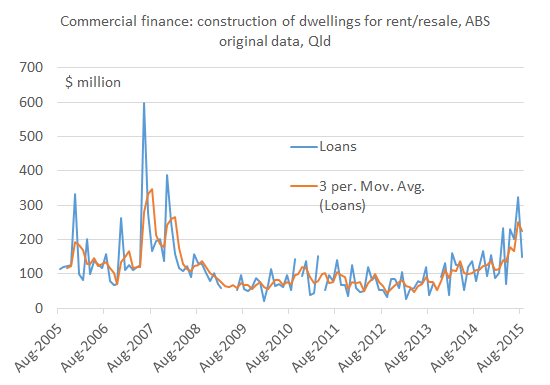

The Queensland Treasurer Curtis Pitt correctly noted yesterday that “The property sector is a real bright spot in the Queensland economy and it’s making a positive contribution to jobs and growth.” This is confirmed by data and casual observation. Regarding the data, for example, the Treasurer pointed to the high level of loans to investors for the construction of new dwellings, at least compared with the last few years (see chart above). Regarding casual observation, wherever you walk in inner city Brisbane you are likely to spot cranes, as I did while walking along the Bicentennial Bikeway on Sunday afternoon (see image below of cranes over West End).

This is all very well and good, but, as I’ve noted previously, there are real concerns about the impact all the new supply will have on the market over the next year or so:

This is all very well and good, but, as I’ve noted previously, there are real concerns about the impact all the new supply will have on the market over the next year or so:

As many units as houses approved in Queensland in last 12 months – is a unit price crash coming?

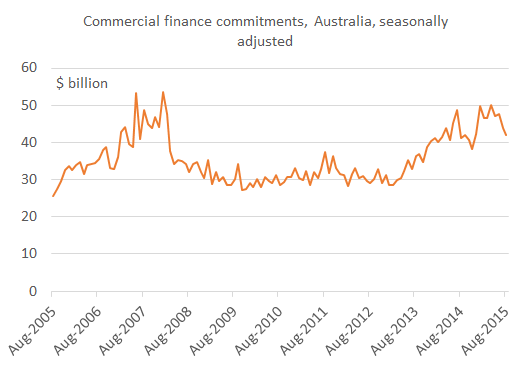

I also remain concerned about the broad economic outlook for the Australian and Queensland economies, particularly given potentially weak levels of business investment over the next twelve months. The drop in commercial finance commitments across Australia reported by the ABS yesterday (see chart below) has reinforced this concern of mine.

Borrowing money to swap non-productive assets with each other – some economic model.

APRA and the RBA should be ashamed of themselves.

Australia needs a recession to cleanse the imbalances. Instead they got another chapter in debt fueled speculation and systemic risk in the banking system.

The bubble has crowded out other business apart from that of the government (which also promotes fantasy wages).

At least QLD is going to look better in five years compared to Sydney and Melbourne – that hangover is going to be a doozy.

The issues raised in the comment above seem to be gaining some prominence Gene – see also the article l link to below. It would be great to have your views on this topic!

http://www.news.com.au/finance/economy/the-high-cost-of-australias-housing-obsession/story-fnu2pwk8-1227457463991

Thanks Toby. I’ll try to cover this in the future. I made some comments about negative gearing in a speech I gave today at the CPA Congress. The highly concessional tax treatment of capital gains has led to a blowout in landlords negative gearing unfortunately. Nothing wrong with allowing negative gearing in principle though.

I agree with some of your sentiments (and with Toby’s). Investing in non-productive assets (i.e. housing) does little for long-term economic growth as it crowds out business investment. Governments should not be subsiding these investments (e.g. via negative gearing) when business investment is not necessarily afforded the same largesse. Of course, no largesse to anyone is the best policy.

But the challenge we face is that it makes perfect sense for the banks to continue to lend more into the housing sector unless there is a significant change to the way the lending market works (I don’t know what).

For a business loan, the risk of payment default and asset values are inextricably linked (the asset value is a function of long-term profitability). This makes for a pretty risky lending market and the two sources of risk are positively correlated).

For the housing lending market, the link between payment risk and asset risk does not really exist. Payment risk is a function of the borrowers employment (relatively low and is often insured as part of the lending requirements). Asset price risk separate from payment risk and is mitigated through minimum deposit requirements and the fact that borrowers are still contractually obliged to repay any outstanding debt after a house is repossessed and sold (this is different to the case in the US which left the banks holding much of the asset value risk leading hop to the GFC).

The bottom line is that the risk to banks from lending for houses is negligible, while the margins are still a lot higher than the risk would suggest. This is a recipe for sustained low-risk profits.

Thanks Jim. Some greats point there.

Thanks for the comment White Elephant. Yes, Qld may well end up looking better than southern states.

From the RBA Financial Stability Review:

“While the housing market remains a long way from oversupply nationwide, some geographic areas appear to be reaching that point, particularly the inner-city areas of Melbourne and Brisbane. Apartment approvals remain at very high levels in these areas, even though these rental markets already look soft; apartment prices have been little changed in the past year, rental vacancy rates are relatively high and growth in rents is subdued”

Thanks Mark. Yes, the amount of new supply and prospective supply is extraordinary in these areas.