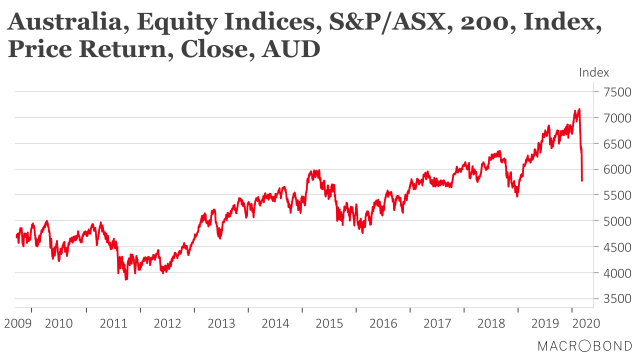

Human psychology can influence financial markets in very weird ways, and such was the case on Monday, which was Wall Street’s worst day since December 2008. The sharp fall in equity markets around the world including here in Australia (see chart below) was arguably justified by a greater understanding of the huge adverse economic impact coronavirus is likely to cause, but it couldn’t be justified by what was the apparent proximate cause: the 30% oil price collapse following Saudi Arabia’s announced supply increase. US President Trump has shown more of an appreciation for economic facts and history than world financial markets in his latest remarks reported by the Financial Times (Trump tries to shift blame for market slide on to oil feud):

On Monday, Mr Trump said the collapse in oil prices would be “good for the consumer” by lowering petrol prices, as he played down the scope of the coronavirus epidemic.

Yes, you would actually expect a supply-induced collapse in oil prices to be good for economic growth because it would lower costs to consumers and businesses. We know that oil price changes in the opposite direction (i.e. oil price increases) have had adverse economic impacts in the past. For instance, the oil price hike of 1973 was a major contributor to the mid-seventies recession.

That said, the relationship between oil prices and the economy isn’t straightforward, as a 2005 note Oil and the Macroeconomy by eminent US econometrician James Hamilton explores. Oil price increases have much more of an economic impact (in absolute terms) than price decreases. And an important complicating factor in the US is now the impact of the oil price collapse on the viability of the US shale oil industry (e.g. see this Fox Business report). In Queensland, a lower oil price will eventually flow through to lower LNG export prices and lower gas royalties paid to the Queensland Government.

Even with the above qualifications, you’d still expect an oil price fall to have a positive macroeconomic impact. Equity markets around the world shouldn’t be plunging because of the oil price shock, although traders and investors are probably justified in being very concerned about coronavirus. They are rightly fearful of a global coronavirus-induced recession.

In Australia, we will learn details of the Morrison Government’s economic stimulus package, expected to be $5 billion or more, later this week. I applaud the federal government for recognising the urgency of this situation and reacting so promptly. However, I think governments at all levels still need to provide more information to the public about the current and planned public health response to coronavirus.

Gene

Great post. I’m really perplexed with what has been happening in the equity markets. 20% off the price of the market in a few days. I suspect the actual impact on firms (i.e. longer-term profits foregone) that actually drive the implicit value of firms will be nothing like that unless the virus hangs around for years.

But with price / ratios still way above long-term averages (currently around 18, off the high of 20 in January, and a long-term average of around 15), I’d be calling this a Covid 19 induced correction rather than a crisis.

Perhaps Eugene Fama might be able to explain how the current actions in the market are a reflection of his efficient market hypothesis, because I surely can’t. There seems to be such a massive disconnect between equity markets and the actual value of equity, I don’t know why we even look to equity markets for clues on what is happening in the real economy.

Thank Jim. I totally agree. Great comments.