gaps.”

Okay, we are doing much better than in the late 2000’s – good on us.

Moody’s analysts should focus on the capacity of the Queensland economy to reduce its public debt and deficit levels over time based on the long-run performance of the Queensland economy and long-run average growth in public expenditure and revenue. In other words, Moody’s should ask whether Queensland’s level of debt is sustainable at 3-3.5% economic growth, 3-4% expenditure growth, and wildly unpredictable revenue growth that has ranged between -8.8 per cent in 2012-13 and +18.0% in 2008-09?

This is not to say that Queensland is anywhere near risking default. Of course it isn’t because the state has a large pool of assets that it could tap into in an economic emergency. More generally, the Queensland Government always retains the coercive power of taxation over its law-abiding (and taxpaying) citizens, and (worst case) the Australian taxpayer will always stand behind the Queensland taxpayer.

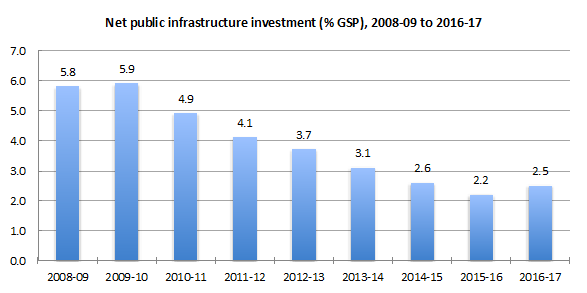

However, poor public financial management – letting our balance sheet slowly slip away – does affect long-run growth prospects. Higher debt and higher interest payments mean less money for future infrastructure investment, especially if the existing debt has proven unproductive (a point made in recent years by Professor Tony Makin and Professor Henry Ergas to name just two). And, to the extent that the debt is unproductive, an unfair burden is placed on the next generation.

In my view, the Queensland Government should focus on expanding the capacity of the Queensland economy. Invest in infrastructure that supports productivity and growth, and invest in people – especially the young and low skilled – to help them into a labour market hampered by the highest minimum wage in the OECD.

In other words, rather than trying to stimulate demand in particular industries that might be struggling, focus on stimulating the supply of productive infrastructure and productive workers.

Sounds easy, but it’s not. The challenge of course is knowing what infrastructure will be productive and which incentives will work to get the young and unskilled into work at the lowest cost to the taxpayer.

With public infrastructure, a rigorous and sober process of cost benefit appraisal helps to prioritise the best projects and make it that much harder for politicians to go with their pet projects if they don’t stack up. Transparency is also important – releasing full cost benefit appraisals and business cases is essential to good investment decisions, not just the summaries that are impossible to critique let alone replicate.

Unfortunately, the way our Federation works means that big bang mega-projects are often prioritised over smaller, more incremental, projects that may have better payoffs in terms of supporting productivity and growth – but that’s a post for another day.

Joe Branigan is a Brisbane-based Associate with Cadence Economics and a Senior Research Fellow at the SMART Infrastructure Facility UOW. His daughter Valentina recently started Day Care and, as a result, Joe is tentatively stepping back into the ‘blogging scene’.

Hi Gene and Joe

I am really glad you posted this. I thought the Moody’s statement was quite counterintuitive. Firstly it states …….

“Similarly in FY2016/17, the state forecasts a deficit equal to 1.8% of revenues, down from the 3.8% budgeted, and it may even move into a surplus due to the recent surge in coal prices, as related to the disruptions caused by Cyclone Debbie in late March 2017.”

This does not follow as the spike in coal prices caused from the Aurizon rail corridors being out of action also denies its export and in turn royalty revenue to the State Government.

Secondly the section articulating the change in outlook to stable from negative is almost the case for why is should stay negative in my view ……

“The stable outlook reflects Moody’s view that Queensland’s fiscal position over the medium term, either through slim deficits or modest surpluses, will not have a material impact on the state’s debt burden nor interest expenses. Both the debt burden and interest expenses will remain elevated compared to higher rated peers over the rating horizon.

Moody’s further notes that recent debt reduction is due to a re-structuring of the state’s balance sheet, including the taking of a superannuation holiday, the drawing down of funds set aside for employee liabilities, and the transference of debt to public corporations, which are all essentially one-time measures that do not address structural imbalances in the budget. “

Welcome your thoughts, but I thought it was a bit perplexing.

Cheers

Nick

Thanks for the comment Nick. Yes the Moody’s logic is a bit confusing but it’s a good thing they’ve taken off the negative outlook.

Nick – exactly. I thought the same on your second point. On your first point, you show that Moody’s analysis is just bizarre – are they really changing their outlook based on 3 months (April-June) of higher royalty revenue in a single year (2016-17) from an event that happens every decade or two?? Moody’s is effectively forecasting a cyclone in March each year to spike coal prices to achieve a surplus…has Moody’s informed BOM??

Cheers

Joe