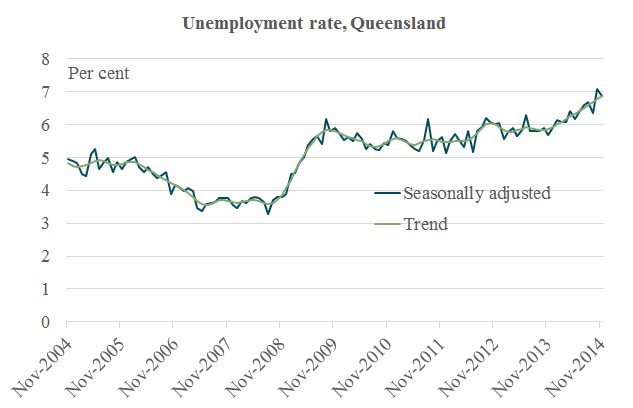

It became clear toward the end of 2014 that the upcoming Queensland election would be fought in a relatively weak economy. 2014 unfortunately saw an increase in Queensland’s unemployment rate from around 6 per cent to around 7 per cent (see chart below), giving Queensland the highest unemployment rate on mainland Australia.

Important forward indicators such as business surveys (e.g. CCIQ Pulse Survey) and job vacancies don’t suggest a strong recovery in the Queensland economy any time soon, although building approvals are more positive. Building approvals have recovered from dismal levels, but remain below highs in the 2000s, and will take a long time to reach former highs unless interstate migration recovers from its current low levels. Because of our low rate of interstate migration, Queensland is now growing at a slower rate than the national average (see Queensland Treasury’s information brief).

A less optimistic outlook than six months ago has led Queensland Treasury to revise its economic forecasts in the Mid Year Fiscal and Economic Review. For example, for the current financial year 2014-15, the average unemployment rate was revised from 6 to 6¼ per cent. This is possibly slightly optimistic, considering if unemployment remains near 7 per cent for much of early 2015. While the seasonally adjusted rate did fall in December, there is a lot of volatility in the data and month-to-month movements typically do not signify a trend.

The Queensland economy continues to struggle to find sources of growth to replace mining sector investment, which is now in decline as construction projects, such as major LNG terminals at Gladstone’s Curtis Island, are wrapping up. This is occurring in the context of continuing below-trend growth in the national economy, which is reinforcing the weakness in Queensland (e.g. see this recent speech by an RBA official: The Business Cycle in Australia).

While the export of LNG will provide a boost to Gross State Product to get economic growth to nearly 6 per cent in 2015-16, this may not translate into a large boost to employment and incomes for Queenslanders. Far fewer people will be employed at the LNG plants once they are in the production phase rather than the construction phase. Also, much of the profits earned at the plants will be repatriated overseas to the shareholders of the oil and gas companies involved in the Curtis Island projects (e.g. see Philip Adams’s article at the Conversation: Why gas isn’t the answer to falling commodity prices or employment).

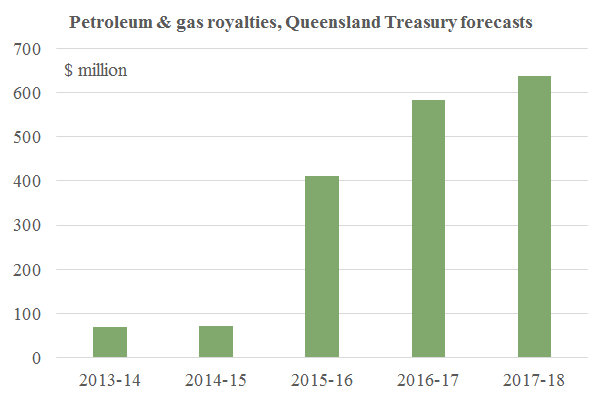

Nonetheless, the export of LNG will provide a welcome boost to Queensland Government revenue through an increase of royalties of the order of $500 million per annum, representing around a 1 per cent boost to total revenue (see chart below). No doubt the Government will be factoring these royalties into its election planning and possible spending commitments.

The lower Australian dollar will provide some relief to the economy, as will lower petrol prices, with a UQ tourism academic predicting an increase in driving holidays (Queensland road trips to return in 2015). Increased tourism as a result of the lower dollar should consolidate recent gains and provide a boost to regional economies such as Cairns, Gold Coast and Sunshine Coast. Lower petrol prices will also provide more disposable income to spend on other items, many of which, such as services, have a greater economic impact than spending on petrol due to less leakage from the economy.

Finally, the Queensland and Australian economies need to contend with risks of economic downturns in other economies, particularly in China. This is one of the great unknowns. Commonwealth Treasury is reasonably optimistic but notes the risks to the Chinese economy in the latest Mid-Year Economic and Fiscal Outlook (p. 9):

An important component of the medium-term reform agenda is financial system deregulation. This is critical to improve the efficient allocation of capital across the economy, but carries with it risks as it will require the management of impaired loans in the system.

To conclude, the outlook for Queensland remains uncertain, but it is reasonably clear the economy will not be strongly recovering in 2015, at least not in the first half of the year. Many Queensland businesses will be waiting to see the outcome of the election and will be hoping the Government starts spending the money it is anticipating from asset leases soon after the election, which should provide a welcome boost to the economy—although we should remain concerned about the value of some of the possible projects funded by the lease proceeds, of course (see my post Privatisation proceeds should be spent wisely).