Guest post by Dr Andreas Chai, Economic Policy and Analysis Program, Griffith University

1999 was a great year to be alive in Australia. Apart from Prince hitting the airwaves again, Powderfinger were still playing and topped the hottest 100, the first Matrix movie was released and you could still get a flat white for under three dollars. In terms of the Federal budget, 1999 marked the start of a remarkable period in which the Federal budget accumulated approximately $90 billion dollars between 1999-2008.

2018 is starting to look a lot like 1999, at least in terms of international commodity prices. While global growth remains sluggish and domestic business investment is stuck in a low gear, the underlying cash balance of the Federal government is projected to reach surplus in the coming quarters thanks to the strong performance in commodity prices, such as an iron ore.

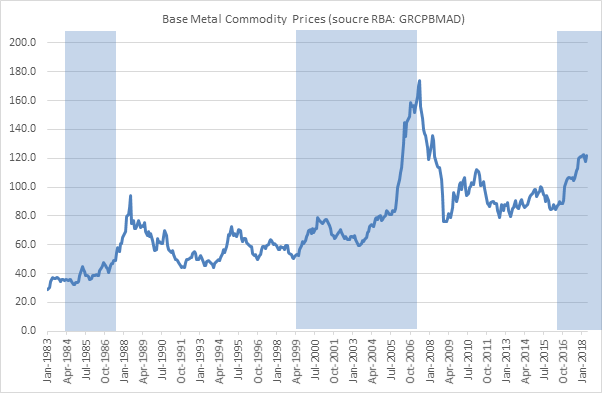

Rising iron ore prices drive up earnings in the resource sector and therefore tax revenues. The chart below highlights the link between commodity prices and the Federal budget. The shaded area highlight phases in which there was significant returns to surplus in 1985-1987, 1999-2007 and 2016 to present.

These phases of fiscal recovery coincided with a significant upward jump in the commodity prices. The only period where the fiscal position improved in the absence of rising commodity prices was immediately after the 1991-92 recession.

While a recovering fiscal position is warmly welcomed by politicians, especially with a federal election just around the corner, it is worth reflecting on the fact that much of these new spending opportunities are not due to sound economic management but are rather due to global market forces that are extremely volatile in nature and hard to predict. It is much too tempting for Governments to view these upward movements as permanent. Any new spending initiatives are thus likely to be built on shaky foundations. New spending initiatives should be tagged with the big asterisks flagging “funding initiatives will only last as long as global commodity prices keep surging.”

A much deeper issue is how the Australian economy can evolve to grow in a more balanced manner and reduce its exposure to falling commodity prices. This fundamental question has bedeviled Australian politicians for centuries since the Gold rushes in the 1800s. Having recently emerged from a commodities super-cycle between 2004 and 2013 (see figure above), it’s funny how some of the lessons from the last commodities boom have already been forgotten. In 2013, there was much agreement that Australia had squandered the mining boom mainly due to having spent the windfalls during the boom, raising inflation and debt levels.

A more strategic approach would consist of getting a national response to rising commodity prices right by setting up Sovereign Wealth Funds that can translate short terms gains into long term investments in health (e.g. NDIS), education and infrastructure that will help hedge Australia’s economy against future downturns in commodity prices. A good start was made in this direction as some of the mining boom surplus from the last super-cycle was put into investment funds (e.g. the Future Fund, Education Investment Fund). However, we are still far behind other countries such as Norway, Singapore and the UAE in terms of developing a sophisticated long term strategy to leverage future surges in commodity prices (and improvements in the Terms of Trade) to diversify the economy and support long run productivity growth. While the long run return to surplus is good news, it’s time we take heed of the lessons from the recent past.

Dr Andreas Chai is Senior Lecturer in Economics and the Director of the Economic Policy and Analysis Program at Griffith University. Andreas has previously worked at the Productivity Commission (Melbourne) and the Commonwealth Treasury (Canberra). Andreas is an applied microeconomist with expertise in consumer behaviour and demand analysis, skills shortage projections, tourism economics and innovation economics. He has published in the Journal of Economic Perspectives and the Cambridge Journal of Economics.

This post is expected to be cross-posted at Griffith University’s Policy Innovation Hub.

excellent

Thanks Craig. Andreas has made some excellent points in this piece.

Thanks for this Gene,

Needless to say I agree with you.

I didn’t know Singapore’s SWF had a focus on cyclicality (if that’s a word 😉

Though I do know that at least in the past they’ve made ad hoc changes to it which may reflect cyclical issues. You can do that in an authoritarian state (or at least if you’re in one of the few that is well run). We seem to have a lot more trouble with that in democratic states.

Can you tell me more about Singapore?

Hi Nick, glad you enjoyed the article!

Singapore owns two independent SWFs : Temasek Holdings (since the 70s) and GIC (more recent). Total annualised returns for the previous have been reportedly 18%. Although Temasek originally invested domestically, foreign investments now account for more than half of its total portfolio, concentrated in Asia. I think they used to own Optus, not sure if they do now. Note that it got into a bit of hot water during the GFC for being over exposed to subprime mortgages.

Regards

Andreas

The graph is interesting. Are base metal prices a good proxy for Australia where bulk commodities dominate?

Look. It probably wont make any difference and maybe I just expect a higher quality of academic research.

I’ll check with Andreas. I think he is using this as a proxy for the iron ore price which the federal budget is especially sensitive to via its impact on mining profits and hence company tax.