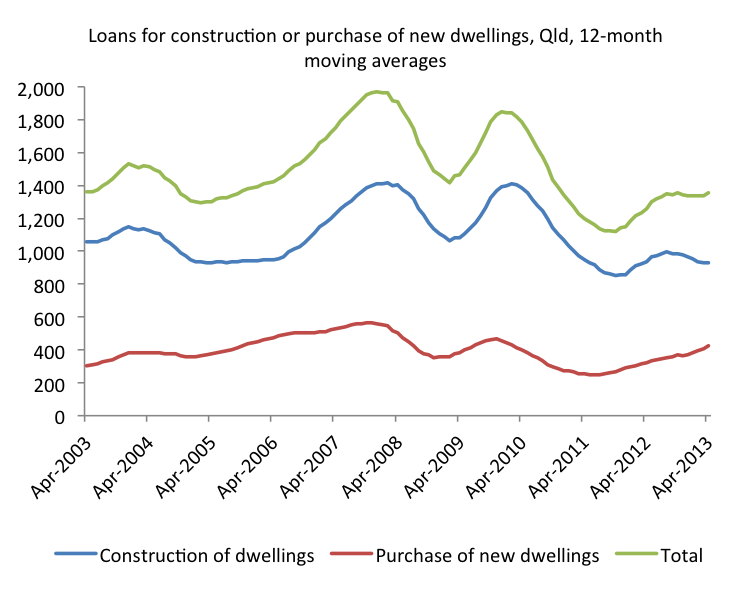

The Housing Industry Association (HIA) gave an apt summary of today’s ABS housing finance data in the title of its media release Home lending up but not by enough. The Queensland data (see my chart below) are consistent with building approvals data (see this previous post) that suggest a very slow recovery for our building industry.

It is interesting that the proportion of new loans for the purchase of new dwellings, as distinct from the construction of dwellings, is increasing. Could this be because costs imposed by regulations (e.g. around environmental sustainability or heritage protection) are making building new houses in established areas even more unaffordable, leaving many people little choice but to buy more affordable houses in new estates on the urban fringe? The HIA certainly thinks regulation, along with taxation (stamp duty, I assume), is constraining housing construction. The media release notes:

It is interesting that the proportion of new loans for the purchase of new dwellings, as distinct from the construction of dwellings, is increasing. Could this be because costs imposed by regulations (e.g. around environmental sustainability or heritage protection) are making building new houses in established areas even more unaffordable, leaving many people little choice but to buy more affordable houses in new estates on the urban fringe? The HIA certainly thinks regulation, along with taxation (stamp duty, I assume), is constraining housing construction. The media release notes:

“…residential investment in construction continues to languish near decade lows, a pointer to the disincentive to new home building attributable to excessive tax and regulatory costs,” warned HIA Senior Economist, Shane Garrett.

Given the very slow recovery in housing construction, our Councils and Governments need to have a serious look at the impact of their regulations and taxes on the sector.

On today’s housing finance data, KS at Loose Change notes there have been some widely varying interpretations:

How to interpret housing finance data?

As usual, MacroBusiness has good coverage of the data:

New home finance confirms ongoing tepid recovery

You note that It is interesting that the proportion of new loans for the purchase of new dwellings, as distinct from the construction of dwellings, is increasing. I think this is explained by the effect of the First Home Owners grant only being available for new dwellings. First Home Owners are now more likely to buy an affordable inner city new unit which qualifies for the FHOS, rather than build a similar cost house in an outer suburb, or an exist dwelling that does not attract FHOS. Developers are now very good at designing, building and marketing new inner city apartments with the $10k FHOS as the deposit. Even for investors, new apartments are far less maintenance, and more transferable than houses. Increasing sales of new apartments – hence the increase in loans for new dwellings.

Yes, I suspect you’re right, Katrina. Thanks. I should have thought of that.

In addition, the market is currently being driven heavily by investors who have historically demonstrated a strong preference to purchase existing houses rather than build.

Yes, good point. Thanks.