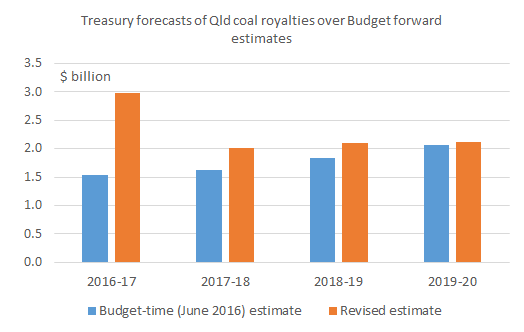

As we have been expecting for some time, higher coal prices and thus royalties (see chart below) have translated into a much improved State Budget balance, with the Queensland Treasury now forecasting the biggest operating surplus ($2 billion) in a decade. The surge in coal royalties is extraordinary, up $1.5 billion over the Budget-time forecast for 2016-17.

The improved operating balance is welcome, but the State Government still has a fiscal deficit of $1 billion (taking into account capital spending), meaning it continues to borrow money and add to State debt, even though we need to reduce State debt if we are to regain our AAA credit rating.

In its editorial today, the Courier-Mail rightly points out the need for rigorous cost-benefit analysis of regional job creation schemes, and the need to restrain the growth of the public service, which has been expanding at a rapid rate under the current Government. The Editor also makes the following point:

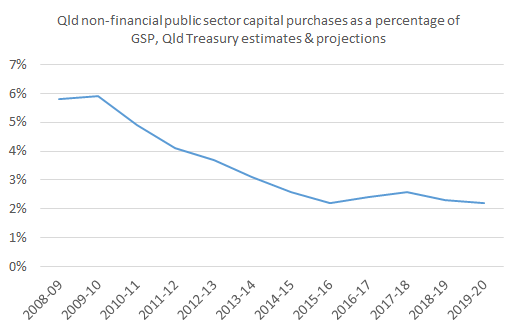

“While the Government likes to make much of its capital works program, the reality is that real spending on capital purchases is declining or (depending on the measure used) at best flatlining at a time when Queensland needs major pieces of investment to underwrite future economic growth.”

The Editor’s point about capital purchases flat-lining is correct (see chart below). As I have noted previously, it was unwise for the Government to rule out privatisations of State assets, which could have allowed it to invest in new assets without increasing debt. I expect the debate about asset recycling to resume in the new year.

The real question about debt is not how much but what it is used for. If the debt is for productive assets then the level shouldn’t be a significant problem.

Thanks Alistair. I agree you can borrow to invest in productive assets, but a lot of Qld’s debt in the past has come from investments in non-productive assets.