The Australian Government is moving in the right direction, but not fast enough, with fiscal policy if it wants to fight inflation. It appears too reliant on the expected cessation of pandemic-related stimulated measures to support its claim that the Budget is contractionary. And arguably it should be running a bigger surplus in 2022-23 and a surplus rather than a deficit in 2023-24, if it wants to make a substantial contribution to the fight against inflation. This is clear from Treasury estimates presented in the 2023-24 Budget, as explained in this article.

In defending his Budget, Treasurer Jim Chalmers observed “Our budget is contractionary when inflation is at its highest”, as quoted in The Australian. Is it true the Budget is contractionary? Critics have argued the federal government isn’t being fiscally responsible because spending is increasing. This is true, but the size of the economy and government revenue are also increasing. What matters is how spending and revenue changes compare with what they would be in a fiscally-neutral scenario. How should we judge the government’s fiscal impact or impulse with respect to the economy, or whether its aggregate spending and revenue choices make sense given the state of the economy?

According to IMF economists Garry Schinasi and Mark Lutz in the 1991 Working Paper Fiscal Impulse:

“The IMF measure of the fiscal impulse is the change in the fiscal stance, which is an estimate of the initial amount of expansionary or contractionary pressures placed by the budget on aggregate demand. This measure of fiscal impulse attempts to remove changes in the actual budget balance that are transitory in a cyclical sense.”

The fiscal stance can be considered as an estimate of what the budget balance would be if cyclical influences (i.e. the state of the economy relative to its trend) were removed. The fiscal impulse is the change in the fiscal stance, and it tells us whether the government budget will add more or less to aggregate demand in one budget year than in a previous year.

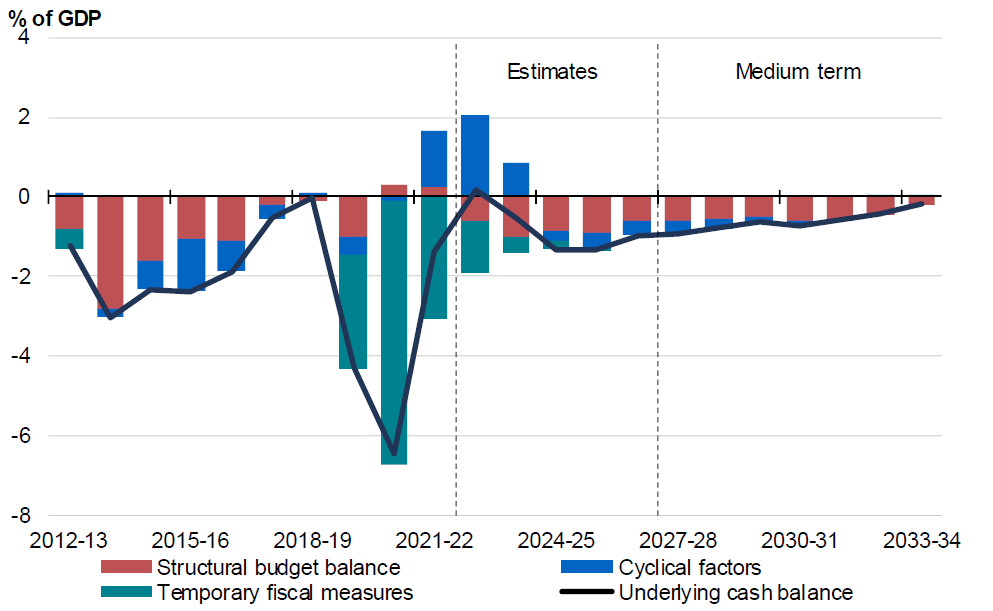

There is no perfect way of estimating the fiscal stance, and hence the fiscal stimulus, but various organisations such as the IMF and Treasury have tried doing so. While the Treasury doesn’t explicitly indicate the fiscal impulse of the budget, it does provide measures that help us determine whether the Government Budget can be considered expansionary or contractionary. The Treasury gives us an indication of the fiscal stance of the Government in the Fiscal Strategy and Budget Outlook chapter of Budget Paper 1, with the important chart reproduced below (Figure 1).

Figure 1. Structural budget balance estimates presented in 2023-24 Australian Government Budget

First, consider the evolution of the budget balance between 2022-23 and 2023-24, the budget year for the Budget handed down by Treasurer Jim Chalmers on 9 May. To gauge the fiscal impulse, we need to compare the deterioration in the budget balance, labelled underlying cash balance (UCB), the black line, with the reduction in the positive contribution of cyclical factors, the blue columns. The Budget forecasts the UCB deteriorates 0.7 percentage points, from 0.2% of GDP in 2022-23 to -0.5% of GDP in 2023-24. Eyeballing the chart above, however, we see that cyclical factors (i.e. higher commodity prices, stronger-than-usual economy) make a much smaller positive contribution to the UCB in 2023-24 than in 2022-23, falling from around 2% of GDP to what looks like around 0.7-0.8% of GDP. The reduction in positive cyclical influences appears greater than 1% of GDP.

This means that we could say that, in 2023-24, the government is expected to reduce the impact of its Budget on the macroeconomy. You could say it is tightening the fiscal stance. Given what is happening with cyclical factors (i.e. a slowing economy), the UCB should deteriorate by more than it is actually expected to deteriorate. It does not deteriorate by over one percentage point (i.e. the reduction in the positive boost from cyclical factors) because, at the same time, over 2023-24, temporary fiscal measures are being reduced (i.e. the shrinking green columns). Of course, that was always going to happen so the Government probably doesn’t deserve much if any credit for that.

The structural budget balance, an indication of the state of the budget in normal times, is forecast to deteriorate slightly in 2023-24. This is consistent with the Government’s policy decisions since the Budget in October which will worsen the UCB by $12 billion in 2023-24, with an additional $13.8 billion in payments offset by only an additional $1.8 billion of receipts induced by new policy measures (see Table 3.2 in Budget Paper 1). In its discretionary measures, the Government is not undertaking contractionary fiscal policy it appears.

On my calculations, the fiscal impulse of the Budget in 2023-24 is estimated to be around -½ percentage point of GDP. This is the difference between the change in the contribution of cyclical factors to the Budget (around -1¼ percentage points) and the change in the UCB (-0.7 percentage points). Incidentally, using the same logic, we could estimate a fiscal impulse of around -1¼ percentage points in 2022-23 as temporary fiscal measures associated with the pandemic were withdrawn. Again, the Government probably doesn’t deserve much credit for that.

The blue columns in Figure 1 from Treasury tell us what the UCB would be if there was no structural budget deficit and if there were no temporary fiscal measures (i.e. stimulus measures, most recently during the pandemic). This could be considered as an estimate of a neutral budget balance. It tells us that the UCB could have been 2% of GDP in 2022-23 and around 0.7% of GDP (based on eyeballing Figure 1) in 2023-24, if there was no structural budget deficit and if there were no temporary fiscal measures.

Certaintly, temporary fiscal measures now seem rather inappropriate given the COVID-recession is well behind us. Arguably, given the strong recovery post-COVID and high commodity prices, the Government could have done more to tighten the Budget so it wasn’t adding as much to aggregate demand and very likely contributing to the higher-than-usual inflation we’ve been experiencing. From a macroeconomic perspective, it would likely be desirable for the federal government to run a larger surplus in 2022-23 and a surplus rather than a deficit in 2023-24 to reduce aggregate demand and put downward pressure on inflation.

Please feel free to comment below. Alternatively, you can email comments, questions, suggestions, or hot tips to contact@queenslandeconomywatch.com. Also please check out my Economics Explored podcast, which has a new episode each week.